What is Income Summary?

An income summary is a temporary account in which all the revenue and expenses accounts’ closing entries are netted at the accounting period’s end. The resulting balance is considered a profit or loss. Once the entries are finalized, the income summary closing entries are documented and transferred to the retained earnings of an organization or individual.

If the net balance of the income summary is a credit balance, it means the company has made a profit for that year, or if the net balance is a debit balance, it means the company has made a loss for that year. It summarizes income and expenses arising from operating and non-operating activities. Therefore, it is also called a revenue and expense summary.

- An income summary refers to a temporary account in accounting. All closing entries about the company or firm’s revenue and costs are entered into this account at the end of the accounting period. Afterward, the resultant balance is known as a profit or loss.

- The business was profitable that year if there was a credit balance in the income summary net balance. A debit balance, on the other hand, indicates a loss for the business.

- It is a vital tool for making financial statements and functions as a checkpoint. Also, it eliminates errors while preparing the financial statements by directly transferring the balance from revenue and expense accounts.

Income Summary Explained

An income summary is a summary of Income and expenses for a specific period, and the result of this summary is profit or loss. It is an essential tool for preparing financial statements. It works as a checkpoint and mitigates errors in preparing financial statements by directly transferring the balance from revenue and expense accounts.

Instead of sending a single account balance, it summarizes all the ledger balances in one value. It transfers it to a balance sheet, which gives more meaningful output for investors, and management, vendors, and other stakeholder. An income summary account summarizes all the operating and non-operating business activities on one page and concludes the company’s financial performance.

This account follows the double-entry system of bookkeeping. As in, it has a debit side and a credit side. If the credit side is greater than the debit side, the company or the individual is said to have been profitable in the assessment period. In contrast, when there is a loss incurred, the debit side has more value than the credit side of the account.

It is also commonly found that an income summary is confused with an income statement. Despite the fact that both provide insights into the financial health of an organization or an individual, the former is a temporary account and the latter is a permanent account. Moreover, the entries in the income statement are finally transferred into the income summary after which, the deductions are made.

How to Calculate?

Let us understand how income summary closing entries are passed. Before passing those entries, there are a few processes and steps to be followed to reach that stage. Let us understand how to calculate the income of a company or an individual through the discussion below.

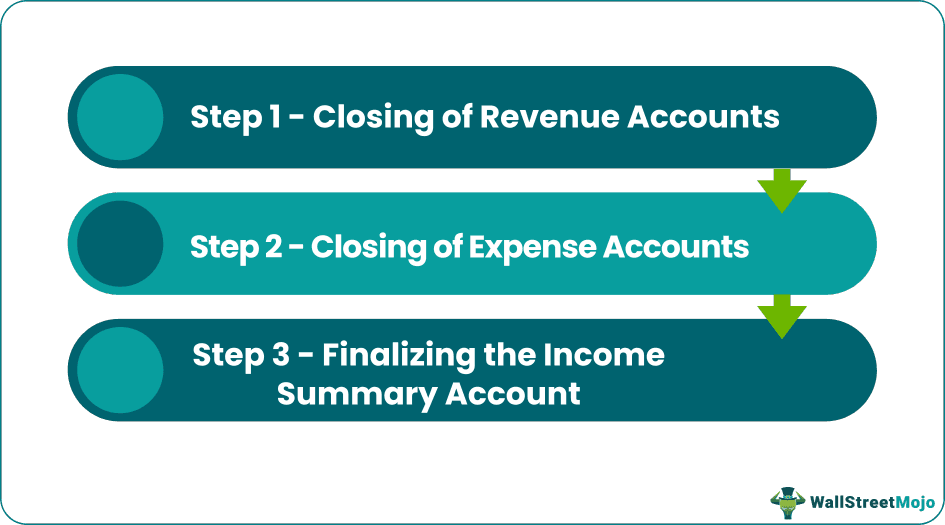

Step 1 – Closing of Revenue Accounts

Revenue accounts always have credit balances. At the end of the accounting period, all the revenue accounts will be closed by transferring the credit balance to the income summary. It will be done by debiting the revenue accounts and crediting the income summary account. After passing this entry, all revenue accounts will become zero.

Step 2 – Closing of Expense Accounts

Expenses accounts always have debit balances. At the end of the accounting period, all fees will be closed by transferring the debit to the income summary by crediting the expenses account and debiting the income summary account. After passing this entry, the all-expense accounts balance will become zero.

Step 3 – Finalizing the Income Summary Account

Now, these accounts have all the revenue accounts balance in the credit side column as the total Income of the organization and the expense account balance in the debit side column as the total expenditure of the organization. If the credit balance is more than the debit balance, it indicates the profit; if the debit balance is more than the credit balance, it shows the loss. In the last credit or debit balance, whatever may become, it will be transferred into retained earnings or capital account in the balance sheet, and the income summary will be closed.

Revenue vs Income Explained in Video

Examples

Let us understand the concept of an income summary account with the help of a couple of examples. These examples would give us an in-depth idea about the concept.

Example #1

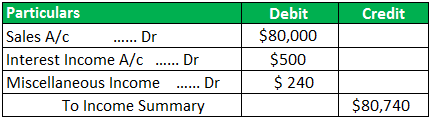

XYZ Inc is preparing an income summary for the year ended December 31, 2018, and below are the revenue and expense account balances as of December 31, 2018.

The closing balance of revenue accounts is as below:

- Sales – $80,000

- Interest Income – $500

- Miscellaneous Income – $240

The closing balance of expense accounts is as below:

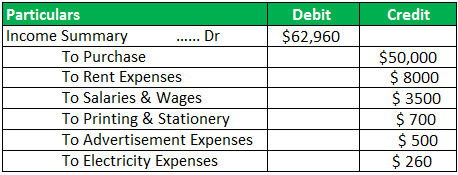

- Purchase – $50,000

- Rent Expenses – $8,000

- Salaries & Wages – $3,500

- Printing & Stationery – $700

- Advertisement Expenses – $500

- Electricity Expenses – $260

Now all the above accounts will be closed by transferring their balances into an income summary with the help of the below journal entry:

Balance of income and expenditure will be transferred to retained earnings by passing the below entry:

After passing the above journal entry of income, the summary account will be prepared as below:

Example #2

Capital One Financial Corporation declared their net income closing entries for the fourth quarter of 2022. It was declared at $1.2 billion or %3.03 for each diluted common share.

Overall, in 2022, their income across all sources accounted for a mammoth $2.4 billion or $5.41 for each diluted common share.

The breakdown of their growth across sectors included:

- Increase in net revenue by 3 percent

- Pre-provision earnings saw an increase of 3 percent

- Non-interest expense increase by $5.1 billion

- Provision for credit losses increased from $747 million to a staggering $2.4 billion.

How To Close?

Closing the income summary account is done after all income sources are accounted as retained earnings of the organization. But before that entry is passed, there are a few steps to the process. Let us discuss the steps through the explanation below.

- Debiting all revenue accounts irrespective of them being direct or indirect incomes.

- Credit all revenue accounts to the income summary account. Therefore, all revenue accounts would be dialed back to zero.

- Since there must be some expense accounts as well, they must be credited, and the summary account must be debited to carry out the same.

- The amount remaining in the summary account can be transferred and accounted as retained earnings to close the account.

Advantages

Let us understand the advantages of passing income summary closing entries for an organization or an individual through the points below.

- It gives the organization’s total revenue and expense information in one place.

- It helps investors and shareholders analyze a company’s financial performance for a specific period to decide on future investments.

- One can track the company’s performance easily by reviewing the income summary of past years to know whether it is making a profit regularly or not.

- It also helps fill income tax returns because it gives all the necessary information in one place.

- It is easily understandable because it has only two columns.

- Income summary helps in budget vs. actual variance analysis.

- It is easy to derive the cash profit by adding or deducting the accrual balances.

Disadvantages

Despite the various advantages listed above, there are a few factors that act as hassles while maintaining an income summary account. Let us understand the disadvantages through the discussion below.

- It includes operating and non-operating revenue and expenses. Therefore, it does not give the correct financial picture of the organization.

- It is prepared on an accrual basis like it records the total sales value, whether money has been received or not, whether expenses have been recorded on an accrual basis, and whether it has been paid or not. Therefore, there is a chance of misrepresentation.

- An income summary of one year is not helpful for financial performance analysis. An investor must take at least ten years of summary to analyze financial performance. Therefore, it is time-consuming and sometimes challenging to get the ten-year summary of the organization, which is not listed.

Frequently Asked Questions (FAQs)

Where do you close the income summary account?

After closing all the company’s or firm’s revenue and expense accounts, the income summary account’s balance will equal the company’s net income or loss for the particular period. In such cases, one must close the owner’s income summary account to their capital account. In a corporation’s case, one must close the retained earnings account.

Is income summary a temporary account?

The income summary is a temporary account where all the temporary accounts, such as revenues and expenses, are recorded.

Does income summary have a normal balance?

The income summary has a normal debit balance. If the company profits for the year, the retained earnings will come on the debit side of the income summary account. Conversely, if the company bears a loss in the year, it comes on the credit side of the income summary account.

Are dividends closed to income summary?

Dividends are close to the income summary and retained earnings. Therefore, the retained earnings account shows the earnings that are kept, net income fewer dividends in the business. Moreover, the closing procedure shows that revenue, expense, and dividend accounts are retained earnings subcategories.

Recommended Articles

This has been a guide to Income Summary. Here we explain the steps to calculate and close the Income Summary account, examples, advantages, and disadvantages. You can learn more from the following articles –