Part of our Journal Entries guide

Journal Entries for Interest Receivable

The following Interest receivable journal entry example explains the most common type of situations where the Journal Entry of Interest Receivable is accounted for and how one can record the same. As there are many situations where the Journal Entry of Interest Receivable can be passed, it is not possible to provide all the types of examples.

Some of the most common Journal Entry of Interest Receivable are given below -.

Examples of Interest Receivable Journal Entry

Below are the examples of Interest Receivable Journal Entries.

Example #1

Company X Ltd. deposited a sum of $ 500,000 in the bank account on December 01, 2018. The accounting year of the X ltd. ends on December 31, 2018. The company earned the interest of $ 5,000 for the December month on bank deposit, but the same was received on January 07, 2019. Analyze the treatment of the interest received by the company and pass the necessary journal entries.

Solution:

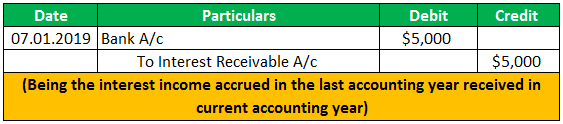

The date when the interest is received: January 07, 2019

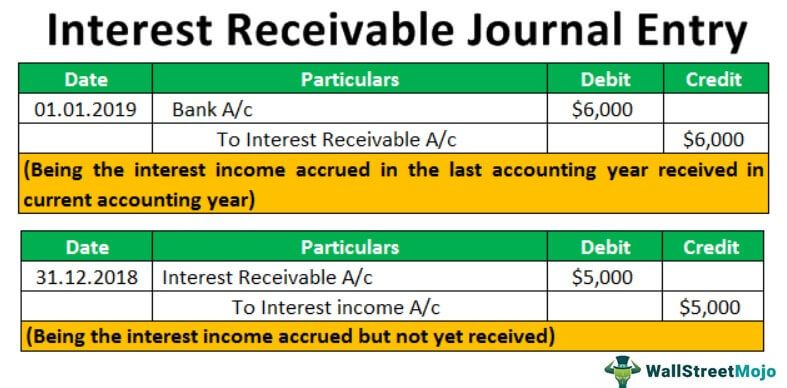

In the present case, company X ltd. earned the interest in one accounting year (ending on December 31, 2018) and received the same in the next accounting year (ending on December 31, 2019). Here, X ltd will recognize the $ 5,000 interest income in financial statements of the year ending 2018 even though the company received the same in the next accounting period because it relates to the current accounting period, i.e., 2018.

The following are the accounting entries for recording interest income receivable in financial statements for the year ending 2018 and the receipt of income in financial statements of the year ending 2019.

Entry to record the interest income receivable

For the year ending December 2018

For the year ending December 2019Entry to record the receipt of interest income

Example #2

Bank gave the loan on September 30, 2018, to one of its employees, amounting to $200,000, on the condition that the interest rate of 12% would be charged. It was promised by the employee to return the principal amount along with the interest portion after three months, i.e., at the end of the accounting year 2018. However, the principal and interest were not paid by the employee at the end of the year. Therefore, on January 01, 2019, the employee sent a check for the payment of the interest portion of the three months.

Analyze the treatment of the interest received by the company and pass the necessary journal entries in the bank’s books.

Solution:

In the present case, the employee was not able to pay the loan principal amount and the interest portion on the due date. The interest portion got accrued in the accounting year ending in 2018 but was not received. So the bank will recognize its income of interest in the accounting year ending in 2018 and record the receipt of the same in the accounting year in which the income is received.

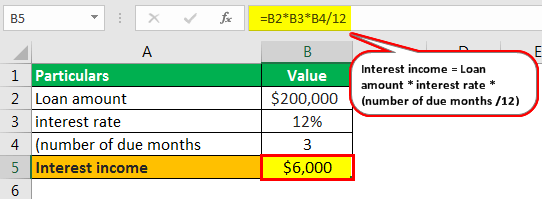

Calculation of Interest income to be recognized in the accounting year ending in 2018.

= Loan amount * interest rate * (number of due months /12)

= $ 200,000 * 12% * (3/12) = $ 6,000

Entry to record the disbursement of loan and interest income receivable

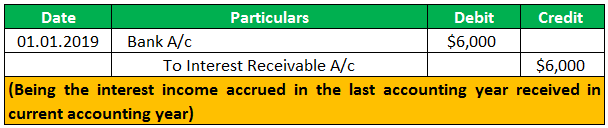

For the year ending December 2018

For the year ending December 2019, Entry to record the receipt of interest income.

Example #3

On November 01, 2018, Company Y ltd purchased a 1-year bond for $ 500,000 that pays the interest at 12% interest. The company will collect the principal and interest amounts due at the end of the bond’s term. Pass the necessary journal entries in the books of the company.

Solution:

At the accounting period ending in 2018, on December 31, 2018, interest has already been accrued for the one month. Therefore, the company can recognize the same in its books of accounts, even if interest has not been received yet.

Calculation of Interest income to be recognized in accounting year ending on 2018

= Loan amount * interest rate * (number of due months /12)

= $ 500,000 * 12% * (1/12)

= $ 5,000

The journal entry for the year ending December 2018 would be:

The above adjusting journal entry will be required at the end of every period to prepare and present the correct monthly financial statement of the company.

Video Explanation of Journal vs Ledger

Conclusion

Interest receivable is an amount that the person has earned but has not been received yet. Once the interest income is accrued (becomes receivable), the journal entry should be passed to record when it became due and the date when the payment against the same is received. Then on that date, the receipt entry should be passed into the books of accounts.

The adjusting journal entry should be passed at the end of every period to prepare and present the correct monthly financial statement of the company to the stakeholders.

Recommended Articles

This has been a guide to Interest Receivable Journal Entry. Here, we discuss the most common Interest Receivable Journal Entries examples and provide detailed explanations. Here are the other articles in accounting that you may like –

- Correcting Entry

- Journal Entry Format

- Record Purchase Credit Journal Entry

- Journal Entries of Accrued Expense

- What is Interest Expense?

Recommended Articles

Continue with these closely related articles from the same guide.