Table Of Contents

Journal Entry For Accrued Expenses

An accrued expense journal entry is passed on recording the expenses incurred over one accounting period by the company but not paid actually in that accounting period. The expenditure account is debited here, and the accrued liabilities account is credited. The accrued liabilities account is debited when the company settles its obligation with cash, and the accrued expense account is credited.

Accrued expense refers to the expense that has already been incurred but for which the payment is not made. This term comes into play when in place of the expense documentation, a journal entry is made to recognize an accrued expense in the income statement along with a corresponding liability that is generally categorized as a current liability in the balance sheet.

- If the journal entry is not created, then the expense will not appear in the financial statements of the company in the period of occurrence, which will result in a higher reported profit in that period.

- In short, this journal entry recognized in the financial statements enhances the accuracy of the statements. The expense matches the revenue with which it is associated.

Table of contents

Example of Accrued Expense Journal Entry

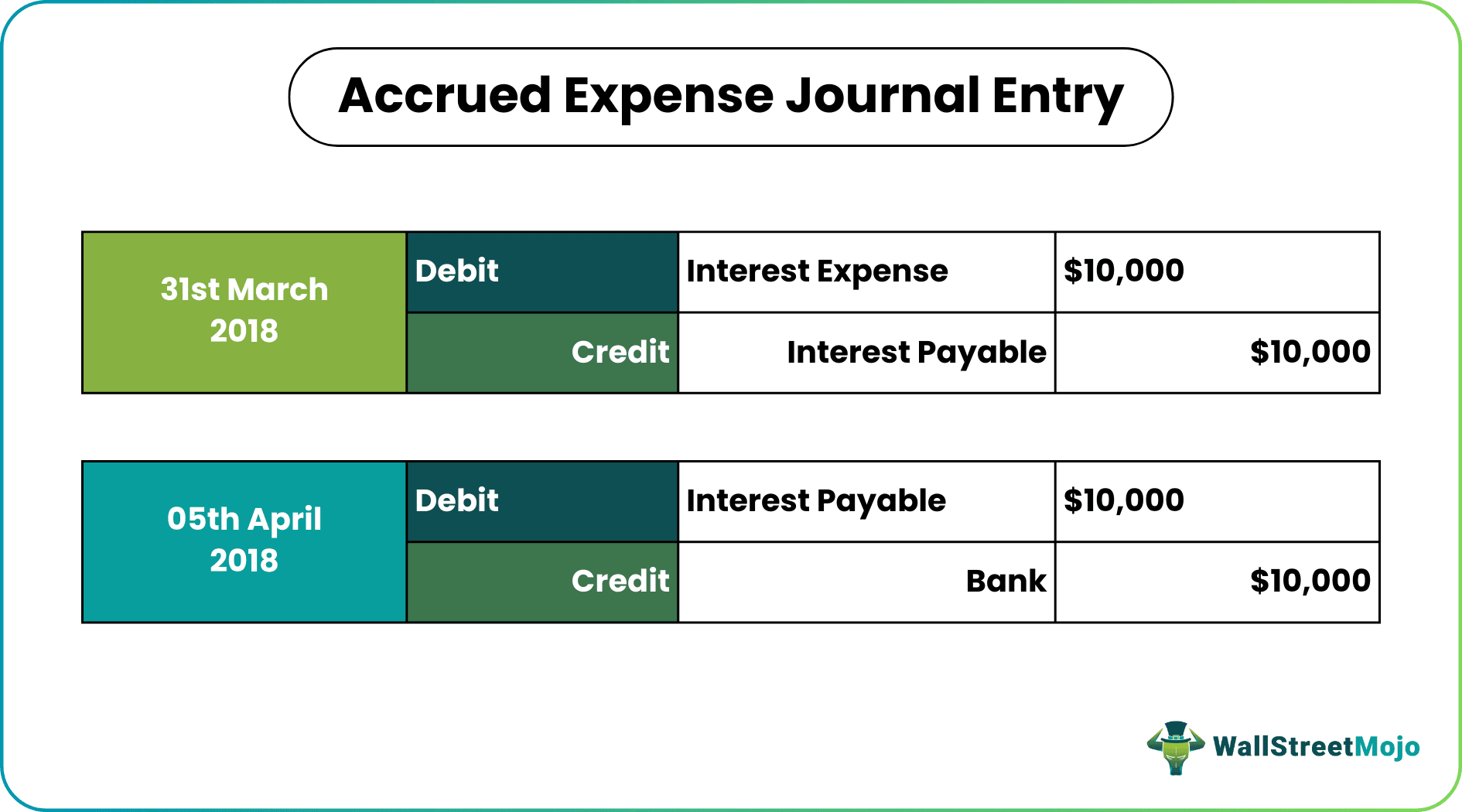

A company, XYZ Ltd, has paid interest on the outstanding term loan of $1,000,000 for March 2018 on 5th April 2018. The interest is charged at 1% per month. Determine the accrued expense journal entry for the example transaction, given that XYZ Ltd reported the accounting year at the end of 31st March 2018.

As per the matching concept, XYZ Ltd will record the interest expense of $10,000 (= 1% * $1,000,000) in the financial statements of the financial year ending on 31st March 2018, even though the interest was paid in the next accounting period, because it is related to the period ending on 31st March 2018.

The following accounting entry will be recorded to account for the interest expense accrued:

| 31st March 2018 | Debit | Interest Expense | $10,000 |

| Credit | Interest Payable | $10,000 |

The accounting entry will be reversed on the day of payment of the interest, i.e., 5th April 2018, and the following accounting entry will be recorded in the subsequent financial year:

| 05th April 2018 | Debit | Interest Payable | $10,000 |

| Credit | Bank | $10,000 |

Advantages

- The primary advantage is the accurate representation of the company’s profit, which otherwise will be overstated.

- Under accrual accounting, liabilities become more transparent. Given that the financial transactions are recorded immediately as it occurs, the chances of discrepancies or errors are almost zero. Also, the information remains easily accessible for audits or similar activities because all the transactions are recorded.

- Another advantage is that the users of the financial statement can see all the obligations of the business along with the dates on which it will become due. Under the cash basis of accounting, the full extent of such transactions is not entirely clear.

- Unlike cash accounting, accounting of accrued expense journal entries is based on the double-entry system. It means that while one account debits, another account credits. A financial user can see that one account decreases while the other one increases. It enhances the accuracy of the accounting system, which makes things easier during audits.

- Another benefit is that GAAP recognizes accrual accounting, and as such, many companies follow the practice of recording accrued expenses.

Essential Points to Note about Accrued Expense Journal Entry

A company usually recognizes an increase in accrued expenses immediately as it occurs. It is credited to accrued expenses on the liability side of the balance sheet. The increase in accrued expense is complemented by an increase in the corresponding expense account in the income statement. Hence, the company will debit the expense account and insert it as an expense line item in the income statement. Therefore, an increase in accrued expense has a reducing effect on the income statement.

On the other hand, a decrease in accrued expenses happens when a company pays down its outstanding accounts payable on a later date. To recognize a decrease in accrued expenses, a company will debit the accounts payable to decrease the accounts payable on the liability side and credit the cash account on the asset side by the same amount. It is to be noted that the cash paid in the current period is not an expense for this period because the related expense has happened and was subsequently recorded in the previous accounting period. Therefore, a decrease in accrued expenses does not affect the income statement.

Conclusion

Although accrued expense is not paid in the same period when it occurs, it is captured in the balance sheet for the period. It is crucial from an accountant's point of view as it helps him maintain a transparent accounting system in concurrence with the matching principle. Also, from an investor's perspective, accrued expense helps ascertain an accurate picture of the company's profit.

Recommended Articles

This article has been a guide to Accrued Expense Journal Entry and its meaning. Here we discuss Accrued Expense Journal Entry examples along with advantages & disadvantages. You can learn more about accounting from the following articles –