Part of our Revenue Recognition guide

What is Accrued Income?

Accrued Income is the income the company has earned in the ordinary course of business after selling the goods or after the provision of the services to the third party but the payment for which has not been received and is shown as an asset in the balance sheet of the company.

Accrued Income is the income earned by the company or an individual during the accounting year but not received in that same accounting period.

It can be any income for which the company gave goods and services to the customer, but customer payment is pending. Sometimes this income can also be applied to revenue generated for which a bill is not issued by the entity yet. Also, it has not been paid yet.

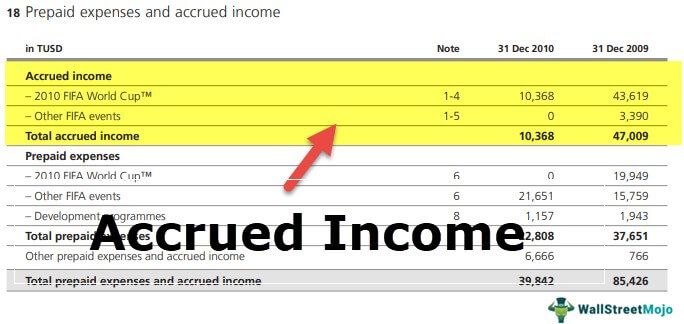

We see from the practical example of Accrued income treatment in the FIFA Financial Report 2010. We note that this income for FIFA in 2010 and 2009 was TUSD 10,368 and TUSD 47,009, respectively.

Accrued Income Examples

There are different types of ways through which it can take place in any business:

#1 – Investment

Accrued income can be the earning generated from an investment but yet to receive.

For example, XYZ company invested $500,000 in bonds on one march in a 4% $500,000 bond that pays interest of $10,000 on 30th September and 31st March. XYZ invested the amount on the 1st of March, but as it was the first month, the company didn’t receive an interest income of $1,667(i.e., $10,000/6) on the 31st of March in the same year. So till 30th September, the amount of $ 1,667.00 is the accrued earnings for the company as the company knows that interest for March has been generated, but it will receive it on 30th September.

#2 – Rent Income

Rent income can be considered accrued income when payment policies differ.

For example, a real estate company gives a building on rent and decides to take the rent from a renter quarterly, not monthly. Here, the treatment of rental income will be as accrued earnings. It is so since rent of two months has been generated, but the company will receive that rent at the end of the 3rd month of the same quarter.

#3 – Income from services

Suppose a service provider company provides its services to the customer, and the customer promises to pay after some time. The payment regarding those services will be treated as accrued income.

Accrued Income Explained in Video

Accrued Income Journal Entries

→ Explore all 30 Journal Entries articles

It is current assets for any business and impact a Balance sheet and Profit & Loss A/c. For this, an accountant needs to pass the journal entry that debits accrued Income A/c and credit Income A/c.

Journal Entry In the income account

It needs to be added to the concerned income in the profit and loss account:

Journal Entry in Balances sheet

In the Balance sheet, it is shown as a separate item under the current asset on the asset side.

Accrued Income Journal Entry Examples

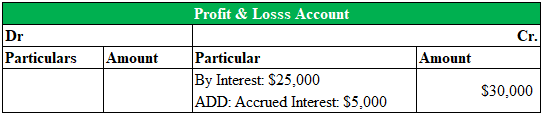

Example #1

Suppose ABC Ltd earned an interest income on the investment of $30,000 in which only $25,000 is received, and $5,000 still needs to be received. Below are the accounts in which this impact of accrued earning can be shown:

For Accrued Interest

For Interest Received

For-Profit & Loss Account

For Balance Sheet

Example #2

Here are some more examples for journal entries:

Abhay Mittal ltd. It gives some space of the building for rent, and the renter agreed to pay the rent monthly. In June, the renter didn’t pay the rent and asked the landlord to pay next month. So, for this scenario, the adjustment entry should be:

Example #3

Jagriti Pvt Ltd lent $10,000 at 10% interest on March 1, 2015. The amount needs to be collected after one year. At the end of March, the journal entered no entry regarding interest income.

Interest is earned over time. In the case above, the company will collect the $10,000 principal plus a $1,000 interest after one year. The $1,000 interest pertains to 1 year.

However, one month has already passed. The company is already entitled to 1/03 of the interest, as prorated. Therefore the adjusting entry would be to recognize $83.33 (i.e., $1,000 x 1/12 ) as interest income.

So in this scenario, the necessary adjustment entry should be:

Recommended Articles

This article has been a guide to What accrued income is and its meaning. Here we discuss Accrued Income Journal Entries and practical examples (investment, rent & other sources). You may also go through our other suggested accounting articles –