Liquidity Preference Theory Definition

The liquidity preference theory of Keynes states the relationship between interest rate, liquidity preferences, and the quantity or supply of money. It explains the preference for money or liquidity and the reason to demand and get a high-interest rate for long-term financial assets.

The founder of Keynesian economics and the father of modern macroeconomics, John Maynard Keynes popularized this concept in his book- The General Theory of Employment, Interest, and Money (1936), explaining the liquidity preference framework analyzing the determination of equilibrium interest rate based on the supply of and demand for money.

- The liquidity preference theory of interest was introduced by the father of modern macroeconomics, John Maynard Keynes, in his book The General Theory of Employment, Interest, and Money (1936).

- The theory focuses on the interest rate, liquidity preferences, and the quantity or supply of money. It explains the association of higher interest rates with long-term instruments.

- The theory explains people’s motives to prefer holding cash rather than investing in interest-bearing securities. The three motives explained by the model are transaction, precautionary and speculative motives.

Understanding Keynesian Liquidity Preference Theory

The liquidity preference theory of interest is a theory of money that explains the monetary nature of the interest rate. Keynes explained that liquidity preference influences the interest rate rather than the saving decision. He believed that money or liquidity is necessary for economic activity in monetary production economies compared to savings.

The individual decides the portion for spending and reserve for future consumption based on income. Also, factors like psychology, uncertainty in the future, and the economy’s structure influence the portion for spending. When it comes to saving for the future, people can hold in the form of cash or investment in interest-bearing assets.

If the demand for cash balance is behavior towards risk, both demand for cash balances and the interest rate will manifest an inverse relationship. If the interest rate is low, people prefer holding cash and vice versa. Also, people prefer a high-interest rate for long-term securities compared to a low-interest rate for short-term securities. It also points to the fact that the interest rate is the price for parting the liquidity or parting the desire to hold wealth in the form of cash.

Keynes portrayed the liquidity preference model in terms of three motives:

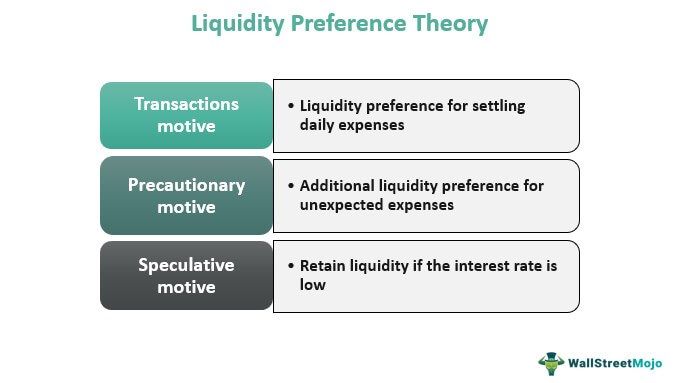

Transactions Motive

It highlights the people’s choice to prefer liquidity for their day-to-day expenses or normal transactions. Investors like to have the liquidity to ensure their short-term obligations rather than struggling or borrowing. The amount of liquidity is directly proportional to the income level. The higher the income is, the more it is used for increased spending. Paying rent, buying groceries, and managing bills are short-term obligations.

Precautionary Motive

Cash plays an important role in everyone’s life, specifically in times of crisis and emergencies. Precautionary demand reflects the need to cover abrupt expenditures, contingencies, or unforeseen opportunities. Hence this is another motive explained by the liquidity preference theory for retaining cash.

Speculative Motive

Speculative motive explains people’s intention to gain speculative profit utilizing changes in interest rates. If the interest rate is low or investors may have a higher demand for liquidity, anticipating a future increase in interest rates, they hold cash for future investment.

Income rather than the interest rate primarily influence the transaction and precautionary motives. That is, they are relatively interested inelastic. Therefore, as income increases, cash reserve for the transaction and precautionary motives increase and vice versa. On the other hand, the speculative motive is interest elastic; it depends on the interest rate. Hence the speculative motive and cash available to satisfy the speculative motive determine the interest rate.

Example

According to the data from the Bloomberg website on 20 April 2022, the US Treasury yields for different length of time is listed below:

3 Months: 0.79%

6 Months: 1.24%

12 Months: 1.89%

2 Year: 2.55%

5 Year: 2.87%

10 Year: 2.89%

30 Year: 2.95%

In the above data, there is no significant increase in the interest rate with the increase in duration; still, the interest rate increase with the increase in the length of time. Normally, longer-duration interest rates are higher than short-duration. It is convinced by the fact that the investors’ cash is locked in for a longer timespan, and they are also exposed to a greater probability that interest rates will change with the duration.

Video Explanation of Liquidity

Limitations

Let’s look into some of the limits exhibited by the liquidity preference theory:

- Little or no focus on the presence of exogenous elements like uncertainty.

- It overlooks the presence of banks and bank money. Neglecting the bank money causes the theory to minimize the capacity of the monetary authorities to influence the interest rates.

- Wealth is an exogenous element whose presence is not explained by the theory.

- The assumption of a constant employment rate.

- The explanation always specifies either hold as cash or invest in bonds or securities. But both acts can perform simultaneously.

Frequently Asked Questions (FAQs)

What is theliquidity preference theory of Keynes?

Keynes coined this theory to replace theories like loanable funds theories of interest. The theory focused on connecting interest rate and liquidity decisions. Rather than saving decisions, liquidity decisions influence the interest rate. Interest rate is portrayed as the price of parting liquidity.

What are the three motives of liquidity preference theory?

According to the Keynes theory, the demand for liquidity is based on mainly the three motives:

Transactional motives: Holding cash for daily expenses and normal transactions

Precautionary motives: Cash for unforeseen expenses

Speculative motives: Retain the liquidity if the interest rate is low

Who gave the liquidity preference theory of interest?

The founder of Keynesian economics and the father of modern macroeconomics, John Maynard Keynes, introduced the theory in his book The General Theory of Employment, Interest, and Money (1936). He described a model explaining the connection between interest rates and preferences to hold cash.

Recommended Articles

This article has been a Guide to Liquidity Preference Theory & Definition in Keynesian Economics. We explain the Liquidity Preference model and framework by Keynes. You can learn more from the following articles –