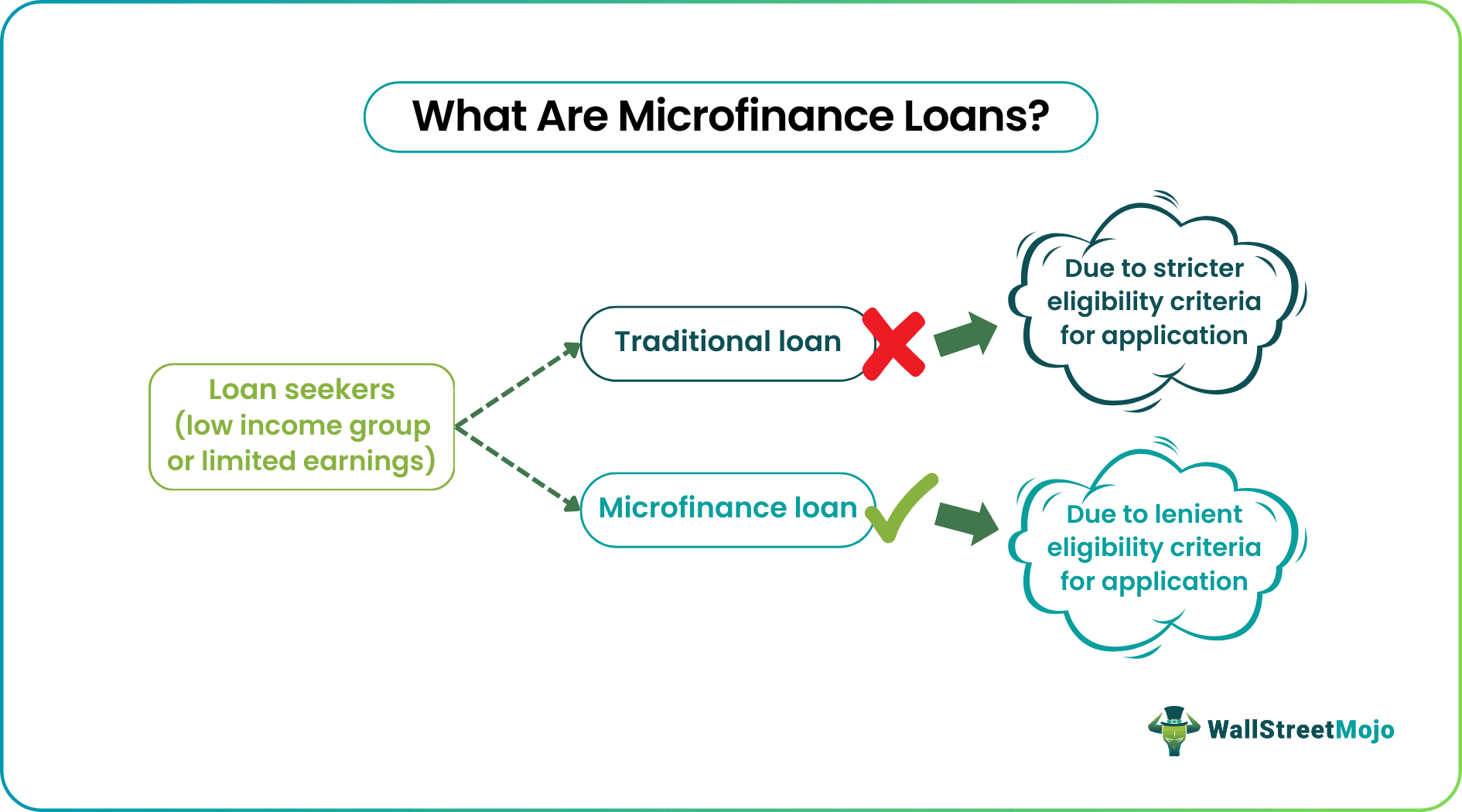

What Are Microfinance Loans?

Microfinance loans are financing options that help people with low or no regular income gather funds to meet their financial requirements. These alternatives have been introduced for those who are not eligible to apply for conventional loan options that come with stricter criteria.

Microfinance loans can be used for fulfilling both personal and business financial commitments. It helps start-ups with limited resources build capital while enabling individuals with limited income to have a self-sufficed lifestyle. There are microfinance institutions (MFIs) to look into the needs of these individuals or groups of individuals and offer them the required financial assistance.

- Microfinance loan is a category that specifically caters to the needs of people from lower-income groups and those with marginalized earnings.

- The administrative costs for these loans are huge. Hence, the lenders charge higher interest rates to cover the administrative costs of these short-span loans.

- These microcredit options help ensure a financially stable population all across the region it operates and also boost entrepreneurial activities around.

- The institutions that offer these loans are known as microfinance institutions.

How Do Microfinance Loans Work?

Microfinance loans are for those who do not qualify for traditional financing options or cannot access other available loan alternatives due to stricter eligibility criteria. Microfinancing allows individuals from low-income groups or with limited earnings to open savings accounts, enjoy fund transfers, get microcredit facilities, etc.

Muhammad Yunus, an economist from Bangladesh, introduced micro finances in 1976 as he thought this option would help the financially marginalized population of the society gain financial freedom. Moreover, while individuals get these loans to fulfill their requirements, start-ups use this financing as working capital loans.

The MFIs that offer these loans initially started as non-profit organizations. But since there’s a huge need for funding in developing countries, continuing as a non-profit venture hardly worked, making it difficult for them to sustain. Hence, they turned into for-profit firms.

The interest rates on microfinance loans are higher than the usual financing options. This is due to the risk the lenders take by offering funds to the economically weaker sections of society. The more the risk, the higher the interest rate is. In addition, the administrative costs for these loans are huge, i.e., around 10-15% of the loans. And since the loans are given for a very short duration, the institutions try to cover the administrative costs with higher interest rates.

Fluctuation in currency and inflation are also the major causes the financial institutions to lose money. Hence, they keep minimum operational profits for themselves, which covers around 5-10% margin. As a result, currency fluctuation and inflation don’t increase their losses. However, they affect the interest rates of the microcredit options significantly.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

These loans operate based on two models, categorizing the finance options into two types of microfinance loans. The first is a relationship-based model, and the second is a collective model. The former helps entrepreneurs and small businesses get their loans approved due to the cordial terms they establish with the bank. On the contrary, the latter lets the services get facilitated for a group of people when they apply for the loan collectively.

Microfinance Loan Video Explanation

Examples

Let us consider the following microfinance loans examples to understand the concept better:

Example #1

Shelly plans to expand her home business and buy a business unit. However, she requires significant funds to purchase a commercial unit. As she did not have proof of her regular income, the lenders considered her ineligible for the conventional loan. The owner learned about the microcredit option and applied for the same. To her surprise, the loan terms were lenient enough. She applied for the same to proceed with setting up her first unit.

Examples #2

Recently, a report depicted how start-up Eskala, which spun off from Global Brigades, a non-profit firm, intends to implement the micro-equity strategy to take up equity positions in the ventures invested in rather than involving the loan complications. The parent company adopted the same attempt a few years ago, whereby it received a grant of $98,000 from the World Bank to address the economic development activities in rural Central America. This work involved a micro-equity strategy, letting banks take small equity positions against the growth capital they provided without any loan complications.

Advantages & Disadvantages

Microfinance loans help many low-income groups become financially stable with respect to their personal and professional requirements. However, one must be aware of a few risks involved in facilitating these financing options. Knowing the advantages and disadvantages helps one understand microfinance loans definition better. So, let us have a quick look at them:

| Pros | Cons |

|---|---|

| Helps make weaker economic sections of society financially independent | Higher interest rates on the loans |

| Boosts entrepreneurship and start-up ecosystem | Lenders may take advantage of the situation. |

| Encourages people to opt for financial education to understand the schemes properly | |

| Best for those who stay in remote locations and cannot access other financing alternatives |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

How to apply for microfinance loans?

Like any other loan option, the loan seekers require filling in the application form and submit the required documents to back the important information. As soon as the application is submitted, the lenders undergo a detailed verification and contact them to discuss further.

How are microfinance loans paid back?

The repayment process is the same for these loans. For example, if $10,000 is to be paid within 30 weeks, the interest charged is $625. The borrowers, in this case, must pay the interest every month until they pay back the principal in full.

Are microfinance loans good or bad?

Of course, these loans are good as they allow individuals to fulfill their financial requirements despite belonging to a lower-income group. In addition, these alternatives help people build capital to fulfill their entrepreneurial dreams without facing loan approval difficulties. Unfortunately, however, this lenient approval sometimes becomes a lender’s way of taking advantage of a borrower’s situation.

Recommended Articles

This has been a guide to what are Microfinance loans. Here we explain how they work, their types, advantages, disadvantages, and examples. You may also have a look at the following article to know more about Corporate Finance –