Reference Rate Meaning

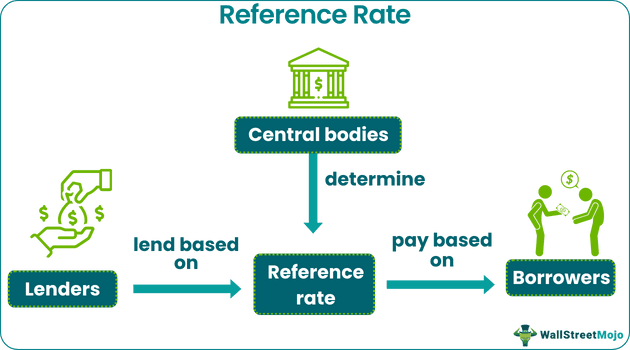

A Reference Rate is a benchmark interest rate that acts as a point of reference for determining the interest rates of loans, bonds, derivatives, and various other financial contracts. It is typically fixed by the central bank in a country or any other relevant organization to maintain equilibrium in the economy by ensuring that interest rates across markets are aligned with economic and market conditions.

These rates play a key role in financial markets by enabling smooth market functioning and seamless market operations. It acts as the basis for executing standardized trading contracts (derivatives, floating-rate notes, etc.) at low transaction costs. Besides, they reduce any asymmetry in the market. The reference rate framework differs across countries due to differences in regulatory environments, economic conditions, and market structures.

- Reference rates act as a benchmark or base that helps determine the rates of interest rates in the economy.

- These rates originated in the 1950s, introduced by the Federal Reserve Bank of New York. The UK introduced LIBOR in 1986, while the Fed Fund Rate came into effect in July 1954.

- The central banks and regulatory bodies of various economies have a crucial role in setting this rate. LIBOR was a crucial global reference rate until it was abolished in 2017.

- The reference rate reform eliminated unnecessary interest rates and helped entities adopt new rates for better functioning.

Reference Rate Explained

The reference rate helps set the rates of various financial contracts and securities. For instance, the London Interbank Offered Rate (LIBOR) is a benchmark rate used as a reference for unsecured short-term borrowing.

These are crucial for both lenders and borrowers. Also, they help predict the financial condition of an economy. They are monitored by the public and private sectors due to their importance in keeping financial systems stable.

In the mortgage market, the reference rate framework has great importance. It defines the benchmark against which mortgage interest rates are fixed. Financial institutions and lenders add a margin or spread to arrive at the actual interest rate that will be applied to the borrowings. This margin or spread covers a lender’s operating expenses and risks and enables lenders to make profits. Typically, if a borrower’s credit score is not favorable, the margin may be higher than normal.

The application and uses of these rates prevail in many ways. It can lower transaction costs and increase market liquidity. A reference rate must meet certain requirements, which are:

- It must provide a standardized point of reference for pricing financial instruments, eliminating or reducing the need for individual negotiations and related costs. Such standardization facilitates lower transaction costs and increased market efficiency.

- The rate must enhance the liquidity of financial markets. Market participants should be able to easily buy and sell financial instruments without the need to continually reevaluate the asset value based on independent credit assessments or market conditions.

- They must work as effective hedging tools that enable interest rate risk management. Financial institutions and other market participants use these rates to hedge against potential adverse movements in interest rates to protect their portfolios and maintain financial stability.

These rates must adhere to certain principles and guidelines to ensure the credibility and effectiveness of the financial system. They must be immune to economic crises and follow transparent fallback period procedures (a period when the rate cannot be determined due to specific circumstances). Also, they should be frequently published, and fast contract verification is required.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

History

The history of reference rates pertaining to the US dates back to the 1950s when the Federal Reserve Bank of New York (FRBNY) commenced publishing the daily federal funds rate. It is the interest rate that banks charge each other for overnight loans of reserves, and it served as a critical benchmark for other interest rates that affected the US financial system.

In 1986, the LIBOR was established as a global benchmark interest rate. It was derived from estimated average interest rates at which banks in London lent unsecured funds to other banks in the London interbank market. LIBOR gained rapid popularity and was recognized as the key reference rate for a wide range of financial instruments, loans, bonds, and derivatives. Though LIBOR became globally relevant, the federal funds rate was still the primary domestic benchmark in the US.

Purposes

Floating reference rates are used for various purposes in financial markets. Let us study them.

- Reference rates are useful in determining the floating rate legs of loans. Since mortgage and interest rates depend on a base rate, these rates are important.

- They are used in derivatives contracts for managing interest rate risk.

- These rates are a vital component of the exchange-traded and futures market for pricing, settlement, and risk management.

- These rates are an integral part of risk and asset-liability management.

- Other than financial contracts, they are useful while administering compensation schemes, credit ratings, accounting practices, etc.

Examples

Let us study a few reference rate examples to understand the topic better.

Example #1

Suppose Bank A operates in the United States. Before 2021, it followed the LIBOR reference rate as a benchmark for interest rates. So, by taking LIBOR as a reference, mortgage and loan rates were fixed. However, after 2021, LIBOR was abolished. Bank A found it challenging to adjust to this new situation. It used a different base rate based on the revised guidelines. However, it had to consider the following while adopting a new rate and fixing interest rates on mortgages:

- Interpreting the new rate structure and updating its systems

- Communicating the changes to existing and new customers

- The cost of lending, along with its own operating costs

- The margin or spread it would like to have on each mortgage deal

- The risk it is willing to accept against every loan application, which is based on the borrower’s creditworthiness

Imagine a different lending situation for Bank A where the reference interest rate was not abolished. So, when Bank A wanted to determine the interest rate for loans in 2022, the LIBOR rate was 5.47% in December 2022. There was also a surge of 375 points. So, for borrowers, the total interest rate (6%, 5.8%, or 6%) applicable would be the reference rate (5.47%) plus basis points (375).

Example #2

In December 2022, the Financial Accounting Standards Board (FASB) extended the sunset date of the temporary guidance in ASC 848, Reference Rate Reform, to December 31, 2024, from December 31, 2022.

It means those entities that are in the process of transitioning from LIBOR to another interest rate index can continue operations in line with ASC 848 until the end of 2024. This provision simplifies accounting for several entities and helps them combat the potential adverse effects of the discontinuation of LIBOR in a planned manner.

Reference Rate Reform

The reference rate reform refers to the initiative taken by regulators to drop certain rates and introduce new Alternative Reference Rates (ARRs) in their place. The rates that will be discontinued after the reform are called eligible reference rates. For example, LIBOR is an eligible rate that has no importance after reform. However, this reform has many consequences on accounting and financial contracts.

If these rates exit the market, the financial contracts associated with these rates will become pointless. To avoid this, they are adjusted to match the new rate. Thus, the Financial Accounting Standards Board (FASB) issued Topic 848 to help entities address the accounting burden by enabling them to tackle the accounting implications of such a change.

LIBOR was a major point of reference among the interest rates in use earlier. As a result, regulatory bodies felt the need to remove unnecessary rates. Therefore, in July 2017, the Financial Conduct Authority of the United Kingdom announced the need to discontinue LIBOR due to concerns over manipulation and market fragility, among others. Instead, the Working Group on Sterling Risk-Free Reference Rates chose the Sterling Overnight Interbank Average (SONIA) as an alternative. Later, countries like the US, Australia, and Switzerland adopted alternative reference rates.

As the publication of the USD LIBOR ceased in 2021, and the remaining USD LIBOR (one-month to 12-month tenors) ceased by June 2023, the Secured Overnight Financing Rate (SOFR) came into existence. SOFR is an overnight benchmark interest rate that allows borrowing in exchange for US collaterals.

According to the Federal Reserve Bank of New York, this rate has an overnight transaction of $800 billion. However, the Euro Interbank Offered Rate (EURIBOR) and Swiss Average Rate Overnight (SARON) are recommended as alternative rates in the rest of Europe. LIBOR exited in 2021, and SARON futures were launched in the same year.

Pros And Cons

Reference rates are a crucial element of the futures and financial markets. Here are their pros and cons.

| Pros | Cons |

|---|---|

| It links financial contracts and standardized money markets for smooth functioning. | During crises, there is considerable floating reference rate fluctuation. |

| These rates reduce the complexity of financial contracts. | The chances of widening an economy’s financing conditions are high when these rates are not used properly. It causes a rise in overall cost and difficulty of borrowing money in an economy. |

| It decreases translation costs and increases market liquidity. | The rate introduces certain threats like manipulation, misuse, and high operational risks. |

| It acts as an effective hedging tool for market participants. | Cross-border policies and market elements influence these rates. |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. Are alternative reference rates published at different times?

Alternative reference rates can be published at different times depending on the country, the specific rate, and the entity in charge of publishing these rates. These rates are used as substitutes for traditional benchmark interest rates such as the LIBOR or the EURIBOR. SOFR is the rate used in the US; it is published daily by the Federal Reserve Bank of New York.

2. What are exchange reference rates?

These rates refer to the benchmark exchange rates used to enable currency exchange for international deals. They are usually published by central banks or other reputable financial institutions.

3. How are reference rates determined?

Reference rates are determined through various methods, and the process a country adopts can vary based on the type of rate applied and the institution or governing body in charge of computing it.

4. How are alternative reference rates calculated?

Regulatory authorities calculate alternative rates based on the transactions conducted before the market opens. Broadly, data collection, rate calculation, and publishing are the steps involved in this process. Secured Overnight Financing Rate (SOFR), Sterling Overnight Index Average (SONIA), and American Interbank Offered Rate (AMERIBOR) are some well-known alternative reference rates.

Recommended Articles

This article has been a guide to Reference Rate and its meaning. Here, we explain its reform, history, examples, purpose, and pros & cons. You may also find some useful articles here –