What is Bank Rate?

Bank Rate is the rate of interest that the Central Bank charges on the loans and advances to a commercial bank without selling or buying any security. Whenever a bank experiences a shortage of funds, it generally borrows from the Central Bank based on the monetary policy of the country.

- The loans are usually short-term loans that last for a day or overnight. The bank rate is important because commercial banks utilize it to base what they eventually charge their customers for loans.

- Policymakers adopt the bank rate to help them regulate the economy. In reality, it is one of policymakers’ primary means to try and effect economic changes.

- Policymakers can stimulate the economy by lowering the bank rate. That makes loans less expensive, thus encouraging borrowing that expands the money supply and spurs increased spending.

- When policymakers fear that the economy may be growing too rapidly, increasing the risk of inflation, they may raise the bank rate. Raising the bank rate makes loans more expensive. That shrinks the money supply and reduces spending, which dampens the risk of inflation.

- Another important fact about bank rates is that these rates are used as a measure to structure the monetary policy of the economy. The Central Bank controls and manages the currency supply by altering the bank rates. For example, when the unemployment rate increases, the Central Bank of that country reduces the bank rate so that commercial banks offer loans at cheaper rates to individuals. Note that such lending transactions do not involve any collateral.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

What is Repo Rate?

Repo Rate refers to the rate at which the Central Bank lends money to the commercial banks in case of a shortage of funds. The Central Bank uses it to keep inflation under control. When a commercial bank sells the security to the Central Bank to raise money, banks promise to buy back the same protection from the Central Bank at a predetermined date with interest at the rate of REPO. In reality, it is a repurchase agreement.

- Policymakers use this similarly to bank rates to regulate the economy.

- The repo rate is one of the Central Bank’s monetary policy components, used to regulate the money supply, level of inflation, and liquidity in the country.

- During the high levels of inflation, efforts are made to reduce the money supply in the economy. The Central Bank increases the repo rate, making it costly for businesses and industries to borrow money. Consecutively, it slows down investment, reduces the money supply, and negatively impacts the economy. However, this also helps bring down inflation.

- On the other hand, when the Central Bank requires to pump funds into the system, it lowers the repo rate, making it cheaper for businesses and industries to borrow money for different investment purposes. It also increases the overall supply of money in the economy and ultimately boosts the economic growth rate.

Bank Rate vs Repo Rate Video

Bank Rate vs Repo Rate Infographics

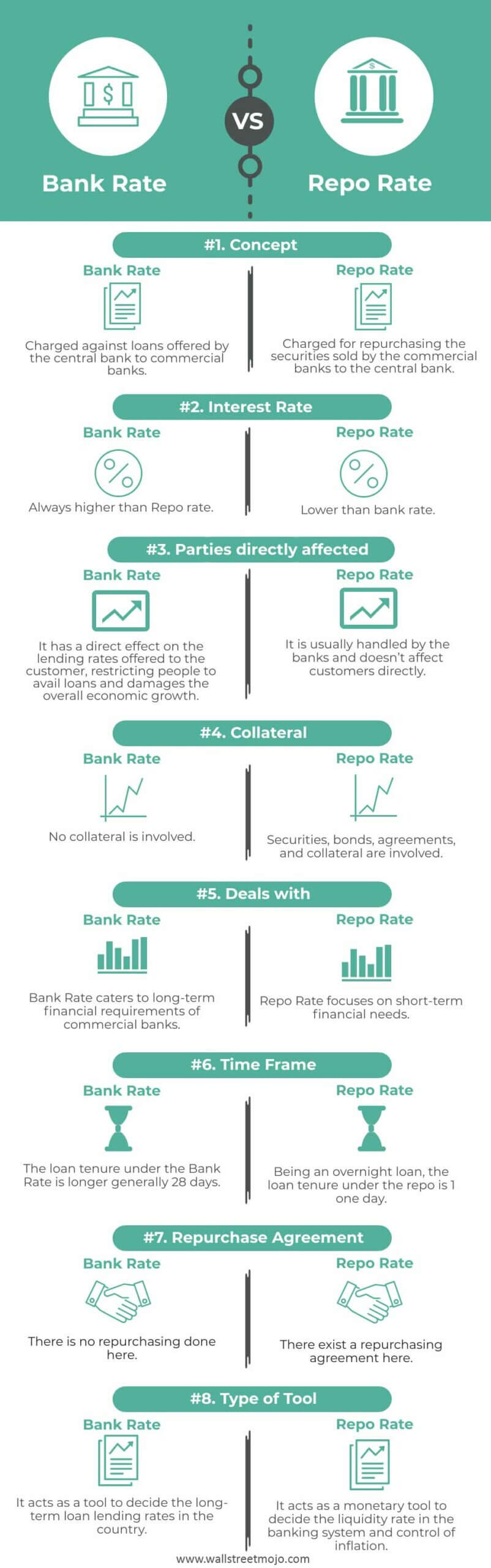

Here, we provide you with the top 8 differences between the bank and repo rates.

Bank Rate vs Repo Rate – Similarities

- The Central Bank fixes the bank rate and repo rate.

- The bank rate and repo rate are used to monitor and control the cash flow in the market.

Bank Rate vs Repo Rate – Key Differences

The key differences between the bank and repo rates are –

- Meaning: The bank rate is described as a discount rate at which the Central Bank (RBI) extends loans to commercial banks and financial institutions. The repo rate is defined as how the Central Bank lends short-term loans to the commercial bank during shortages.

- Charged on: The bank rate is the rate of interest the apex bank charges by the commercial banks for lending the loan, whereas the Repo Rate is the interest rate charged on the repurchase of securities sold by the commercial banks.

- Type of Needs Served: The bank rates are used when the funds are required for long-term purposes, whereas repo rates are used when the funds are needed for short-term needs.

- Repurchase Agreement: In a repo rate, the sale of securities to the Central Bank is performed as per a repurchase agreement, i.e., an agreement to buy back the securities at a predetermined rate and date in the future. Whereas in a bank rate, repurchasing agreement does not exist; it solely lent money to banks and financial intermediaries at a fixed rate.

- Collateral: No securities are required to be provided to the apex bank as collateral when funds are raised through exercising bank rates. However, at the repo rate loan is granted to the banks only after collaterals are provided.

- Interest Rate: The bank rate is used for long-term funds. Thus, the interest is higher than the repo rate. On the other hand, the repo rate is lower than the bank rate.

Bank Rate vs Repo Rate Head to Head Difference

Let us now look at the head-to-head differences between a bank and repo rates.

| Basis of Comparison | Bank Rate | Repo Rate |

| Concept | Charged against loans offered by the Central Bank to commercial banks. | Charged for repurchasing the securities sold by the commercial banks to the Central Bank. |

| Interest Rate | Always higher than the repo rate. | Lower than the bank rate. |

| Parties directly affected | It directly affects the lending rates offered to the customer, restricting people from availing of loans and damaging the overall economic growth. | It is usually handled by the banks and does not affect customers directly. |

| Collateral | No collateral is involved. | Securities, bonds, agreements, and collateral are involved. |

| Deals with | Bank Rate caters to the long-term financial requirements of commercial banks. | Repo Rate focuses on short-term financial needs. |

| Time Frame | The loan tenure under the bank rate is longer, generally 28 days. | Being an overnight loan, the loan tenure under the repo rate is one day. |

| Repurchase Agreement | There is no repurchasing agreement done here. | The repurchasing agreement exists here. |

| Type of Tool | It acts as a tool to decide the long-term loan lending rates in the country. | It acts as a monetary tool to determine the liquidity rate in the banking system and control inflation. |

Conclusion

- The country’s Central Bank is an apex institution authorized to change and monitor the bank and repo rates. The bank rate and repo rate are the elements of the monetary policy rates defined by the Central Bank of the country to control the lending rates by banks, inflation, and money supply in the country. Normally, banks do not borrow money from the Central Bank at the “Bank Rate.” They resort to the Central Bank only in case of a severe shortage of funds.

- The bank rate is a latent weapon to control the interest rate, which, in turn, controls liquidity. However, the repo rate is the top policy rate imposed by the Central Bank that acts as an anchor for the interest rate.

- The bank rate is merely a notional concept now. Barely, any banks borrow from the Central Bank at the bank rate. It is adopted when an imminent shortage of funds indicates a long-term outlook on interest rates. A repo agreement involves keeping government securities as collateral with the Central Bank repurchased once the loan is repaid. The bank rate is generally 100 basis points higher than the repo rate in India.

- Though the bank rate and repo rate have their differences, both are employed by the Central Bank to control liquidity and inflation in the market. In a nutshell, the Central Bank utilizes these two powerful tools to introduce and monitor the liquidity rate, inflation rate, and money supply in the market.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This article guides the bank rate vs. repo rate. Here, we discuss the top differences between the bank rate and the repo rate, along with infographics and a comparison table. You may also have a look at the following articles: –