Part of our Financial Statements guide

What is MD&A (Management Discussion and Analysis)?

MD&A, or Management Discussion and Analysis, is the part of financial statements where the company’s management discusses the company’s performance in the current year using qualitative and quantitative measures to help the investor realize the details that otherwise would not have been available for analysis. The MD&A section includes various topics, including the Macro-Economic Performance of the industry, the Company’s Vision and Strategy, and some key financial indicators and their rationale.

As an investor, that is very insightful information provided by a company to co-relate macroeconomic parameters and the company’s performance in light of them. The section containing Management Discussion and Analysis is included in companies’ annual reports. A similar section analyzes the company’s performance and decodes the financial ratios and various indicators for the investors.

- MD&A stands for Management Discussion and Analysis. It is a part of the financial statements where the company’s management provides a qualitative and quantitative analysis to help investors understand details that may not be readily available for analysis.

- MD&A covers various topics, including the industry’s macroeconomic performance, the company’s vision and strategy, and key financial indicators with explanations for their rationale.

- MD&A provides investors with useful information, and its content and presentation can reflect good corporate governance practices and foster a strong relationship between the company and its investors.

What details must You look at in MD&A?

The corporate world has adopted the MD&A route to demonstrate its commitment to the Company’s vision and strategy and how the management has created value and delivered a performance in light of their long-term goals. Hence, MD&A not only dissects financial figures/results but also looks into the business’s human resources and operations side, which are fundamental factors to any business organization. When the term management is referred to throughout this topic, it will involve the complete structure of the organization, including the Board of Directors, Chief Executive Officer, and other Chiefs, their reporting officers/controllers of various departments – Human Resources (People), Finance, Marketing, Production, and Operations, etc. and the remaining middle and lower management levels.

# 1 – Executive Overview and Outlook

The executive Overview and Outlook section focus on the business details, segments, and geographies. It also provides details on the focus areas of the management and how they look forward to achieving the business and financial accounting objectives.

source: Colgate SEC Filings

- Colgate uses a variety of indicators to measure business health. These include market share, net sales, organic growth, profit margins, GAAP and Non- GAAP income, cash flows, and return on capital.

- Colgate also notes that it expects global macroeconomic and market conditions to remain highly challenging and category growth rates to continue to be slow.

# 2 – Discussion on Results of Operations

In this section, the company discusses key Highlights of the current fiscal period’s financial performance. In this, the management provides details of net Sales, Gross margins, Selling General and Admin Costs, Income taxes, etc. Also, it provides details of any Dividend declared and its payment details.

source: Colgate SEC Filings

- Colgate’s Net Sales were down 5% in 2016 compared to 2015 due to a volume decline of 3% and a negative foreign exchange impact of 4.5%.

- Colgate notes that Organic sales of the Oral, Personal, and Home Care product segment increased by 4$ in 2016.

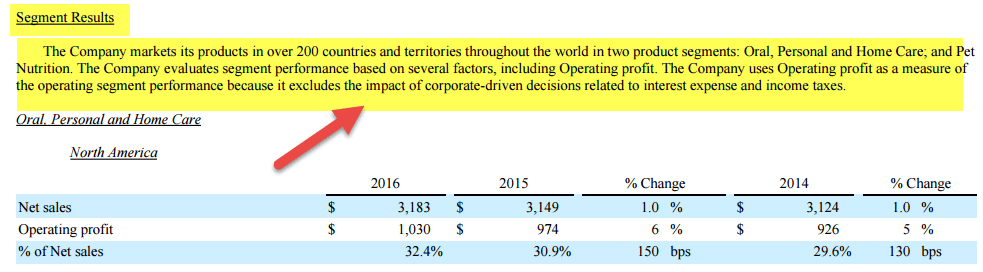

# 3 – Discussion of Segment Results

The company also provides details of its segment, its contribution to the overall sales, growth rates, and other performance measures.

source: Colgate SEC Filings

Colgate operates in over 200 countries with primarily two segments – Oral, Personal, and Home Care; and Pet Nutrition.

# 4 – Non – GAAP Financial Measure

Generally, the company uses Non-GAAP measures for internal budgeting, segment evaluation, and understanding of overall performances. Therefore, the management shares this information with the shareholders to get better insights into the company’s financial performance.

source: Colgate SEC Filings

The above table provides a reconciliation of Net Sales Growth (GAAP) to Non-GAAP measures for Colgate.

# 5 – Liquidity and Capital Resources

This section provides details of cash flow debt issuances that will help meet the business operating and recurring cash needs.

source: Colgate SEC Filings

Colgate generated a Cash Flow from Operations of $3,141 million in 2016 and its cash flow from investing activities was $499 million. Additionally, cash flow from Financing Activities was an outgo of $2,233 million in 2016.

Additionally, Long-term debt, including the current portion, decreased to $6,520 in 2016

# 6 – Off-Balance Sheet Arrangements

This section provides details of any off-balance sheet financing arrangements that the company has entered into.

As we note above, Colgate does not have any off-balance sheet financing arrangements.

# 7 – Managing Foreign Currency, Interest Rate, Commodity Prices and Credit Risk Exposure

In this section, the company discloses how it manages its currency risk, interest rate risks, and price fluctuations.

source: Colgate SEC Filings

- Colgate manages its foreign currency exposures through cost-containment measures, sourcing strategies, selling price increases, and hedging certain costs to minimize the impact on earnings of foreign currency rate movements.

- The Company manages its mix of fixed and floating-rate debt against its target with debt issuances and by entering into interest rate swaps to mitigate fluctuations in earnings and cash flows that may result from the interest rate volatility.

- Futures contracts are used on a limited basis to manage volatility related to anticipated raw material inventory purchases.

# 8 – Critical Accounting Policies and Use of Estimates

In this section, the company management discusses critical accounting policies that have a meaningful impact on the financial representation of the company’s health.

source: Colgate SEC Filings

As we note above, Colgate uses both FIFO and the LIFO method for inventory valuation.

From the details mentioned above, a fair idea can be taken to what kind of information and disclosures in today’s corporate world are required to make them accountable to the investors’ community and society at large and transparency in the reporting. Since the management is well positioned than the stakeholders, who are the outsiders to provide information regarding the performance of the Company, based on such management’s analysis, only certain present actions taken by the Company can be justified, and the management can demonstrate a walk towards their committed goals.

Video Explanation of MD&A

How does it help?

MD&A helps in understanding the operational and financial results in a better light. MD&A has certain definite objectives, which are as follows:

- They are enabling the readers of the financial statements to understand in a better way the numbers and financial condition and to get into management’s shoes to understand certain strategic and operational decisions that are bold and largely impact the future performance and position of the Company.

- Additional supplementary/complementary information provided in MD&A will help readers understand what exactly the financial statements depict and what is not reflected.

- Addressing the investors’ perception of the risks associated with the business operations and outlining past trends to indicate the management’s efforts towards mitigating those risks and leading the path towards future financial statements.

- Though not mandated to be disclosed in the financial statements, there might be certain information. Its additional reference and disclosure by the management can be of added value for the stakeholders’ informed decision-making, including Government authorities.

Government authorities, ranging from the Taxation authorities to capital market watchdogs to fiscal policy makers to banking regulators, etc., try to formulate the operational, fiscal, and monetary policies not only based on the quantitative information provided by the Corporate through financial statements but also based on the qualitative information mentioned in the Management Analysis section on the economy and the industry performance and their future goals.

What serves as the objective of MD&A is the benefiting factor to the stakeholder community. First-time investors in the equity markets can adopt qualitative and informed decision-making based on the information provided by the company’s management in their annual reports.

Format and Extent of information that MD&A should reveal:

As you can note from the objectives mentioned above and governing regulations in India, there is a prescribed and constant practice of presenting the information in the annual report. However, neither is there any comprehensive reporting format prescribed by the Government nor can we notice any universal practice of disclosing such information among various companies from various industries or countries. Hence, the accounting professionals and the governing institutions acting in the respective countries might guide the presentation of MD&A.

For example, the Federal Accounting Standards Advisory Board (FASAB) in the United States has issued a recommended accounting standard on the Management Discussion and Analysis, with the first draft published in January 1997, which can be accessed using the following link – FASAB standard on MD&A. There is no standard or guidance note in India on this behalf; however, the Institute of Company Secretaries of India (ICSI) has issued Reference Note on Board’s Report under their Companies Act 2013 series but leaving MD&A presentation to the interpretation of the industry.

So, taking the FASAB standard for our understanding purpose, MD&A should address the following:

- The entity’s mission and organizational structure;

- The entity’s performance goals and results;

- The entity’s financial statements;

- The entity’s systems, controls, and legal compliance; and

- The future affects existing, currently-known demands, risks, uncertainties, events, conditions, and trends.

Taking a note from another prominent institution’s guidance on Management Discussion and Analysis (originally published in November 2002), the Canadian Performance Reporting Board has laid down certain principles based on which MD&A should be prepared. Those principles are as follows:

- Through the Eyes of Management: A company should disclose information in the MD&A that enables readers to view it through the eyes of management.

- Integration with Financial Statements: MD&A should complement, as well as supplement, the financial statements.

- Completeness and Materiality: MD&A should be balanced, complete, and fair and provide information that is material to the decision-making needs of users. FASAB has described this requirement, saying MD&A should deal with the “vital few” matters.

- Forward-Looking Orientation: A forward-looking orientation is fundamental to useful MD&A reporting.

- Strategic Perspective: The MD&A should explain management’s short-term and long-term objectives strategy.

- Usefulness: To be useful, MD&A should be understandable, relevant, comparable, verifiable, and timely.

Consolidating what we have learned till now, let it be FASAB in the USA or Canadian Performance Reporting Board in Canada or ICSI in India, every governing agency has tried to foster the stakeholder’s informed decision-making function by guiding the corporate world on how the investors can step up and look the situations from the management’s point of view. A good corporate governance practice exercised by a company will always try to improve its information dissemination function to improve its relations with various stakeholders and society.

Differences Between MD&A & Audited Financials

As per SEC, an independent accounting firm should perform an annual audit of a company’s financial statements and provide an opinion on any material misrepresentations. However, auditors are not required to audit the Management Discussion and Analysis section. MD&A section in SEC Filings are the opinions of the management about the company’s financial and business health and provide details of its future operations.

Conclusion

In light of the increased participation of retail and foreign investors in the capital market in recent years, a more comprehensive and transparent mechanism of information dissemination is always required. MD&A must provide insightful and sufficient information to the stakeholder community to analyze companies based on their performance and help better mobilize the capital. It is more required in India, especially after the Economic Survey of 2017 depicts India as the beckoning sweet spot in the darkness of the world economy.

MD&A is one of the very efficient ways to provide meaningful and highly useful information to investors. Improvements in MD&A and its presentation format will lead to good corporate governance practices and a healthy relationship between companies and the investor community.

Frequently Asked Questions (FAQs)

1. Do nonprofit organizations do MD&A?

Nonprofit organizations are not required to include Management’s Discussion and Analysis (MD&A) in their financial statements under generally accepted accounting principles (GAAP). Furthermore, MD&A is typically associated with for-profit organizations and provides management’s perspective on the financial performance and outlook of the company.

2. What is md&a vs. notes to financial statements?

MD&A (Management’s Discussion and Analysis) is a section of a company’s financial statements that provides management’s perspective on the financial performance and outlook of the company. It includes analysis, explanations, and insights into the company’s financial results and operations. On the other hand, Notes to Financial Statements are additional disclosures that provide detailed information about the company’s accounting policies, financial instruments, contingencies, and other relevant information.

3. What are the potential legal implications of including misleading or false information in the MD&A?

Including misleading or false information in the MD&A section of financial statements can have serious legal implications, including potential violations of securities laws, regulations, and other legal requirements. In addition, it may lead to legal actions, such as lawsuits, fines, penalties, reputational damage, and potential liabilities for the company’s management team for negligent or fraudulent misrepresentations.

Recommended Articles

For more on Financial Statements, explore these related articles from our Financial Statements guide.