Part of our Journal Entries guide

What Is A Journal in Accounting?

Journal of accounting is named as the book of original entry. It’s called the book of original entry because if any financial transaction occurs, the company’s accountant would first record the transaction in the journal. That’s why a journal in accounting is critical for anyone to understand. No matter who you are, a would-be accountant, a finance enthusiast, or an investor who would like to understand the inherent transactions of a company, you need to know how to pass a journal entry before anything else.

- The journal is a fundamental accounting tool to record financial transactions chronologically.

- 2. The journal entry consists of the date, description of the transaction, and debit and credit amounts.

- 3. The journal is used to prepare financial statements and other reports and provides a permanent record of all financial transactions.

- Rules of the journal in accounting: Debit the account when assets and overheads increase and when liabilities and income decreases. And credit the account when assets and overheads reduce and penalties and income increase.

Double-entry system

The double entry system is the system that is used to record entry in the journal. Let’s understand what double entry system is. The double entry system is a system that has two parts – debit and credit. If you know what a debit and a credit are, you would understand the entire financial accounting quite effectively.

Let’s understand the rules of debit and credit briefly, and then we will see the examples of journal entries –

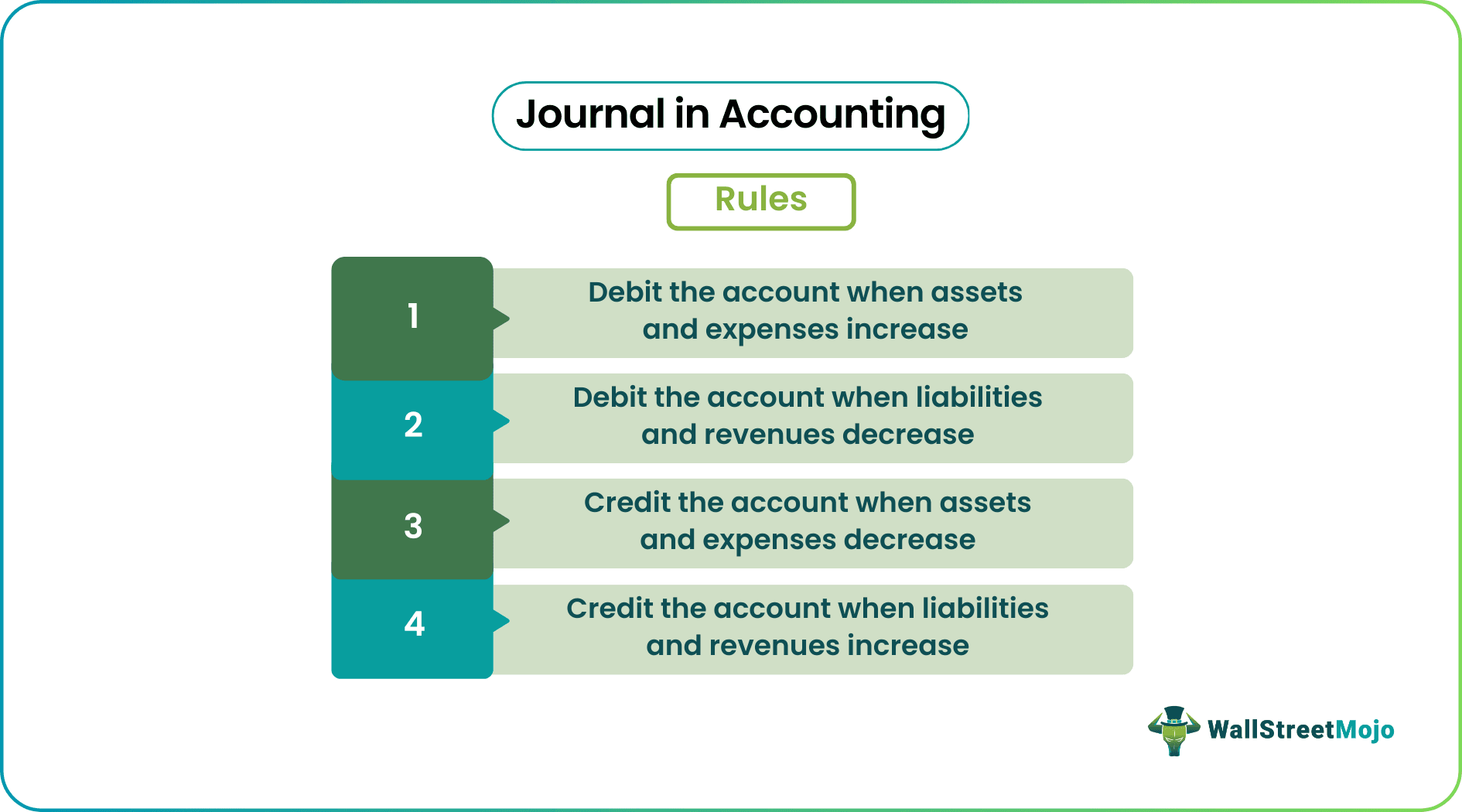

- Debit the account when assets and expenses increase.

- Debit the account when liabilities and revenues decrease.

- Credit the account when assets and expenses decrease.

- Credit the account when liabilities and revenues increase.

The following examples will help us understand how to debit and credit the accounts in transactions.

Journal in Accounting – Video Explanation

How to Make Journal Entries in Accounting?

Example#1

Mr. M buys goods in cash. What would be the journal accounting entry?

As we know the rules of debit and credit, we can see that Mr. M is expanding cash; that means cash is going out, and instead of cash, he is receiving goods. That means “cash”, a current asset is decreasing, and “purchase,” an expense is increasing.

As per the rule, we will credit the account when the asset decreases and debit the account when the expense increases.

So, the journal entry in the accounting book would be –

Purchase A/C…..Debit

To Cash A/C…..Credit

Example#2

G Co. sells goods in cash. Which account will be debited and which account will be credited?

- G Co. sells goods in cash, meaning cash is coming in, and goods are going out. “Cash” is an increasing asset, and “sales” is a revenue account increasing.

As per the rules of debit and credit, when “asset” increases, it is debited; and when “revenue” increases, it is credited.

So, here the journal entry in accounting book would be –

Cash A/C……Debit

To Sales A/C…..Credit

Example#3

Mr. U pays off his long term debt in cash. What would be the journal entry?

Here we can see that Mr. U is paying cash; that means “cash” is going out. And as a result, his long-term debt is also getting checked off. That means “long-term debt,” a liability, is decreasing.

As per the debit and credit rule, when an asset gets reduced, it is credited, and when liability reduces, it is debited.

So the journal entry in accounting book would be –

Long term debt A/C……Debit

To Cash A/C……..Credit

Example#4

More capital is being invested in the company in the form of cash.

In this example, there are two accounts. One is “capital,” and another is “cash.”

Here, cash is invested in the business. As we know, cash is an asset; investing in a business means increasing the asset.

At the same time, due to more cash injection into the business, the capital, which is a liability, also increases. When liability increases, we credit the account.

So as per the rules of debit and credit, the journal entry in accounting would be –

Cash A/C……Debit

To Capital A/C……Credit

Frequently Asked Questions (FAQs)

What is the purpose of the journal in accounting?

The journal’s purpose is to provide a chronological record of all financial transactions of a business. The journal provides a permanent record of transactions and serves as the basis for preparing financial statements and other reports.

What is the difference between the journal and the ledger in accounting?

The journal is used to record financial transactions in chronological order, while the ledger is used to summarize and classify the transactions recorded in the journal. The ledger summarizes the balances of all accounts, while the journal provides a detailed record of individual transactions.

How are journal entries recorded?

Journal entries are recorded in chronological order, each consisting of the date, a description of the transaction, and debit and credit amounts. The debit amount is recorded first, followed by the credit amount. Each entry must balance, with the total of the debit amounts equaling the credit amounts.

Recommended Articles

This article has guided what Journal in Accounting is and its definition? Here we discuss how to make journal entries in accounting and detailed explanations. You may also read through our other articles on basic accounting –

Recommended Articles

Continue with these closely related articles from the same guide.