Table Of Contents

What is International Trade?

International Trade is the exchange of goods and services across international borders. It usually comes with additional risks caused by changes in exchange rates, government policies, laws, judicial systems, and financial markets.

Cross-border trade comprises import, export, entrepot, foreign direct investment, job outsourcing, setting up production in other countries, and setting up of multinational companies. Cross-border commerce increases the reach of local traders and producers—manufacturers upgrade their products and services to suit global demands.

Table of contents

- What is International Trade?

- International trade refers to the purchase or sale of goods or services outside geographical boundaries. It is a means of global economic interaction between the buyers and sellers of different countries.

- Global trade occurs via three routes—import, export, and entrepot.

- It works on the principle of comparative advantage—one nation specializes in producing a specific product—gains reputation—then supplies the product to the international market.

International Trade Explained

International trade drives a country's growth. Import-export figures are one of the top contributors to a country's gross domestic product. Thus, every country tries to strengthen its global trade relationships with world leaders.

In the 18th century, Adam Smith brought the international trade theory of comparative advantage analysis into the limelight. It was founded on the the mercantilist thoughts of the British School of Classical Economics. In Wealth of Nations, the author instigated the need for specialized goods production amidst extensive demand and scarce supply of resources. Later, the classical economist David Ricardo proposed the principles of comparative advantage.

Goods and services are imported goods due to the following reasons:

- Low price

- Superior quality

- Lack of availability in the domestic market

- Excessive demand

- Low supply

Similarly, goods are exported due to the following reasons:

- Higher value in the international market

- International quality

- Excess production in the domestic market

- Increasing demand in the global market.

Often, companies set up their production units outside their geographical boundaries to avail cheap labor, natural resources unavailable domestically, and lower cost of production.

International Trade Types

Cross border trade can take place via three different routes:

- Import: Primarily, when a country is incapable of producing products domestically, goods are imported.

- Export: When a country produces surplus goods or services of international quality, it can sell these outside its geographical boundaries. Such international selling of products is termed export trade.

- Entrepot: It is a blend of import and export. Country A buys goods or services from country B and sells them to country C after adding some value to the goods.

Examples

Let us look at some examples to better understand global commerce.

Example #1

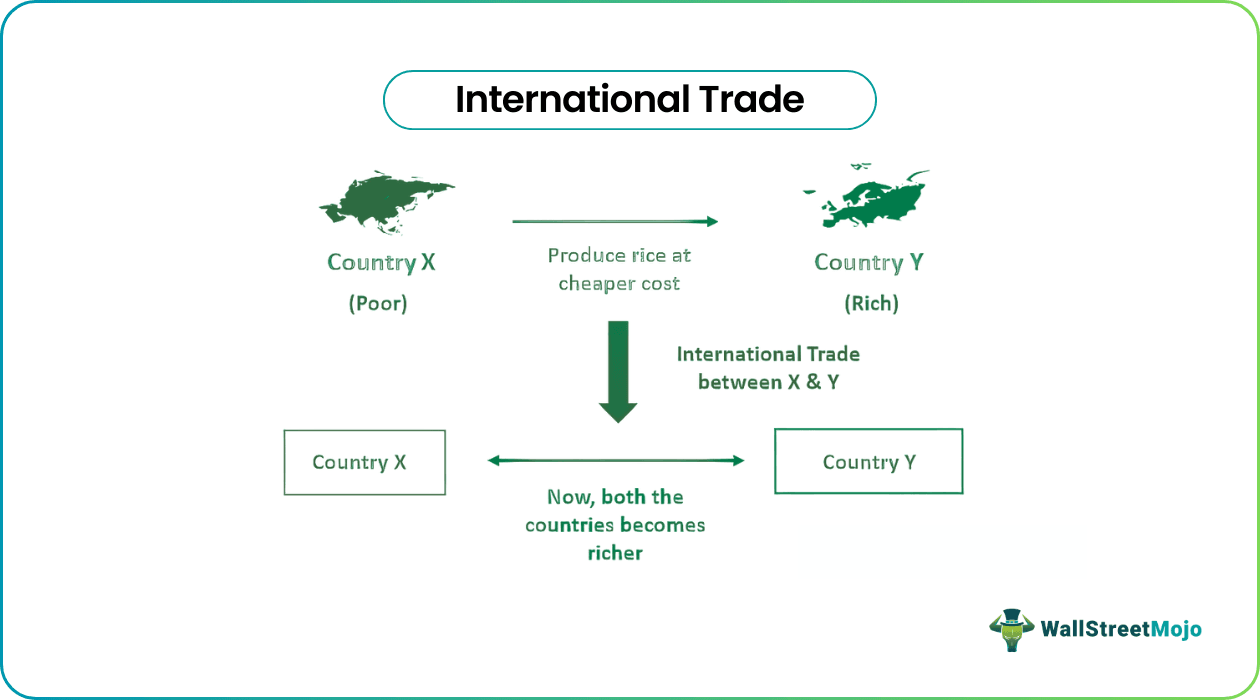

Let us assume that there are two countries, X and Y. X produce rice at a very low price (in comparison to Y). X is a developing nation. Y, on the other hand, cannot grow rice on its land despite having a flourishing economy—due to the unfavorable climate and soil.

In such a scenario, international trade takes place between X & Y. To fulfill domestic demands, Y can buy as much as it needs from X. Likewise, by selling its excess yield to Y, X gains monetarily.

Example #2

In 2022, Europe started importing natural gases from Qatar instead of Russia. Before the war, Russia fulfilled almost 40% of Europe’s natural gas requirements. Consequentially, Qatar has signed various long-term contracts with the US (natural gas imports).

Importance

In the global era, international trade has bridged the gap between producers, sellers, and consumers.

Comparative Advantage: Through international trade, a nation gains expertise in a particular product or service and develops a reputation. For instance, the US has a comparative advantage in capital goods.

Global Development and Economic Growth: An increase in cross-border commerce boosts the local economy of the involved countries.

Attaining Economies of Scale and Specialization: As the demand for imported goods from a particular nation increases—the country becomes well known for the particular product—production is ramped up. The producing country brings down the cost of production by achieving economies of scale.

More Choices for Consumers: When the market is flooded with imported goods and services, the buyers have more options to select from. Customer decisions are dictated by preference and purchasing power. Increased options also mean more competition for the producers—increased product innovation and product quality.

Access to Abundant Raw Material: Many nations lack a particular resource that is required for manufacturing goods. Via international trade, even the rarest natural resources can be acquired.

For example, to manufacture batteries used in electric vehicles cobalt is required; 70% of the world's cobalt is found in the Republic of Congo. But, through international commerce, other countries can acquire the mineral.

International Trade Benefits and Drawbacks

The benefits of international trade are as follows:

- Price Stability: When the goods or services are exchanged globally, their prices standardize in the international market.

- Enhances Technological Know-How: There is an exchange of technology between countries—which also contributes to GDP.

Let us now go through the various problems caused by cross border commerce:

- Adverse Effect on Domestic Consumption: The import of goods or services from foreign countries results in the falling demand for local products. Domestic players may suffer drastically.

- Political Influence: Sometimes, trade is dictated by political agenda—it does not benefit the economy.

- Environmental Cost: When a nation receives foreign direct investment, increased production can cause environmental issues—global warming, carbon emission, air pollution, and water pollution.

Frequently Asked Questions (FAQs)

Cross-border commerce is crucial for the economic growth of a nation; it brings comparative advantage, opens new avenues for local traders and artisans, facilitates economies of scale, and provides access to rare natural resources available.

Barriers to international trade are as follows:

- Natural obstacles like language, distance, etc.

- Tariff barriers—import duty, export duty, or anti-dumping duty.

- Non-tariff barriers—embargoes, government restrictions on imports, and import quotas.

Popular trade theories include:

1. Mercantilism

2. Absolute Advantage Theory

3. Comparative Advantage Theory

4. Country Similarity Theory

5. Global Strategic Rivalry Theory

6. Modern or Firm-Based Trade Theories

7. Porter's Diamond of National Competitive Theory

8. Product Life Cycle Theory

Recommended Articles

This has been a guide to International Trade. We discuss international trade definition, meaning, theory, benefits, & economics using examples. You can learn more about economics from the following articles –