Part of our Journal Entries guide

What Are Closing Entries in Accounting?

Closing Entries in Accounting are the different entries made at the end of any accounting year to nullify the balances of all the temporary accounts created during the accounting period and transfer their balance into the respective permanent account.

In simple words, Closing entries are a set of journal entries made at the end of the accounting period to move balances from temporary ledger accounts like revenue, expense, and withdrawal/dividends to permanent ledger accounts.

- It is like resetting the balances of temporary accounts to zero to make it clean to be used in the next accounting period, meanwhile hitting the balance sheet accounts with their balances. It is also known as closing the books, and the frequency of closing can vary as per the size of a company.

- A large or mid-size firm usually opts for monthly closing to prepare monthly financial statements and gauge the performance and operational efficiency. However, a small firm can go quarterly, semi-annually, or even annual closing.

Steps for Posting Closing Entries Journal

- Closing Revenue & Expense: It involves transferring the balances of the whole accounting period from the revenue account and expense account to the income summary account.

- Closing Income Summary: Moving the net income or net loss from the income summary account to the retained earnings account of the balance sheet.

- Closing Dividends: If there has been a dividend pay-out then transferring the balance from Dividends account to the retained earnings account

Example of Closing Journal Entries

To look at it more practically, let’s take closing entries journal example of a small manufacturing company ABC Ltd which is going for the annual closing of books:

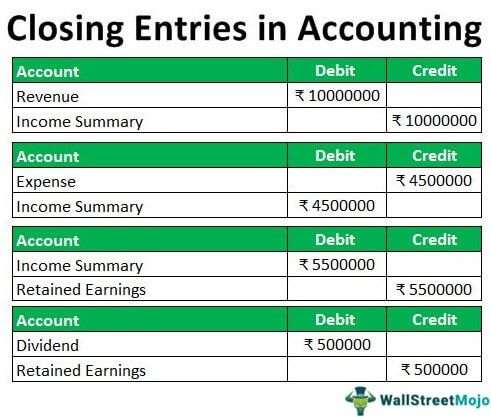

ABC Ltd. earned ₹ 1,00,00,000 from sales revenue over the year 2018 so the revenue account has been credited throughout the year. At the end of the year, it needs to be zeroed out by debiting it and crediting the Income summary account.

| Account | Debit | Credit |

|---|---|---|

| Revenue | ₹ 1,00,00,000 | |

| Income Summary | ₹ 1,00,00,000 |

Let’s also assume that ABC Ltd incurred expenses of ₹ 45,00,000 in the raw material purchase, machinery purchase, salary paid to its employees, etc., over the accounting year 2018.

All these examples of closing entries in journals have been debited in the expense account. At the end of the accounting year 2018, the expense account needs to be credited to clear its balances, and the Income summary account should be debited.

| Account | Debit | Credit |

|---|---|---|

| Expense | ₹ 45,00,000 | |

| Income Summary | ₹ 45,00,000 |

So for posting the closing entries in the general ledger, the balances from revenue and expense account will be moved to the income summary account. Income summary account is also a temporary account that is just used at the end of the accounting period to pass the closing entries journal. It is not reported anywhere.

The net balance of the income summary account would be the net profit or net loss incurred during the period.

In the above case, a net credit of ₹ 55,00,000 or profit will finally be moved to the retained earnings account by debiting the Income summary account. The accounting assumption here is that any profit earned during the period needs to be retained for use in future company investments.

| Account | Debit | Credit |

|---|---|---|

| Income Summary | ₹ 55,00,000 | |

| Retained Earnings | ₹ 55,00,000 |

Something noteworthy here is that the above closing entry can be passed even without using the income summary account. i.e., moving the balances directly from revenue and expense account to the retained earnings account. But using the income summary account was used to give a clear view of the company’s performance when there was only manual accounting. Usually, where the accounting is automated or done using software, this intermediate income summary account is not used, and the balances are directly transferred to the retained earnings account. The temporary accounts need to be zero at the end of an accounting period.

Coming back to our initial example, let’s suppose that ABC Ltd also paid out dividends worth ₹ 5,00,000 to its shareholders during the accounting year 2018, i.e., the dividend account has a debit balance of ₹ 5,00,000, which needs to be credited and then directly debiting the retained earnings account. Since the dividends account is not an income statement account, it is directly moved to the retained earnings account.

| Account | Debit | Credit |

|---|---|---|

| Dividend | ₹ 5,00,000 | |

| Retained Earnings | ₹ 5,00,000 |

Eventually, after following the above steps, the temporary account balance will be emptied into the balance sheet accounts.

Types

Below are the types of Closing Entries segregated into Temporary and Permanent accounts:

#1 – Temporary accounts

Temporary Accounts entries are only used to record and accumulate the accounting or financial transactions over the accounting year, and they do not reflect the company’s financial performance. So it is essential to clear the balances of temporary account so that, for example, revenues and expenses for ABC Ltd. for the accounting year 2018 should be isolated and not be mixed with revenues and expenses of the year 2019.

#2 – Permanent accounts

Permanent Account entries show the long-standing financial position of a company. It is necessary to transfer the balances to this account because it takes into account the appropriate consideration of assets or liabilities for future utilization, e.g., Let’s suppose ABC Ltd. incurred an expense to buy machinery to be used for manufacturing, it is going to be utilized in the future years and not just in the accounting year in which it was recorded, so it needs to be moved to the balance sheet account from the temporary account.

So, if the closing entries journal is not posted, there will be incorrect reporting of financial statements. And not having an accurate depiction of change in retained earnings might mislead the investors about a company’s financial position.

Hence, strong accounting regulations and policies restrict the public listed companies from abusing certain loopholes while producing their financial reports. Apart from the guidelines, there are strict auditing rules to protect and ensure the integrity of the numbers being reported for any accounting period. Having an intermediate income summary account proves helpful to the accountant here as it provides a trail of accounting closing entries for each financial transaction.

Recommended Articles

This article has been a guide to what Closing Entries in Accounting are. Here we discussed types of Closing Entries Journal along with practical examples. You can learn more about accounting with the following articles –