Part of our Balance Sheet guide

Real Accounts Definition

Real Accounts do not close their balances at the end of the financial year, but the same retains and carries forward their closing balance from one accounting year to another. In other words, the closing balance of these accounts in one accounting year becomes the opening balance of the succeeding accounting year. These accounts are also called permanent accounts.

The golden rule that applies to a real account is that the organization should debit what is coming in the organization and credit the items going out of the organization.

Examples of Real Accounts

The following are the items present in the company’s financial statement that are considered to be examples.

#1 – Assets

Any resource of the business organization that is owned by the organization and has a monetary value that can help generate revenue and is also available to meet the organization’s liabilities are the assets of the business. The assets are further classified into two different categories, which are as follows:

- Tangible Assets: The assets that can be seen or touched are considered tangible assets. Tangible assets include cash, furniture, inventory, building, machinery, etc.

- Intangible Assets: The different assets that cannot be felt or touched are considered intangible assets. Examples of intangible assets include patents, goodwill or trademark, etc.

#2 – Liabilities

These are the legal and financial obligations an organization owes to someone else. Examples of liabilities are loans payable, accounts payable, which include creditors, bills payable, etc.

#3 – Stockholder’s Equity

Shareholders Equity is the value of assets that are available for the company’s shareholders after the payment of the due liability. Examples of the same are retained earnings, common stock, etc.

Journal Entries of Real Accounts

→ Explore all 30 Journal Entries articles

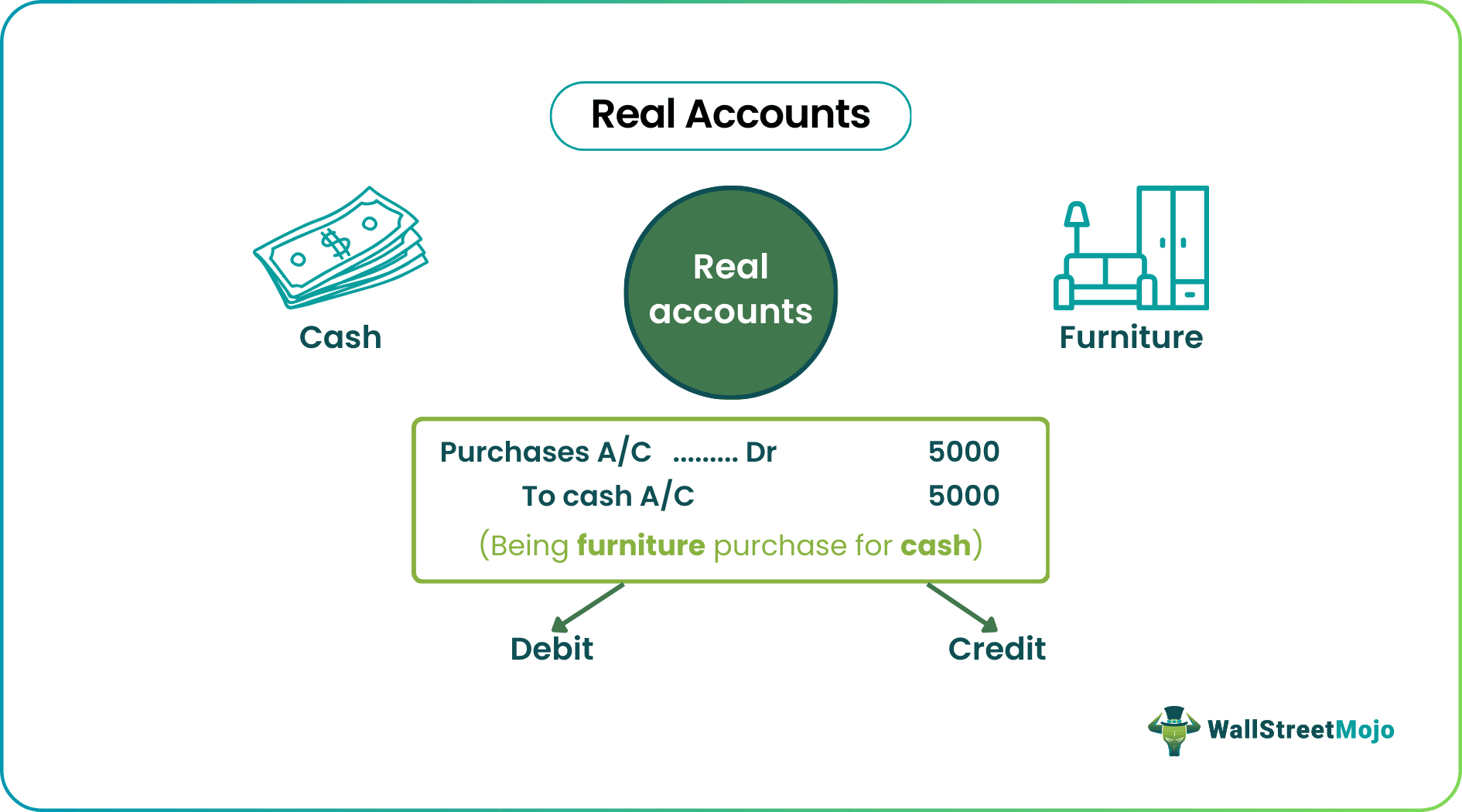

Let’s take the example of Mr. X, who has a business in purchasing and selling the different mobile phones in the area where its business is situated. In the business, he purchased furniture, having a value of $5,000, by paying cash for the same. To analyze the same, consider the real accounts.

In the case of the above example, the journal entry for the transaction in the books of accounts of Mr. X will be as follows:

| Particulars | Amount |

|---|---|

| Furniture A/C …..Dr | $5,000 |

| To Cash A/C | $5,000 |

There is an interaction between two different assets, i.e., furniture and the cash account, classified as real accounts in the above journal entry. Firstly, the furniture account is debited as per the rule, i.e., debit what comes in, and the cash account is credited as per the rule credit that goes out. Then, both are reported on the balance sheet of the company.

Advantages

The advantages are as follows:

- It becomes easier to do journal entries because of the rule of debit what comes in and credits what goes out as it clarifies on which side, i.e., on the debit side or the credit side, is needed to be posted.

- It provides the closing balance of the assets and liabilities reported in the balance sheet and then carried forward in the next accounting year.

Disadvantages

The disadvantages are as follows:

- If there is an error in the closing balance of the real accounts in any accounting year, then the same error gets carried forward in the next accounting year. The closing balance of one accounting year is the opening balance of the succeeding accounting year.

Important Points

The different important points are as follows:

- These accounts are shown on the organization’s balance sheet, which reports the stakeholder’s equity, liabilities, and the business’s assets.

- The word ‘Real’ refers to these accounts’ permanent and perpetual nature. These accounts remain active from the beginning of the business until its end.

- The golden rule that is applicable is that the organization should debit what is coming in the organization and credit the items going out of the organization.

Conclusion

Real accounts, also known as permanent accounts, are the account balances carried from one financial year to another accounting year. i.e., the closing balance in one accounting year of the company becomes the opening balance of the succeeding accounting year in its balance sheet. Examples include the assets, liabilities, and the Stockholders equity. It remains active from the beginning of the business until its end. As a result, it is possible to have a temporary zero balance in some of these accounts.

Recommended Articles

This article has been a guide to what is Real Accounts and its definition. Here we discuss components of real accounts along with an example, advantages, and disadvantages. You can learn more about accounting from the following articles –