Part of our Interest Rates guide

Simple Interest Definition

Simple interest (SI) refers to the percentage of interest charged or yielded on the principal sum for a specific period. Borrowed funds (loans), investments, and deposits are considered the principal sum.

Calculating Simple Interest is easier than calculating compound interest. Also, the amount of interest remains the same through consecutive periods of borrowing or deposit. SI is the fee borrowers pay lenders.

- Simple interest (SI) is the method of directly evaluating the percentage charges on the principal sum for a specific period.

- For a borrower, it is the amount charged as SI on the loans, credit card dues, etc. Whereas for a depositor or investor, it is the returns from investments, bonds, and debentures.

- However, after the emergence of compound interest (CI), the SI method has become less popular due to its inability to provide progressive returns to investors. Lenders also earn more with the CI method.

How Simple Interest Works?

Simple interest (SI) is evaluated as the percentage charged on the principal sum borrowed or deposited for a specific tenure. SI is usually denoted in years. Thus, it is the actual cost incurred on the principal amount. This excludes the outstanding interest. In the real-world scenario, the Non-Banking Finance Companies (NBFCs) widely use the SI method for extending short-term loans such as consumer loans and personal loans. Some of these loans have a tenure of 3 months. Further, it is beneficial for the borrowers to pay off the sum earlier to reduce their liability.

Although banks and investors usually prefer compound interest (CI) over the SI method, it is still used for mortgage loans, auto loans, and car loans. Moreover, the coupon payment of certain bonds and SI on certificates of deposit are computed using the SI formula. Even suppliers often charge SI on credit sales of goods or services.

SI is significantly different from CI. CI is the rate charged on the principal sum and the overall outstanding interest amount. For an investor, the CI yields a higher amount. While SI is calculated as P*R*T / 100, CI is computed as P*[1+r] t. Most bank transactions like bank loans and deposits use the CI method.

Simple Interest Formula

To understand the calculations, let us first look at its formula:

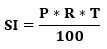

Here, SI = Simple Interest,

- P= Principal Amount,

- R= Rate of Interest, and

- T= Time (in years).

The elements of SI are explained below:

- Principal Amount: It is the sum borrowed, invested, or deposited.

- Rate of Interest: The percentage of interest charged from the borrower or offered to the depositor. It is often written as R/100.

- Time: The duration for which the SI is to be computed, denoted in years. Say, if the period is in months, then it is represented as quarters or half-year. It is divided by 12, 4, or 2, respectively.

Simple Interest Examples

Let us now go through the calculation part, and for this purpose, we are illustrating three different examples where Simple Interest is applicable.

#1 – Deposits

Mr. A deposited $5000 in the RST bank. If the bank offers SI at 4% p.a., find out the interest receivable after 2 years.

Solution:

SI = (P*R*T)/100

SI = (5000*4*2)/100

SI = $400

Thus, Mr. A. will receive $400 as SI after 2 years.

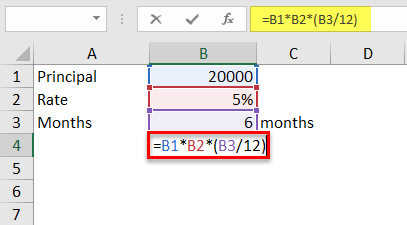

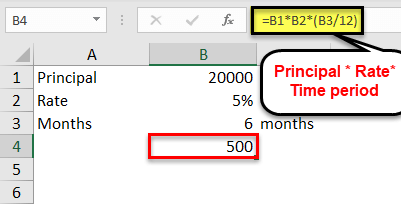

#2 – Bonds

ABC Bank subscribed to the certificate of deposits totaling $20000 issued by the government of India, which carries a 5% interest per annum. The certificate of deposits matures in 6 months.

Interest earned by ABC Bank on the certificate of deposits:

SI = Principal * Rate* Time period

Thus, ABC Bank will earn a total interest of $500 on the certificates of deposits on maturity, i.e., after 6 months.

#3 – Mortgages

XYZ Ltd. mortgaged its office building with RST bank against a loan of $300000 for 5 years. Suppose the interest rate is charged at 9% p.a. and payable semi-annually. Calculate the half-yearly installment and the total amount chargeable from the company in 5 years.

Solution:

Total interest payable on a mortgage loan:

- SI = (P*R*T)/100

- SI = (300000*9*5)/100

- SI = $135000

Half-Yearly Instalment:

Interest payable half-yearly = (P*R*T)/ (100*2)

- Interest payable half-yearly = (300000*9*1)/ (100*2)

- Interest payable half-yearly = $13500

Number of Payment Periods= Total Years*2 (semi-annual)

- Number of Payment Periods = 5*2

- Number of Payment Periods = 10

Principal Amount Payable Half-Yearly = Principal Amount/ Number of Payment Periods

- Principal Amount Payable Half-Yearly = 300000/10

- Principal Amount Payable Half-Yearly = $30000

Half-Yearly Instalment = Principal Amount Payable Half-Yearly + Interest Payable Half-Yearly

- Half-Yearly Instalment = 30000 + 13500

- Half-Yearly Instalment = $43500

Thus, XYZ Ltd. has to pay total interest of $135000 in half-yearly installments of $43500.

Note: While computing interest payable half-yearly, we have taken the time as ½ since we calculate interest for six months, and when it is converted into years, it becomes 6/12 or ½.

Advantages And Disadvantages

SI forms the base for learning this concept for short-term borrowings, bonds, debentures, etc. So, let us understand the various other benefits of using this method:

- Easy to Calculate: As the name suggests, it is one of the most straightforward formulas for evaluating interest.

- Remains Constant: The amount for all the periods is the same in the SI method until the borrower makes an early payment or the investor withdraws funds.

- Applicable on Short-Term Borrowings: In the present era, SI is extensively used by the Non-Banking Financial Credits for computing short-term borrowings like consumer and personal loans.

- Early Payment Benefit: The borrowers can always reduce their debt and installment burden by paying off the loan sum before the due date. This means that as the period of repayment reduces, the amount also falls.

Moving on, the following are the limitations of the Simple Interest method:

- No Compounding Benefit: The major setback is its failure to provide progressive returns to the depositors or investors. This is why the CI method is popular with banks.

- Lower Returns: Since SI is received only on the sum invested or deposited, the earnings are limited.

- Limited Application: In the modern banking and finance system, the SI method has lost relevance and is restricted to short-term loans and advances.

Frequently Asked Questions (FAQs)

What is simple interest?

Simple Interest is a method of charging or yielding a specific percentage on the principal amount borrowed or deposited in a particular period. SI can be computed as the product of principal amount, interest rate, and time. Following is the formula for this method; SI = (Principal*Rate*Time)/100.

What is the difference between the Simple Interest method and the Compound Interest method?

Simple Interest is a more convenient way whereby the interest is computed as a specific percentage of the principal amount in a certain period and remains the same in every consecutive period. However, the Compound Interest method is slightly complex since it is calculated as a percentage of the principal amount plus the overall interest due.

Do banks use the Simple Interest method or Compound Interest method?

Banks provide CI on the savings account using the compounding method, i.e., the annual percentage yield (APY). Also, most of the bank loans are charged with a CI, i.e., on the missed installment (comprising of the interest amount) along with the additional principal amount due.

Recommended Articles

This has been a guide to what is Simple Interest and its Definition. Here we discuss the SI formula, calculations, examples, advantages, and disadvantages. You may also look at the below articles to learn Corporate Finance.