Part of our Interest Rates guide

Euribor Definition

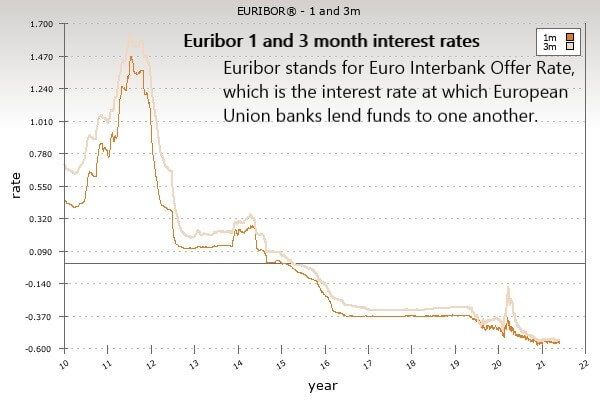

Euribor stands for Euro Interbank Offer Rate, which is the interest rate at which European Union banks lend funds to one another. It is a benchmark and reference interest rate that changes daily and covers tenures ranging from a week to a year.

According to the European Commission, the Euro Interbank Offer Rate is a critical benchmark. This is because it helps in arriving at key lending rates in the eurozone market.

- Euribor (Euro Interbank Offer Rate) is the benchmark interbank lending interest rate prevailing in the eurozone unsecured money market. It defines the interest rate for all the 8 short-term maturities with varying tenures.

- The tenures include one week, two weeks, one month, two months, three months, six months, 9 months and one year.

- It is regulated and computed by the European Money Markets Institute (EMMI) using the interbank interest rates of 18 influential European banks, constituting the panel.

- The representative banks in the panel have to submit their interbank interest rates according to the contribution procedure of the Code of Obligations of Panel Banks (COPB).

- EMMI uses the 30% trimmed mean method for calculating these rates and thereby adopts the standard mechanism of Benchmark Determination Methodology (BMR).

How Does Euribor Work?

Euribor is the interest rate used as the benchmark for inter-bank short term borrowing amongst many European banks. The loans are unsecured and are financed through excess reserves available with the banks. The time period of loans ranges from a week to a year, with the exchange occuring in Euros. As such, the Euro Interbank Offer Rate provides seperate lending rates for all these maturities.

Euribor sets a benchmark for retail and business loans in the eurozone money market along with many financial products. It is computed as the average of different interest rates at which many European banks provide short-term, unsecured lending.

The European Money Markets Institute (EMMI) evaluates and administers this rate every day. It is estimated using a standard mechanism suggested under the Benchmark Determination Methodology (BMR). It involves contributions from a representative panel of banks. Thomson Reuters publishes the rate daily at 11.00 am as the designated distributor.

It is similar to the London Interbank Offered Rate (LIBOR), which is the benchmark rate for global interbank short term lending. Like LIBOR, the Euro Interbank Offer Rate also facilitates the pricing of savings accounts, mortgage loans, interest rate swaps, forward rate agreements, etc.

How is Euribor Calculated?

The European Money Markets Institute (EMMI) evaluates and takes the help of certain banks to determine Euribor rates. The authority makes a daily request to a representative panel of 18 banks to submit their interbank short-term lending rates. These credit institutions have to follow a specific contribution procedure in adherence with the Code of Obligations of Panel Banks (COPB).

As a methodology, the 30% trimmed mean method is used to compute the average interbank interest rates offered by the panel banks for different maturities. Thereafter, Thomson Reuters calculates Euribor by eliminating the 15% of the lower and upper ends of the interest rates data. This is followed by computing the mean value of the remaining rates to a maximum of three decimal points. After this, Thomson Reuters publishes the final rates at 11 a.m.

The contributing banks include those belonging to EU countries whether they participate or not participate in the euro. It even consists of non-EU large international banks, essential for eurozone operations. The representative panel of 18 banks is listed below.

Market Impact of Euribor Rates

Euribor rates affect mortgage loans, derivative instruments, savings account, Euro interbank term deposits, futures and other financial products in the eurozone. An example of how the rates affect EU consumers can be understood with a variable rate mortgage.

The interest rate on a loan is not fixed under a variable rate mortgage. The interest rate of variable rate mortgage is formed using a Euribor rate and its percentage spread. As such, when Euribor rates go up, your interest rate on the variable rate mortgage loan will also go up.

Euribor Rates

Euribor rates define the interest rates for all the 8 short-term maturities with varying tenures. The tenures include one week, two weeks, one month, two months, three months, six months, 9 months and one year. Thus, for example, there will be a separate interest rate for the 3 month Euribor which has been a negative number since 2016.

In fact, for some years, Euro Interbank Offer Rate rates have been negative. In 2014, the European Central Bank (ECB) had brought in negative interest rates. In 2020, its deposit rate was -0.5%. The negative rates policy requires banks to pay interest on their excess reserves. Consequently, it pushes banks to lend more. While it lowers overall borrowing rates, it also reduces the revenue of credit institutions.

The 2021 Euribor rates for different maturities according to the official EMMI website are as follows:

| Particulars | 17-06-2021 | 18-06-2021 | 21-06-2021 | 22-06-2021 | 23-06-2021 |

|---|---|---|---|---|---|

| 1week | -0.573 | -0.560 | -0.558 | -0.564 | -0.569 |

| 1month | -0.555 | -0.548 | -0.550 | -0.553 | -0.553 |

| 3months | -0.543 | -0.544 | -0.542 | -0.540 | -0.538 |

| 6months | -0.513 | -0.513 | -0.511 | -0.508 | -0.509 |

| 12months | -0.486 | -0.485 | -0.480 | -0.477 | -0.478 |

Rigging of Rates

There have been incidents where the individuals from participating banks have adopted illegal ways to manipulate the rates of Euribor. It is deemed a severe offence since these rates are crucial for fixing key banking and finance rates.

Manipulation of interest rates can increase the borrowers’ financial burden and decrease banks’ earnings. When talking about rate rigging, we cannot miss the case of Deutsche Bank. In 2015, Deutsche Bank was separately fined by the US and US regulators over LIBOR and Euribor interbank rates manipulation.

The US and UK regulators altogether imposed a fine of 2.5 billion on the Deutsche bank. Another crucial reason behind the penalty was the bank’s misleading attempts to hamper the investigations.

Euribor vs Libor

The purpose of both these rates is similar, i.e., the averaging of interbank short-term lending rates. Although, both these rates differ from one another in multiple ways.

- Euribor is a reference interest rate applicable to the Eurozone banks, i.e., the banks operating in the eurozone countries. LIBOR is a global reference interest rate used globally as a benchmark or reference for short-term lending.

- The former is the mean of interest rates prevailing in the eurozone interbank market. The latter is the average interest rate applicable to the credit institutions in the global market.

- Also, the Euro Interbank Offer Rate comes in the euro; the London Interbank Offer Rate is used in different currencies, including the US dollar.

- In 2020, it was reported that LIBOR would cease to exist by June 30, 2023. The move came after LIBOR rates were caught at the center of controversies such as rates rigging and financial debacles of troublesome years.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

What does Euribor stand for?

<p>Euribor is expanded as u0022Euro Interbank Offer Rateu0022. It is a benchmark rate for inter-bank borrowing amongst eurozone banks.</p>

What is the Euribor curve?

<p>The forward curve graphically represents the market’s expectation and prediction of future Euro Interbank Offer Rate, using the current and previous information.</p>

What is the difference between Euribor and Libor?

<p>Euribor is worded as Euro Interbank Offer Rate that is adopted as a reference interest rate for uncollateralized lending in the eurozone interbank market and comes in euro. <br/><br/>Whereas the LIBOR is an abbreviation for London Interbank Offer Rate, it is a benchmark rate applicable to the interbank transactions globally.</p>

How is Euribor used?

<p>Euribor is served as a benchmark in the eurozone interbank market for pricing of <br/>• Financial Products – Car loan, mortgage loan, savings account; and <br/>• Derivative Instruments – Futures contract, forward rate agreements, interest rate swaps.</p>

Recommended Articles

This has been a guide to what is Euribor and its definition. Here we discuss Euribor rates for different maturities and list of the panel banks along with examples, advantages, and disadvantages. You can learn more about accounting from the following articles –