What Are The Rules of Journal Entries?

Journal is the book of original entry, in which any business transaction is recorded for the first time and chronologically. There are rules of debit and credit that apply to such recording. Such rules vary with the nature of the accounts to be considered in the transaction.

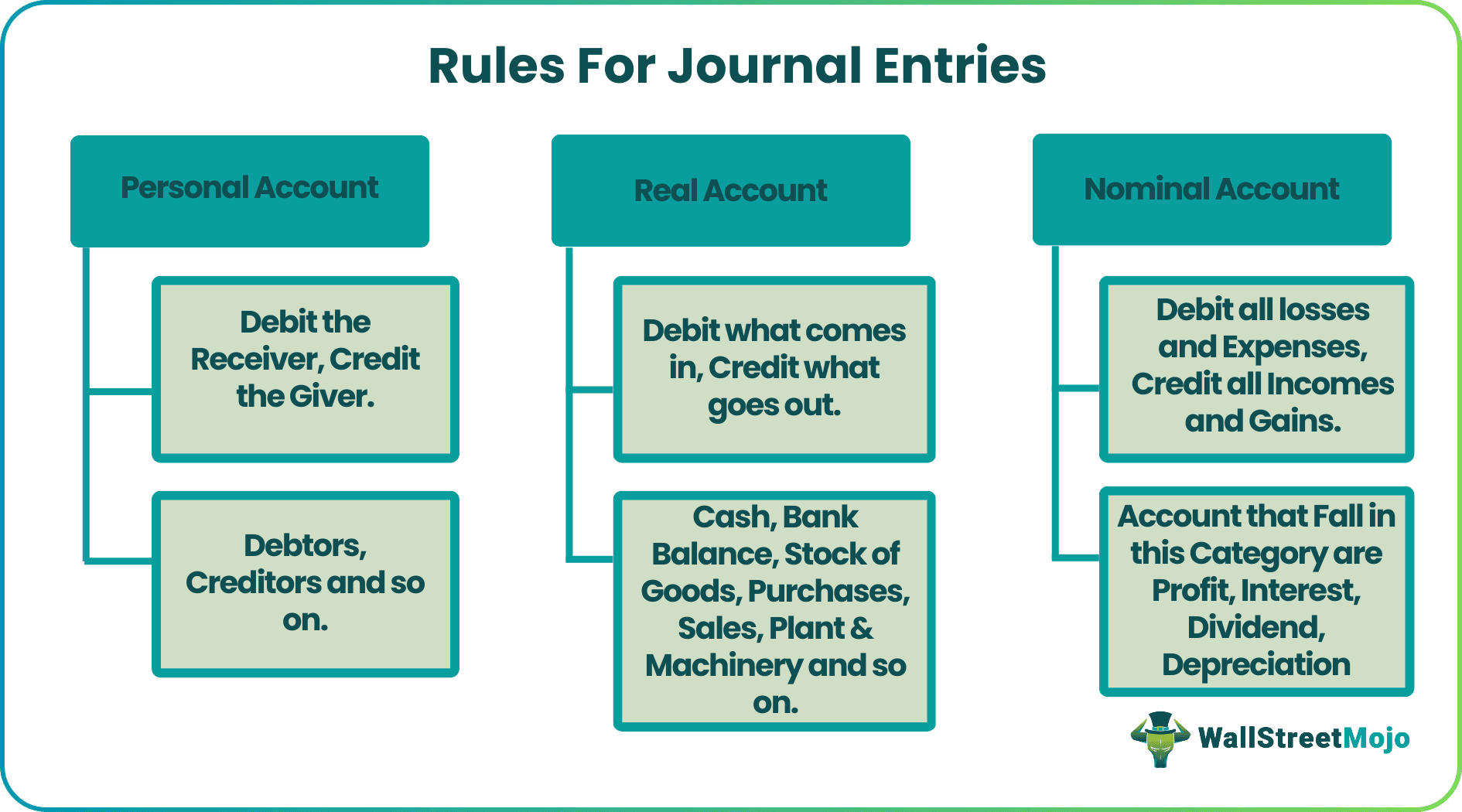

The most popular classification is the Personal, Real & Nominal account and the rules of these are as follows:

#1 – Personal Account

A personal account is that of a person, company, an organization such as a bank, etc.

- Debit the Receiver, Credit the giver.

- Accounts that fall in this category are: Debtors, Creditors, and so on

#2 – Real Account

A Real Account accounts for tangible and intangible items such as inventory, cash, bank account, plant and machinery, and so on.

- Debit what comes in, Credit what goes out

- Accounts that fall in this category are: Cash, bank balance, stock of goods, Purchase, Sales, Plant & Machinery, and so on.

#3 – Nominal Account

This account accounts for profits, losses, incomes, and gains.

- Debit all losses and expenses, and Credit all incomes and gains.

- Accounts that fall in this category are Profit, Interest, Dividend, and Depreciation.

Example of Rules for Journal Entries

Now let’s take a few example transactions to understand these rules in the business context:

On 1st April 2020, Ron & Daughters. started business with cash of $2000 that it received from the owner Mr. Ron

- This transaction deals with two accounts, Ron’s account, and the Cash account

- Ron’s account is personal. The owner’s account is called the Capital account. Ron is the giver in this transaction, so his account should be credited.

- Cash is a real account that comes in, so it should be debited.

On 2nd April 2020, Ron Inc. bought goods with cash for $200

- This transaction deals with two accounts; the Purchase account for goods purchased and the Cash account

- The purchase account is a real account. Goods come in, so the account should be debited.

- Cash is a real account that goes out, so it should be credited.

On 3rd April 2020, Ron Inc. Sold goods for cash for $300

- This transaction deals with two accounts; the Sales account for goods sold and the Cash account

- The sales account is a real account. Goods go out, so the account should be credited.

- Cash is a real account that comes in, so it should be debited.

On 4rth April 2020, Ron Inc. deposited cash in its bank account of $500

- This transaction deals with two accounts, a Bank account, and a Cash account.

- A bank account is a real account that comes in, so the account should be debited.

- Cash is a real account and goes out, so it should be credited.

On 31st April 2020, Ron Inc. paid a salary to the employees of $50 in cash.

- This transaction deals with two accounts, a Salary account, and a Cash account.

- The salary account is a nominal account, and it is an expense, so the account should be Debited.

- Cash is a real account and goes out, so it should be credited.

Rule from the Asset/Liability Classification

Let’s look at the rule from the Asset–Liability classification

- Assets are debited when they increase and credited when they decrease

- Liabilities are credited when they increase and debited when they decrease

Let’s look at all the above transactions of Ron & Daughters from this classification;

1st April

- The firm owes Ron the money he has invested in the firm; therefore, it is a liability from a strong point of view. As liability increases, Ron’s account is credited.

- Cash is an asset that increases, so it should be debited.

2nd April

- Goods are assets, and they increase, so the account should be debited

- Cash is an asset that decreases, so it should be credited.

3rd April

- Goods are assets, and they decrease, so the account should be credited

- Cash is an asset that increases, so it should be debited.

4rth April

- A bank account is an asset that increases, so it should be debited.

- Cash is an asset that decreases, so it should be credited.

31st April

- An unpaid Salary is a liability that decreases, so the account should be Debited.

- Cash is an asset that decreases, so it should be credited.

We need to note a few points:

- Both methods lead to the same entries

- Each entry involves at least two accounts; what is debited is also credited. It is known as the double-entry accounting system

Now let’s record the above transactions in a Journal Proper:

Journal vs Ledger Video Explanation

Note

We need to note a few points:

- Accounts that are debited have ‘dr.’ written against them

- In some countries, the word ‘To’ is avoided in the credit part of the entry

- F. stands for Ledger Folio. It is the column in which we write the page number of the ledger where this entry is posted

- Each transaction has a narration that describes what is happening in this transaction. In some countries, the word ‘being’ is not used, while it is mandatory in other countries. These are minute differences, but the overall accounting process remains the same.

- Journal is prepared for a period, such as a month, and the totals are carried forward to the next period.

- The total debit and credit column should always match; otherwise, there is an error in the recording.

- Sometimes there is an error in recording even when the totals match, such as the omission of entry, so this is not a fool-proof check, but it is still a check.

- Profit and loss are calculated at the time of creating a ledger and the preparation of an Income statement. There are journal entries too for the same; however, for the sake of simplicity, these are not mentioned here.

Conclusion

So, to sum up, there are two classification methods based on which journal entries are recorded. Each method has its rules, but the resulting entries remain the same. Both the methods are based on the ‘Double entry system,’ which is the backbone of accounting and implies that every transaction involves recording in at least two accounts; one is debited while the other is credited.

Journal is the first book of accounts where the transactions are recorded in the accounting process, and it is the most critical step. Any errors here can lead to mistakes in all of the future steps.

Recommended Articles

This article has been a guide to rules for journal entries. Here we discuss the basic rules of the journal entries with the example of a transaction. Yow may learn more about accounting from the following articles –