Part of our Types of Bonds guide

What Is A Catastrophe Bond?

A catastrophe bond (CAT bond) is a type of insurance-linked security (ILS) that helps insurance companies raise the amount for claims in the event of any catastrophe. Here, catastrophe refers to any natural calamity on a large scale. Catastrophe bonds yield high returns, but the risk factor is also high.

The catastrophe bond helps mitigate losses through short maturity periods and its cyclical nature. The bond is an alternative for catastrophe reinsurance, opted for by insurance companies to pay off the insured. The investors receive regular interest payments, and the principal is paid upon maturity, provided no catastrophe occurs.

Key Takeaways

- A catastrophe bond is an investment linked to insurance, which helps the insurers manage the outflow of funds when any natural calamity strikes and claims are made by the insured.

- It can be advantageous to both investors and the issuer. But simultaneously, it can also be disadvantageous, as it depends on the contingency of catastrophes.

- CAT bonds can be a great addition to the investment portfolio, as it doesn’t depend on economic or market conditions, thus facilitating diversification.

- A prominent example is the World Bank catastrophe bond, which indemnifies countries worldwide.

Catastrophe Bonds (CAT) Explained

→ Explore all 63 Bonds articles

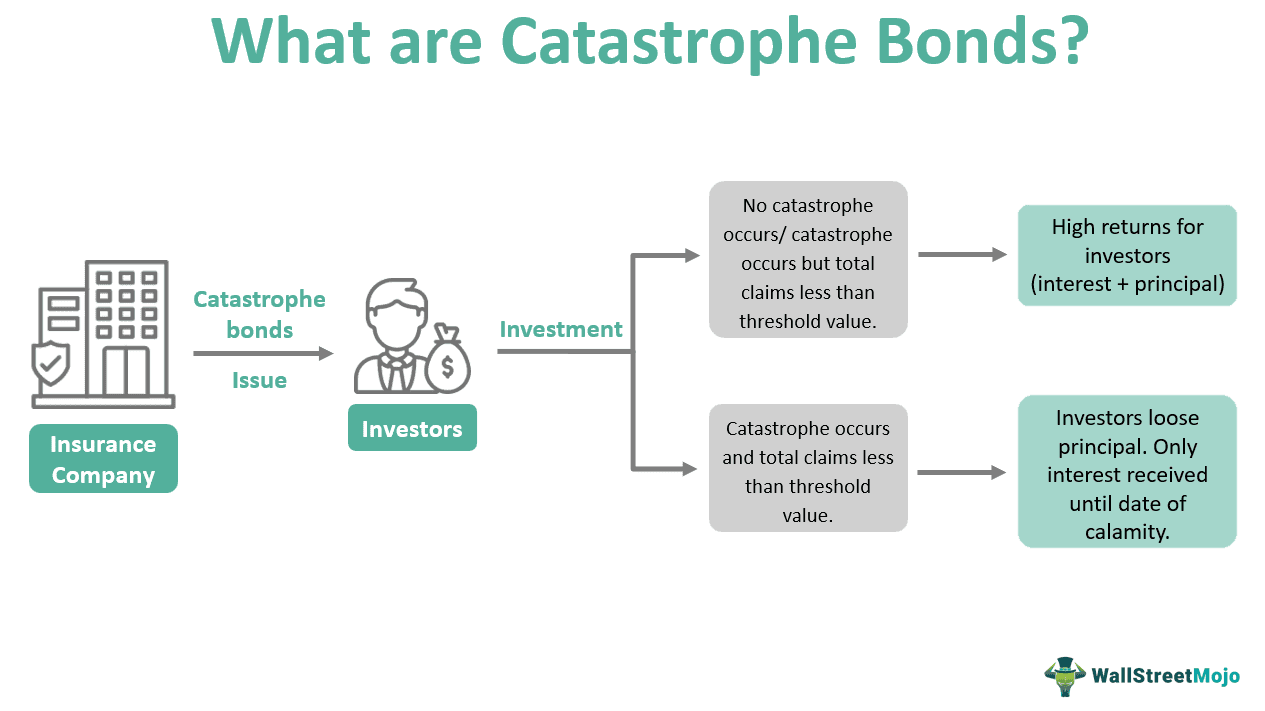

Catastrophe bond funds function as a backstop for insurance companies and help them raise capital to fund claimants’ indemnification. CAT bonds are a simple arrangement between insurance companies and investors.

Usually, when the contingency occurs, the insurance company has to pay off claims. But if it does not have sufficient funds, it is more likely to resort to reinsurance. It approaches another insurance company, raises capital, and forwards it to the claimants. This is a pretty common scenario. However, this puts a lot of obligations on the insurance company. This is because it plays the role of the insured and the insurer. CAT bonds are an alternative to reinsurance.

Insurance companies establish special-purpose entities to issue catastrophe bonds. The total investment amount collected when investors buy these bonds is transferred to a separate account. This amount is often re-invested in another investment which would yield returns for the insurance company. The maturity period of CAT bonds is usually less than three years. In addition, the investors receive regular interest payments for their investments. The insurance company would make this payment from the returns earned by their investment.

During the time of investment, the insurance company specifies a threshold value. If any natural disaster occurs, amounting to losses more than this threshold value, the insurance company will use the total investment amount to indemnify the claimants. Therefore, the investors will face a loss. But they would receive the interest payments until the date of the calamity. Also, the investors will receive an equal share of any balance amount after the indemnification.

However, if such a calamity doesn’t occur, or the net loss of the calamity is lower than the threshold value, the insurance company will have to indemnify the claimant out-of-pocket. Thus, the investors will be entitled to interest payments and the principal amount. Hence, such a case would yield high returns for the investors.

Example

Consider the example of Hurricane Ian, the tropical cyclone that hit Florida in September 2022. This is bad news for investors in Florida’s catastrophe bond market. As a result, many insurance brokers and capital management firms predict substantial losses for CAT bond investors.

As of 2021, the insurance industry had exceeded the $100 billion mark in losses for the fourth time in five years. Hurricane Ian adds to investors’ woe, making the insurance market’s future look grim. The cyclical nature of the CAT bonds helps to give adequate profits and thus motivates the investors. However, continuous losses might discourage them and lead to high insurance costs for commoners.

How To Buy Catastrophe Bonds?

Upon consultation with their investment bankers, insurance companies set up a special purpose entity that would function as the issuer of the bonds. Common investors in catastrophe bonds include hedge funds, pension funds, asset managers, reinsurers, banks, etc. This is because CAT bonds allow portfolio diversification and provide higher returns if no natural disaster strikes.

Further, investing in the catastrophe bond market would be best, provided the investor already has a diversified portfolio. The reason is that if a person wants to invest all their funds into the CAT bonds, they will lose their total investment in the event of a catastrophe. Suppose they have other income sources; they would still profit from other investments even if a calamity occurs.

Pros And Cons

CAT bonds are an arrangement between the issuer and investors such that one of them will surely benefit. However, it is also left to chance and carries some demerits. So let’s examine the advantages and disadvantages of CAT bonds.

Pros

- CAT bonds are usually high-return debt instruments. But as the risk-return relation goes, the higher the return, the higher the risk. Therefore, investors are unlikely to make returns in catastrophe bond funds. However, when they do, the returns will be increased. This high return is what excites and motivates investors.

- It facilitates portfolio diversification to a great extent since its correlation with financial markets is less.

- The short maturity period is an added advantage to investors, as the probability of large-scale calamities costing millions of dollars to insurance companies in a short period is less.

- Another benefit for investors is the specific limit of total claim amounts beyond which the investment amount will be used. Therefore, until the threshold amount is not met, the investors would still profit.

- Considering the insurers’ perspective, they benefit in case a catastrophe strikes. In such situations, they would have to pay an out-of-pocket expense would be less, as the investment amount will cover the claims.

Cons

- Investors will lose the total investment amount if a catastrophe arises. This is because they would only receive the interest until the period before the occurrence of the disaster. Hence, this would result in a total loss for them.

- Even though economic conditions do not affect CAT bonds, if the natural disasters are so strong as to impair the economy, the investors might suffer losses.

- From the issuer’s point of view, they would have to pay the interest payments out-of-pocket if the calamity doesn’t occur. Also, upon maturity, they will have to return the principal amount. Nevertheless, the issuers offset this loss by investing the principal amount elsewhere and making returns from it to pay back investors.

Frequently Asked Questions (FAQs)

How do catastrophe bonds work?

Insurance companies issue catastrophe bonds to investors. The issuer usually specifies the maturity period and the threshold value. Suppose any natural calamity occurs during that period, and the total payout value for the insurance company exceeds the threshold value; the issuer will use the investment amount. Otherwise, the principal amount and interest would be repaid to the investor.

How to invest in catastrophe bonds?

Buying a CAT bond is as simple as investing in another security. Investors can communicate with their investment banker or money manager and express their interest. However, it is important to have other investments in one’s portfolio, to minimize the losses.

What triggers a catastrophe bond?

Any large-scale catastrophe triggers a catastrophe bond. It can be earthquakes, landslides, hurricanes, tornados, tsunamis, floods, etc. Large scale implies the condition where the total payout value exceeds the CAT bond threshold value.

Recommended Articles

This article has been a guide to what is a Catastrophe Bond. Here, we explain the topic in detail with its example, pros, cons, and steps to buy. You may also find some useful articles here –