Table Of Contents

What is Interest in Investments?

Interest on investments is the periodic receipt of inflows on financial instruments like bonds, government securities, or bank accounts. It may be income earned from the specified form of liquid assets. The pay-out can be monthly, quarterly, or annually. Therefore, it is essential to keep track of the receipt of interest income. Over time, new models of money lending are evolving, and the receipt of interest income is also modified accordingly.

Key Takeaways

- Interest on investments refers to the periodic inflows receipt on financial instruments such as bonds, government securities, or bank accounts. It can be received monthly, quarterly, or annually.

- The types of interest on investments are bonds like corporate bonds, secured bonds, bank accounts like saving accounts, current accounts, and government securities.

- IFRS 9 recognizes interest income depending on general or simplified and credit-adjusted approaches.

- Interest income is the secured approach to earning income from the financial instrument.

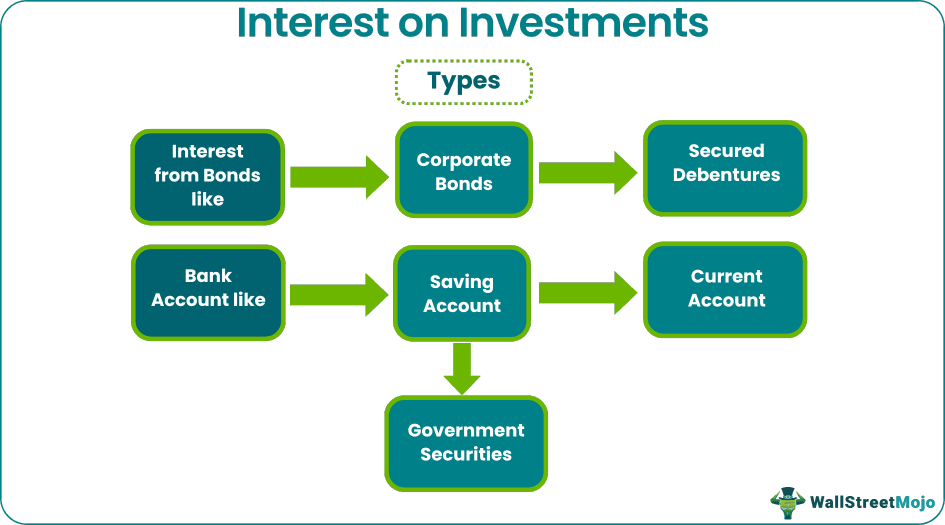

Types of Interest on Investments

The following are the various type of interest on an investment earned from different modes:

#1 - Interest from Bonds like Corporate Bonds, Secured Debentures, etc

Under this, the investor can get an interest in bonds like debentures, corporate bonds, certificates of deposits, etc., for the tenure of holding of respective financial instruments.

#2 - Bank Account like Saving Account, Current Account, etc

Under this, the account holder may get a simple and compounding interest on the balance in the bank account depending on the days of credits available in the bank account.

#3 - Government Securities

Under this, an investor invests in securities issued by various government departments and gilt bonds. Like a corporate bond, investors may get interested based on the financial instrument's tenure.

Formula

Interest Income = P * R * N

When,

- P= Principal

- R= Rate of interest

- N= Period

It is the formula for simple interest. Normally, the bonds and deposits with a regular pay-out market use the above procedure. However, the concept of compounding is applied in bank deposits where the regular pay-out is unavailable. In simple interest, interest is paid periodically, and the principal is repaid.

However, periodic interest is reinvested in compounding and repaid the principal’s cumulative interest at the end of tenure. At the end of the tenure, one may repay cumulative interest and the principal. Compounding is generally seen in mutual funds, where systematic investment plans are kept on investment, and the return on the same is accrued and reinvested.

Interest in Investments Examples

Below given are the examples: –

Example #1

ABC Ltd. invested $10,000 in the bonds of the Fed for five years. The rate of interest in the bond is 5%.

You are requested to calculate:

- Interest income earned by ABC Ltd.

- The total amount that ABC Ltd. will receive post-maturity of the bond. You are requested to calculate:

Solution:

- P= $10,000

- R= 5%

- N= 5 years

Calculation of interest earnings:

= $10,000 * 5% rate of interest * 5 years

Interest-earning will be –

- Interest-earning = $2,500

Amount = Principal + Interest

- Total amount = $12,500

Thus, ABC Ltd. earns an interest of $2,500 with bond investment and receives $12,500 post-bond maturity.

Example #2

Mr. Jackman invested $8,000 in bank deposits for 40 days with Deutsche Bank. The rate of interest on the deposit is 10%. Accordingly, you are requested to calculate the interest income for Mr. Jackman.

Solution:

- P= $8,000

- R = 10%

- N = 40 days

Calculation of interest-earning:

= $8,000 * 10% * 40 days / 365 days

Interest-earning will be –

- Interest-earning = $87.67

Thus, Mr. Jackman will earn $87.67 as interest from the investment in the deposit.

Advantages

- Fixed-rate of interest – One of the best advantages of interest income is providing steady earnings with a fixed rate for a specified period.

- Tax saving benefit – Interest income over departmental government bonds is tax exempted. Hence, one can enjoy earnings and tax exemption.

- Safe mode of earning – Earning interest income is one of the safest modes of earning compared to other investment options because of the risk profile of the investment.

Disadvantages

- Low-interest rate – Compared to other investment alternatives, interest-bearing securities give the least return because the rate is fixed and does not increase with time and the inflation effect.

- Charges/ fees – Often, charges/fees are auto-deducted from the account in financial charges. It gives a negative return to investors.

IFRS Requirement to Recognize Interest Income

IFRS 9 will recognize interest income based on general or simplified and credit-adjusted approaches.

A detailed description is given below:

General or Simplified Approach

| Descriptions | No evidence of impairment exists | Evidence of impairment exists | Credit adjusted approach |

|---|---|---|---|

| Interest income is calculated based on | The carrying the value of the assets at the beginning of the period. | The carrying value of the assets at the beginning of the period is adjusted with credit risk. | The carrying value of the assets at the beginning of the period is adjusted with credit risk. |

| The rate of interest is applied based on | The effective rate of interest. | The effective rate of interest. | The effective rate of interest is adjusted with credit risk. |

The effective interest rate is the rate that discounts all expected future cash outflows/inflows from the financial instrument at the asset’s amortized cost preceding any allowance for expected credit losses.

Conclusion

Interest income is a safe way of earning income from the financial instrument. Moreover, it has the power to give enduring income at a fixed rate without any stoppage. With time, innumerable innovative models of investment have come. These provide the support of income with the effect of inflation.

Interest is a good and secure source of income for corporations, even though the interest rate is not so high.