Part of our Interest Rates guide

What is the Monthly Compound Interest?

Monthly compound interest refers to the compounding of interest every month, which implies that the compounding interest is charged both on the principal and the accumulated interest. Compounding the interest monthly allows individuals to have savings with the interests calculated on interests or have outstanding loan liabilities with interests calculated on the interests being applied at regular intervals.

Monthly compounding is calculated by the principal amount multiplied by one plus the rate of interest divided by several periods whole rises to the power of the number of periods. That whole is subtracted from the principal amount, which gives the interest amount.

Key Takeaways

- Monthly compound interest refers to the monthly compounding of interest, which means that compounding interest is levied on both the principal and the accrued interest.

- It is computed by multiplying the principle amount by one plus the rate of interest divided by the number of periods until the whole rises to the power of the number of periods.

- Then, that total is reduced from the principle amount to provide the interest amount.

- The more significant the frequency, the greater the interest charged or paid on the principle. Monthly compounding may result in a higher interest rate than quarterly compounding.

How Does A Monthly Compound Interest Work?

The monthly compound interest is the rate of interest applied on the principal plus interest amount accumulated over time. In short, it is the interest on interest. This process of compounding interest leads to paced-up growth of the amount in reserves.

For investors expecting good returns, the compound interest concept is a plus as they can expect returns to grow at a faster rate. The borrowers, on the other hand, stay away from interest being compounded monthly as it raises the repayment amount to a considerable high, making repayments difficult.

The interest is compounded either annually, semi-annually, quarterly, monthly, or even daily. Though the interest can be accrued whenever desired, it can formally be recorded only monthly. Once it is formally reflected in the accounts, the monthly compound interest rate is applied. The accruing of the interests is scheduled differently for different financial instruments. For example, Certificates of Deposit or CDs have a compounding schedule of either daily or monthly, while for credit cards, it is daily.

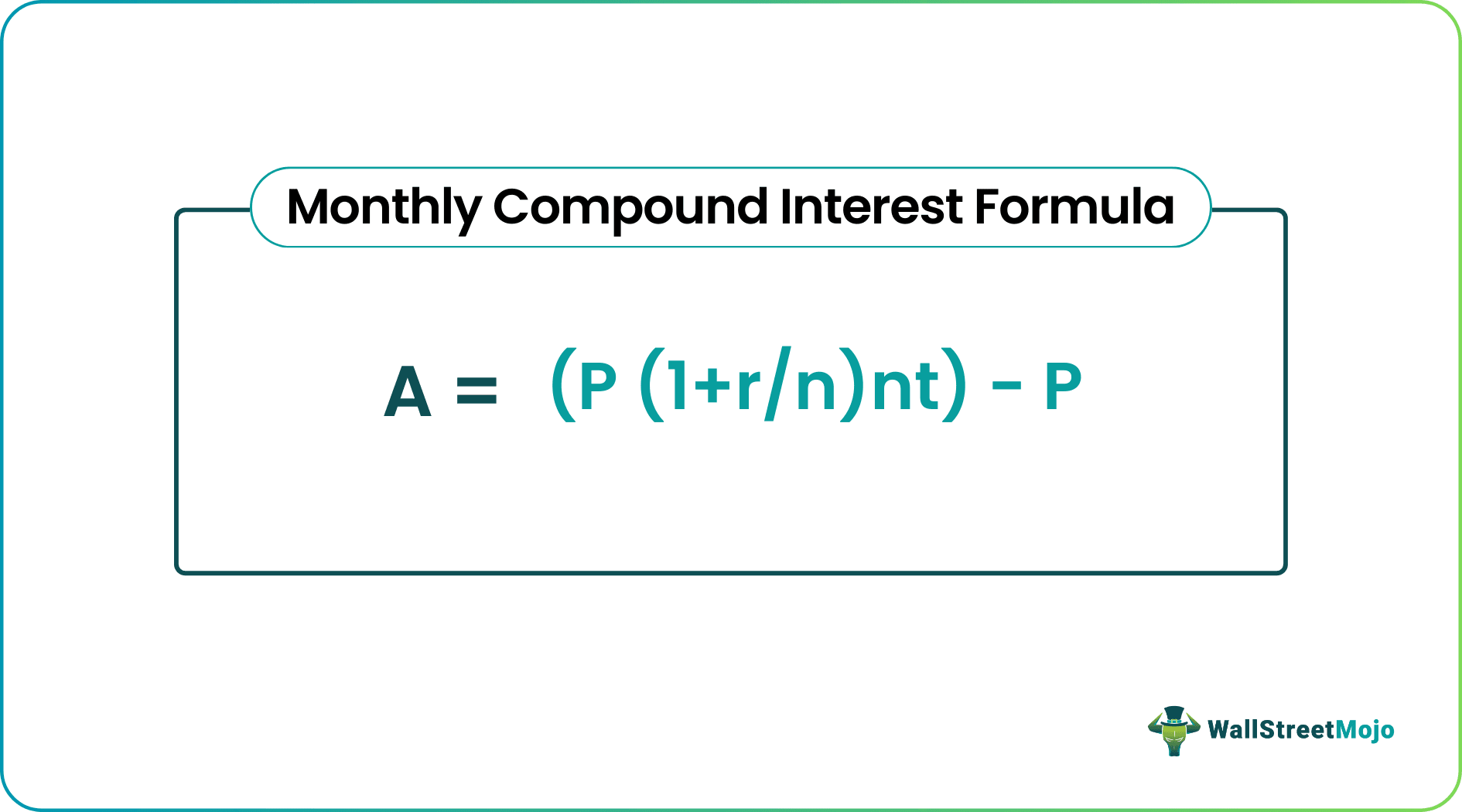

Formula

The monthly compound interest equation for calculating it is represented as follows,

A= (P (1+r/n)nt) – P

Where

- A= Monthly compound rate

- P= Principal amount

- R= Rate of interest

- N= Time period

Generally, when someone deposits money in the bank, the bank pays interest to the investor in the form of quarterly interest. But when someone lends money from the banks, the banks charge the interest from the person who has taken the loan in the form of monthly compounding interest. The higher the frequency, the more interest is charged or paid on the principal. For example, the interest amount for monthly compounding will be higher than the amount for quarterly compounding. This is the business model of a bank in a broader way where they make money in the differential between the interest paid for the deposits and the interest received for the loan disbursed.

Examples

Let us consider the following examples to check how to calculate it monthly compound interest:

Example #1

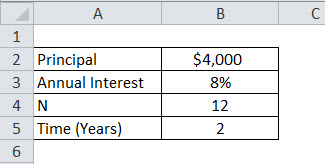

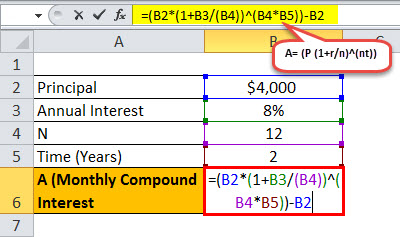

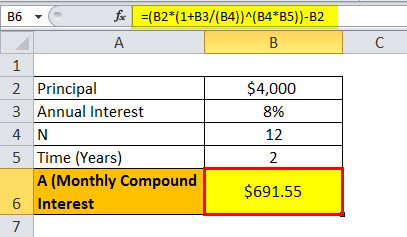

A sum of $4000 is borrowed from the bank where the interest rate is 8%, and the amount is borrowed for a period of 2 years. Let us find out how much will be monthly compounded interest charged by the bank on loan provided.

Below is the given data for the calculation

The Interest can be calculated as,

= ($4000(1+.08/12)^(12*2))-$4000

Example #2

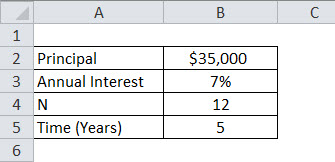

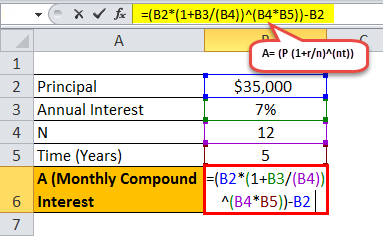

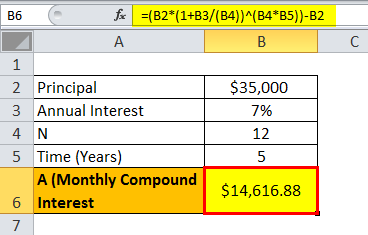

A sum of $35000 is borrowed from the bank as a car loan where the interest rate is 7% per annum, and the amount is borrowed for a period of 5 years. Let us find out how much will be monthly compounded interest charged by the bank on loan provided.

Below is the given data for the calculation

= ($35000(1+.07/12)^(12*5))-$35000

= $14,616.88

= $14,616.88

Example #3

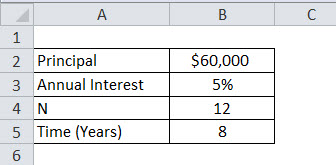

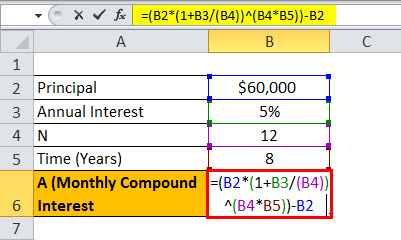

A sum of $1 00,000 is borrowed from the bank as a home loan where the interest rate is 5% per annum, and the amount is borrowed for a period of 15 years. Let us find out how much will be monthly compounded interest charged by the bank on loan provided.

Below is the given data for the calculation

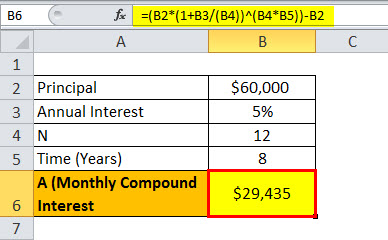

= ($60000(1+.05/12)^(12*8))-$600000

= $29435

So the monthly interest will be $ 29,435.

Relevance and Uses

Generally, when someone deposits money in the bank, the bank pays interest to the investor in the form of quarterly interest. But when someone lends money from the banks, the banks charge the interest from the person who has taken the loan in the form of monthly compounding interest. The higher the frequency, the more interest is charged or paid on the principal. This is how the banks make their money on the differential of interest.

The relevance of compounding interest monthly has been listed below for individuals and individuals to be aware of:

- Helps in making long-term investments for building wealth as the amount grows at a faster pace.

- In the case of loan repayment, when compound interest makes people pay more, they possibly try to get rid of the liabilities quickly.

- The returns are taxable.

- While simple interest is easy to calculate, compounding interest monthly is a complex calculation.

Monthly vs Daily Compound Interest

Monthly and daily compound interest are two forms of compounding that exist in the finance market.

Let us check some of the differences between the two:

- While monthly compounding can lead to better growth of the amount as the interest on interest is applied over that period, daily compounding would only lead to a little growth in the amount.

- Thus, savings multiply extensively due to monthly compounding, while it changes to an insignificant high when compounded daily. Hence, the noticeable change is less for daily compound interest applied.

- The interest is compounded once in every month in the case of the former, while the interest is compounded on a daily basis in the latter case.

The daily interest compounding can be more fruitful when one saves for a longer period. Then, the increase in the or growth in the amount is slightly more noticeable.

Frequently Asked Questions (FAQs)

Is compounding interest monthly better than annually?

. Due to compounding, yearly interest is usually higher. It is because instead of being paid monthly, the invested amount grows over twelve months. However, if you can get the same interest rate for monthly installments as you can for annual payments, go for it.

How do you earn when interest is compounded monthly?

Here are some of the finest investments to take advantage of compound interest: certificates of deposit (CDs), high-yield savings accounts, bonds, and bond funds, money market accounts, dividend stocks, and real estate investment trusts (REITs) are all examples of financial instruments.

How to do monthly compound interest in Excel?

To calculate the final worth of an investment after a particular period, we may use the following formula: A is equal to P(1 + r/n)nt. If the investment is compounded monthly, we may substitute 12 for n:

A = P(1 + r/12)12t.

Recommended Articles

This has been a guide to what is Monthly Compound Interest. Here, we explain its formula, examples, vs daily compound interest, and relevance & use. You can learn more about Excel modeling from the following articles –