Table Of Contents

Default Rate Meaning

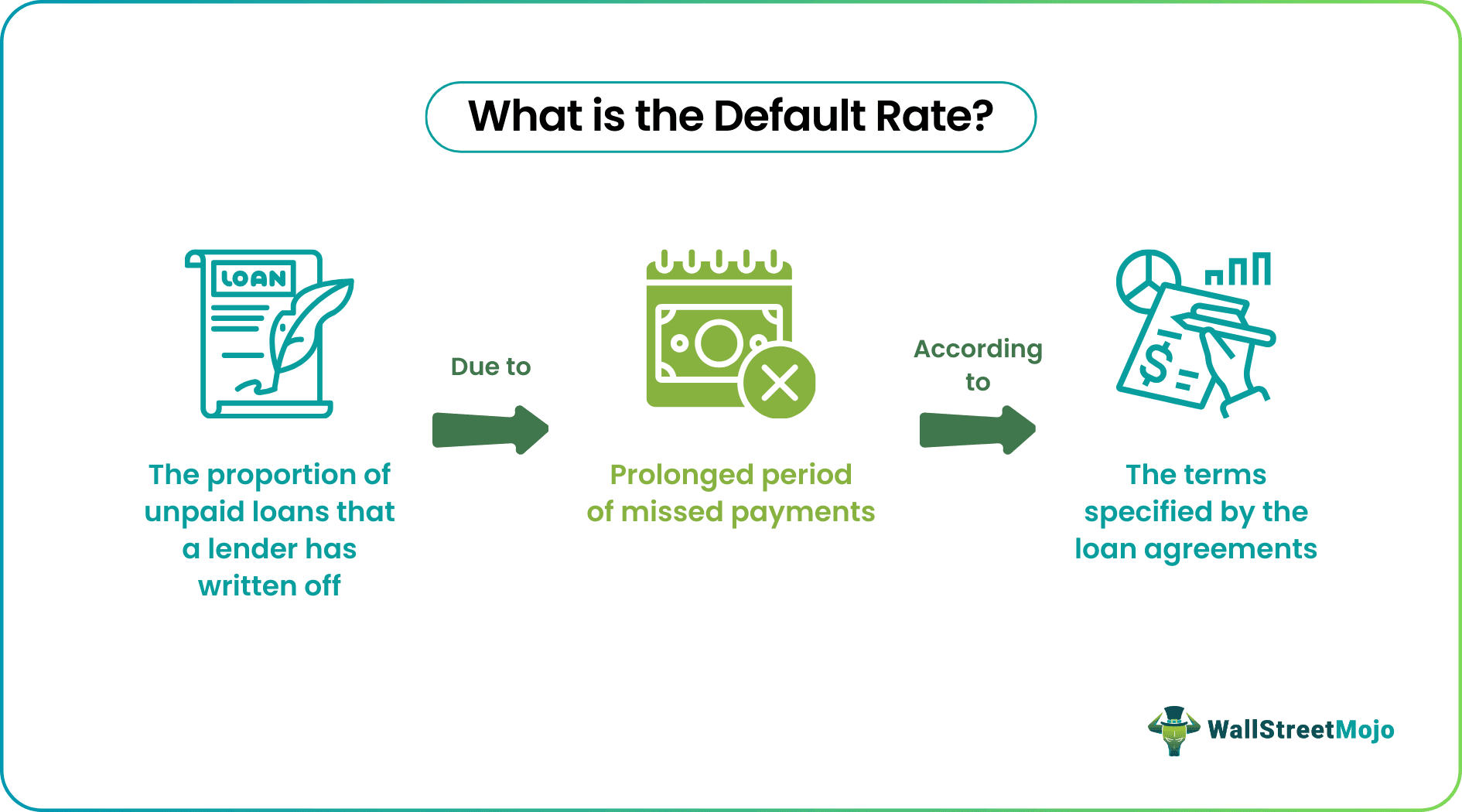

A default rate, also known as a penalty rate in banking, signifies the proportion of loans issued by a lender that has been classified as bad debt written off due to non-repayment by borrowers. This metric serves as a critical indicator applicable to financial lending institutions.

An elevated penalty rate is an adverse signal, suggesting the organization is encountering challenges in effectively recovering its loaned funds. Furthermore, it provides insights into both the economic well-being and the capacity of individuals to meet their financial obligations. It also encompasses the higher interest rates imposed on borrowers who fail to meet payment commitments.

Table of contents

- Default Rate Meaning

- Default rates represent the percentage of loans issued by a lending institution where borrowers default. Defaulting occurs when borrowers fail to make subsequent interest and principal payments, leading the lender to classify the loan as a bad debt.

- Defaulting can be observed across various loan types, including student loans, mortgages, individual loans, and credit cards.

- A cohort default rate is calculated for educational institutions, specifically colleges, and indicates the percentage of students who default on their student loans after making only a few payments. Colleges with high cohort default rates may encounter challenges in obtaining federal grants and loans.

Default Rate Explained

The default rate holds immense significance for lending institutions, with banks being particularly vigilant in their monitoring to ensure effective loan management. A high default or penalty rate serves as a red flag, signaling potential flaws in the lending process. It might indicate that the bank needs to assess borrowers' creditworthiness more accurately, leading to extended loans to individuals more likely to default.

Alternatively, it could suggest that the bank needs to take decisive actions to recover loans. Therefore, various strategies motivate banks to maintain low loan default rates.

To achieve this goal, lenders follow vital steps:

- A meticulous evaluation of an individual's creditworthiness helps identify reliable borrowers.

- Scrutiny of banking activities occurs once a customer displays signs of delinquency.

- Most loans are collateralized, providing a safety net in case of default.

As a last resort, legal measures are employed to facilitate loan recovery. Beyond creditors, economists and governments also monitor penalty rates as indicators of economic health and the populace's capacity to meet financial commitments.

Since many loans are secured by collateral, the prospects of loan recovery are high, barring exceptional cases. Consequently, banks don't hastily label a loan as defaulted when an interest payment is missed. Lenders generally tolerate an initial delay in interest payment. If a second payment is also skipped, delinquency status is declared. Depending on the loan type, sustained delinquency over a certain period designates it as default. For instance, credit card interest overdue for 180 days is classified as default. Once delinquency is acknowledged, lenders may augment interest rates to mitigate losses.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Formula

Here is how to calculate the net default percentage of loans.

Loan default rate = Number of loans defaulted

---------------------------------------- x 100

Total number of loans issued

This formula calculates the percentage of loans that have gone into default by dividing the number of loans that have defaulted by the total number of loans issued, then multiplying by 100 to express it as a percentage.

Examples

Let us understand the concept through the following examples.

Example #1

Here is a calculation example of applying the above formula. Suppose Bank ABC had issued 1000 loans as of December 2022. Fifteen borrowers had defaulted on their loans. Let us calculate the penalty rate of Bank ABC.

Penalty rate = (15/ 1000) x 100

= 1.5%

Example #2

S&P Global Ratings Credit Research and Insights has announced that the US trailing 12-month speculative-grade corporate default rate will increase to 4% by December 2023. This figure would be more than double the 1.7% rate at the end of December 2022. Retail borrowers occupy a higher portion of loan defaults due to inflation and increased debt. Further, debt-service costs will also rise. Borrowers will also need help in refinancing loans according to their terms.

Default Rate vs Delinquency Rate

Understanding the differences between delinquency rate and default rate is crucial in banking. These two metrics provide insights into the health of a lender's loan portfolio and the payment behavior of borrowers.

Below is a comparative table highlighting their distinctions:

| Basis | Delinquency Rate | Default Rate |

|---|---|---|

| Definition | Percentage of loans with overdue interest payments but still need to be deemed bad debts. | It is the percentage of defaulted loans, indicating failure to meet payment obligations. |

| Progression | Delinquency can precede default; not all delinquent loans become defaults. | Default occurs after delinquency if borrowers fail to meet subsequent payments. |

| Severity | It is generally less severe and might be a precursor to default. | More severe, it represents loans that have significantly breached payment terms. |

| Impact on Credit | It can influence credit scores, affecting future borrowing potential. | It strongly impacts credit scores and makes obtaining loans difficult. |

| Lender's Reaction | Lenders notify credit agencies, often considered as a sign of potential issues. | Lenders view defaults as negative indicators of financial stability. |

| Calculation | Delinquency Rate = (Number of Delinquent Loans / Total Loans Issued) * 100 | Default Rate = (Number of Defaulted Loans / Total Loans Issued) * 100 |

| Objective for Lenders | Lenders strive for a lower delinquency rate to manage potential risks. | Lenders aim for a lower default rate to maintain a healthy loan portfolio. |

| Loss to Lender | Delinquent loans might not result in immediate losses. | Defaults can lead to actual financial losses for the lender. |

| Recovery Rates | Delinquency doesn't inherently involve recovery rates. | Recovery rates represent the amount paid to creditors in default cases. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

According to the S&P/Experian First Mortgage Default Index, the first mortgage default rates over a year, from February 2022 to 2023, were recorded at 0.53%. It indicates that 0.53% of mortgagors experienced default on their first mortgage. Correspondingly, the second mortgage default rate for the same period was 0.25%.

Several variables, including geographical location, loan type, and category, influence the trend in default rates. Notably, defaults have risen in segments such as auto loans, bank cards, and first mortgages compared to the previous year. In contrast, defaults on second mortgages have seen a decrease. Despite variations, it's generally observed that default rates across many categories are increasing.

The cohort default rate delineates the percentage of borrowers from a specific college who default on their student loans after making initial payments. The United States Department of Education is the repository for this data, ensuring updates and public access.

Recommended Articles

This article has been a guide to Default Rate and its meaning. Here, we explain it with its formula, comparison with delinquency rate, and examples. You may also find some useful articles here -