What Is Deferred Interest?

Deferred interest is the total amount of interest generated on loan but remains unpaid and such interest gets accumulated when the total amount of loan payment is so small that it is unable to cover all the pending interest amount and therefore increases the principal balance of a loan.

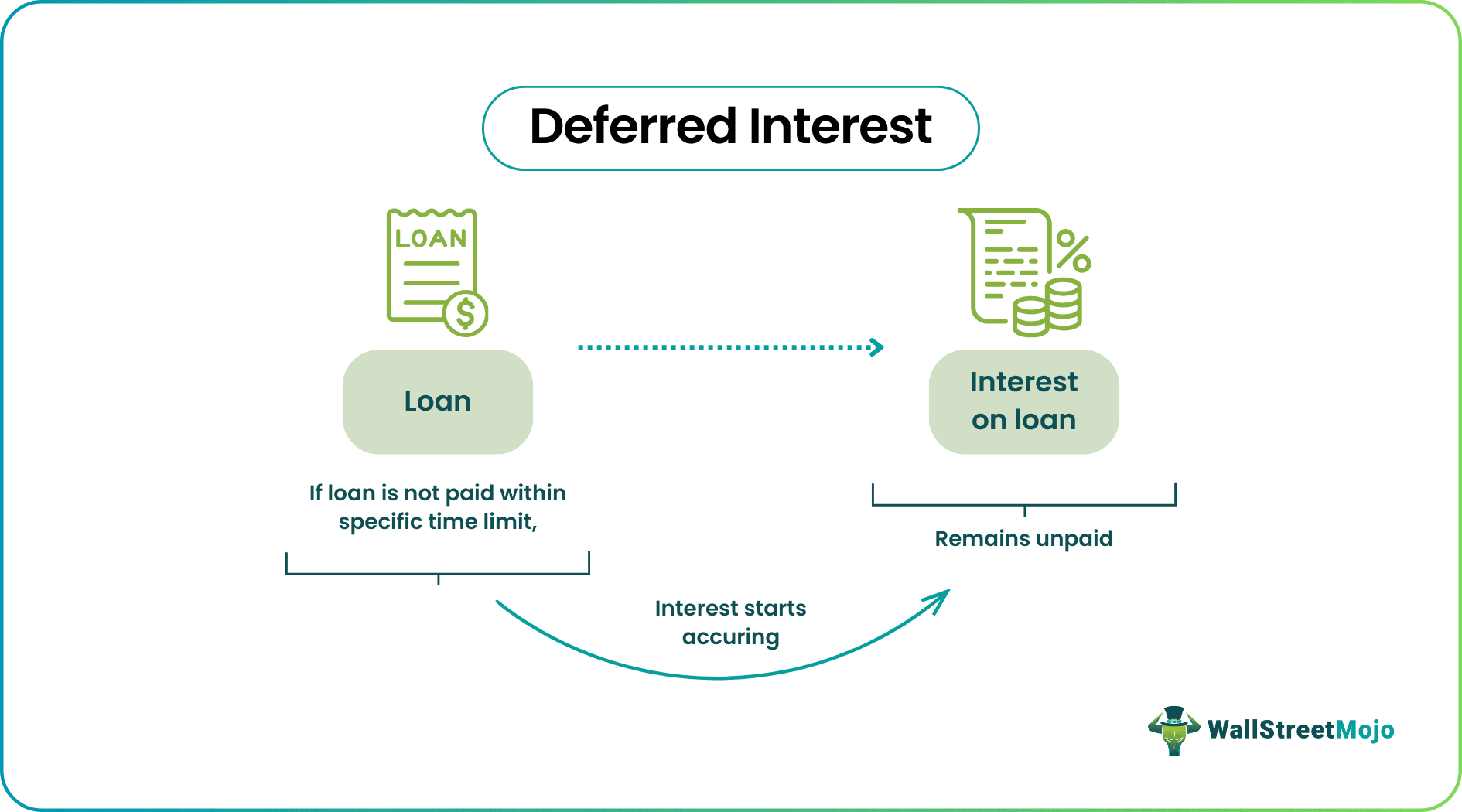

When the payment of interest gets delayed or deferred due to payment plans for a particular period of time is termed as a deferred interest plan. These are usually advertised as “no interest charges until” a particular date, and once that date is crossed, interest starts to accrue, and since then, the interest from the date of purchase is charged to that account.

- Deferred interest refers to a financing arrangement where interest charges on a loan or credit purchase are temporarily postponed or “deferred” for a specific period.

- During the deferred interest period, interest accumulates on the loan or credit balance, but the borrower is not obligated to make interest payments. Instead, the accrued interest is added to the principal balance.

- Lenders or retailers frequently offer deferred interest as a promotional or introductory feature to incentivize purchases or loans. It allows borrowers to postpone interest payments.

How Does It Work?

Deferred interest is one of the most commonly used methods which is used by lenders to sneak additional charges with respect to the so-called zero interest deals. Such an arrangement allows the borrower to pay minimum interest for a temporary period in comparison to what lenders actually charge.

This must also be noted that the borrower might pay a lower rate of interest only if they are able to repay the loan amount before the end of the promotional period. If the deadlines are missed, then the interest charges start to pile up. The borrower might even face compulsion to pay the full deferred interest charges of their original purchase irrespective of how much he or she has paid off until then.

Deferred interest payment are usually marketed as no interest charges until a designated time period, and after that date, interest starts accruing, and then the borrower will have to pay the interest that started to accrue from the day of purchase. If the borrower is able to repay the deferred interest loan amount within the stipulated time period, then they will not have to pay any amount of interest on the same.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How To Calculate?

Deferred interest payment can be calculated in the following steps-

In the first step, one must determine if his or her deferred interest is offering to suspend interest for a couple of months. This is common in the case of credit cards as well as installment plans for expensive products like furniture, jewelry, home appliances, etc.

One must go through the contract and find out if at all, there is no interest in the designated time period mentioned in the contract.

One must look for the deferred interest charges mentioned in the contract as well as the amount of time that he or she has for repaying the debt which is taken.

In the next step, simply multiply the amount that is owed with the rate of interest and the number of years left for paying the same back.

- Lastly, one must deduct the interest from the interest-free period if at all, the interest doesn’t accrue.

Example

Let us go through an example to understand the concept.

For example, A purchased a $1,000 couch at 10% a year and has two years to pay; then A will have to pay $200 in interest, which will be calculated by multiplying the purchase price with the rate of interest and number of days left, i.e., 1,000*10%*2. If the amount of interest accrues, then A will have to pay $200 — 2 years of interest — back in a year, along with the $1,000.

How To Avoid?

Deferred interest loan can be spotted when there are offerings that state “zero interest for twelve months” or “same as cash.” Borrowers do have the option and choice to avoid paying deferred interest, but doing so is really complicated. Such programs are very common when the borrower uses in-store financing or uses store credit card offers. These programs are common in the cases of expensive products like furniture, jewelry, and home appliances. These programs can be mostly seen in abundance during winter holidays since it becomes easy for the retailers to convince buyers to spend extra money on purchasing gifts and pay later. High-end credit card companies and online retailers are also seen in making these offers.

Deferred Interest On Credit Cards

Deferred interest loan allows the buyers to purchase with their credit card without having to pay interest on the remaining balance. Deferred interest on credit cards can help buyers shop on their credit cards at the moment, and they will not have to pay the monthly interest, which will keep accruing after the collapse of the promo period.

If the balance is paid before the promo period has ended, then the buyer can avoid paying interest altogether. But if he fails to repay before the intro period ends, then he will be bound to pay all the interest that has accrued since the very first day.

Deferred Interest VS 0% APR

A 0% APR offer is different from deferred interest. In the case of 0% APR, one will not need to pay any amount of interest, and the interest shall only start to accrue once the promotion ends. If there is a minimum balance left at the end of the offer, then the interest will incur on that small amount only whereas, in a deferred interest loan, a sizable retroactive charge is built for the promotional period.

Benefits

Just like any other financial concept, this concept also has its own advantages and disadvantages. Let us try to understand the advantages, as given below:

- If the deferred interest mortgage is paid fully by the borrower within the stipulated time period, then the borrower will not have to pay the interest amount on the same. This means that the borrower get some extent of financial flexibility and can allocate their funds to some other useful purpose.

- The benefits of deferred interest could only be reaped by an individual if only he or she is able to pay back the total amount of deferred interest on the loan before the end of the designated period.

- The arrangement lowers the monthly installment payments during the deferral period since the borrower does not have to pay the interest amount. This makes the payment more manageable.

- Deferred interest is often used as a promotion or an incentive to attract clients. Consumers can make large purchases immediately.

- The borrowers can use the deferred interest amount to invest in sources that provide good returns.

Limitations

This concept come with some limitations too. Let us understand them in details.

- If the borrower is not able to pay off the interest during the deferral period, then the accrued interest gets accumulated with the principal and results in the magnifying the final payment.

- Sometimes this kind of deferred interest mortgage comes with high rates. Lenders compensate the time gap by charging higher rates. Therefore, the borrowers should be careful while accepting such system.

- Accepting such a payment system needs some financial discipline. Regular payments should be made to pay off the interest before the deferral period. Failure to do so leads to higher rates, penalty and loss of credit score.

- The system may provide a short-term flexibility but may restrict the borrower from making any changes in the payment schedule or modify the agreement in any way.

- The borrower may end up taking more loans to meet the obligations of the deferred interest if they are not able to pay up the amount on time. Thus, it is extremely important to be careful and be certain about one’s creditworthiness.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. What is the difference between accrued and deferred interest?

Accrued interest refers to the interest earned but not yet paid or received. It accumulates over time and is usually based on the outstanding balance or investment amount. Deferred interest, on the other hand, refers to interest charges that are temporarily postponed or deferred for a specific period.

2. What are the risks associated with deferred interest arrangements?

The risks associated with deferred interest arrangements include potential misunderstanding or underestimation of the terms and conditions, high-interest rates or penalties after the deferral period ends, and the possibility of accumulating a significantly higher overall cost if the balance is not paid in full by the end of the deferral period.

3. Why is deferred interest an asset?

Deferred interest is considered an asset because it represents the accumulated interest that will be received or realized in the future. It is an asset for the lender or creditor as it represents the amount owed by the borrower or debtor, and it has a future economic benefit in the form of interest income for the lender.

Recommended Articles

This has been a guide to what is Deferred Interest. We explain interest on credit cards along with example, how to calculate & how to avoid. You can learn more about from the following articles –