Part of our Journal Entries guide

Reversing Entries Definition

Reversing entries refer to those journal entries passed in the current accounting period to offset the entries for outstanding expenses and accrued income recorded in the immediately preceding accounting period. As these entries are no longer required to be recorded as the business’s assets or liabilities, they are reversed at the period’s start.

Understanding Reversing Entries

Reversing Entries are generally used to simplify the system of bookkeeping in the new financial year of the company. It helps in improving the accuracy of the financial statements of the company because when the entry passed in the previous year is reversed, it prevents the duplication of the recognition of revenue or expense in the current year.

The account debited initially in the books of accounts, of the preceding financial year, is credited in the reversing entries with the same amount at the beginning of the current financial year; and the account which was credited originally in the books of accounts is debited in the reversing entries with the same amount.

Frequently, reversing entries are passed to fix input errors made during the passage of any journal entry. However, reverse entries add to the workload of the individual performing the entries.

Example of Reversing Entries

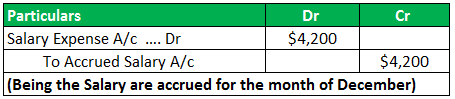

We can take the example of Mr. Daniel, who has an established company of electronics. The financial year of the business closes at the end of December every year. The company has employed staff in the mid of December, for which salary amounting to $4,200. This amount is accrued at the end of December 2018 and not paid. So at the time of closing the books of accounts at the end of December 2018, the following adjusting entry will be passed:

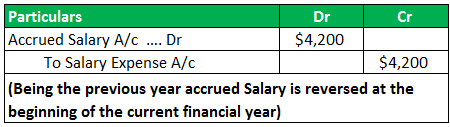

Now in the next year, i.e., at the beginning of the financial year 2019, the above entry will be reversed, and the following entry will be passed:

By this reversal entry example at the beginning of the new financial year, the effect of the previous entry will get canceled out as the reverse entry puts a negative balance in the salary expense account.

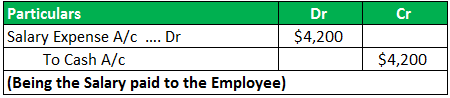

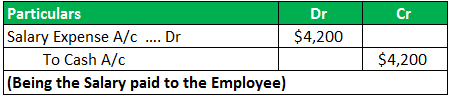

Now, suppose the company paid the salary on January 9th, 2019. The company will record the payment of the salary to the staff by debiting the salary expense account amounting to $ 4,200 with the corresponding credit to the cash accounting having the same amount.

Since there is a negative balance in the salary expense account in the current financial year of $4,200 after passing out the reversing entry, the payment entry of $4,200 will bring the balance of the salary expense account to positive from negative.

Advantages

The different advantages related to it are as follows:

- The passing of such entries helps in improving the accuracy of the financial statements of the company. When the entry passed in the previous year is reversed, it prevented the duplication of the recognition of revenue or expense in the current year.

- A person passing such entries don’t require thorough and in-depth knowledge of the accounting system because of the simplicity of the recording of the reversing entries. That’s because the account debited originally in the books of accounts is credited in the reversing entries with the same amount, and the account credited, is debited in the reversing entries, with the same amount.

Disadvantages

- In case there is an error in recording the reverse entry by the company then it can lead to the overstatement or understatement of the balances in the accounts used for the reversing entries, and this will provide the wrong financial information of the company to the users of the financial statement of the company

- The system of the passing of the reverse entry increases the burden of work of the person making such entries as the person making the reversing entries requires some system for tracking the same to ensure that they complete successfully. This increase in workload also leads to an increase in the chances of getting errors.

Conclusion

Reversing entries are different journal entries that are passed to offset the journal entries which were passed at the end of the immediately preceding accounting year. i.e., they are made in the books of accounts of the company on the first day of the accounting period to remove the adjusting entries of the company’s previous accounting period, and it is the last step of the accounting cycle.

Recommended Articles

This article has been a guide to Reversing Entries and its definition. Here we discuss how it works along with step by step examples. Here are the other articles in accounting that you may like –