Part of our Types of Bonds guide

Gilts Meaning

Gilts are bonds issued by the UK government to raise money. Gilt instruments are called “gilts” because they are fixed-income securities with a gilt edge (higher quality). The government issues these bonds and, through the process, borrows money from buyers with a duration stretching from a few months to decades.

Gilts are a popular asset class for investment as they carry less risk than shares and come with a guaranteed payment since the government issues them. As a result, they are a good option for investors with lower risk tolerance and who want to have a balanced portfolio with high, medium, and low-risk investments.

Key Takeaways

- Gilt is a debt instrument of the UK government denominated in sterling. They are low-risk and secure and are referred to as “gold” or “gold-edged security.”

- Government bonds in the UK are known as Gilts, whereas those in the US are known as Treasury Bills, or T-Bills, and German federal bonds are known as Bunds.

- Different types of gilts include Conventional gilts, Index-linked gilts, Three-month lag index-linked gilts, Eight-month lag index-linked gilts, and Gilt strips.

How Do Gilts Funds Work?

Gilt is a debt instrument of the UK government, the denomination for which is in sterling. The HM Treasury issues it, and investors trade it on the London Stock Exchange. They are low-risk, secure, and referred to as “gold” or “gold-edged security.” They are fixed interest-bearing securities. While government bonds in the UK are known as Gilts, those in the US are known as Treasury Bills, or T-Bills, and German federal bonds are known as Bunds.

Investing in such funds offers the investor protection from credit risk. They provide various maturation periods ranging from a few months to several decades. Interest rate risk is a factor in these products, just like in all other bond funds. The government issues them when it needs funds, which means that by issuing these securities, the government is essentially borrowing from the public.

Bondholders receive interest payments during the security’s life period, and the capital invested returns when it matures. The annual interest rates paid as part of the bonds are called coupons. These coupon returns are calculated as a percentage of the face value of the security. The term “nominal yield” may also describe the coupon.

Interest Amount

The amount of interest paid varies depending on the coupon rate. The greater the coupon, the greater the risk the security carries. Several credit rating agencies, such as Standard & Poor’s, Moody’s, and Fitch, publish ratings for government bonds.

The ratings indicate how much the bond issuing authority can default on its obligations for repayment. These ratings range from AAA (the highest rating) and move on to other alphabets in the following order: “AAA,” followed by “AA” and “A,” and the next set of ratings is “BBB,” “BB,” and “B,” and so forth. Since AAA is highly rated for the quality of its returns, the risk increases as it moves along the alphabetical order.

Investors can hold on to the bonds till maturity. However, they can also trade them on the secondary market, similar to company shares. They produce income and thus are a good investment choice, especially since they are low-risk and backed by the government (it is low-risk because even governments can default on them). Another essential factor to consider while investing is rising inflation and interest rates, which work together to depreciate the value of fixed-income bonds.

Types

There are different types of Gilts, such as:

- Conventional gilts – Conventional gilt is a government liability that entails paying a fixed cash payment (coupon) to the holder every six months up until the maturity date. After which, the holder collects the final coupon payment and the principal return.

- Index-linked gilts – Index-linked gilts are bonds having borrowing rates and principal payments based on changes in the inflation rate. In index-linked gilts, the rates and payments depend on the inflation rates.

- Three-month lag index-linked gilts – The calculation of bond interest and principal payments use the inflation index from three months earlier.

- Eight-month lag index-linked gilts – These gilts use RPI figures applicable eight months before the dates. For a December dividend date, the RPI issue is for the previous April.

- Gilt strips – “Strips” stands for “Separate Trading of Registered Interest and Principal Securities. This comes with an option of stripping, separating the gilt into its cash flow, and trading them separately as zero-coupon gilts.

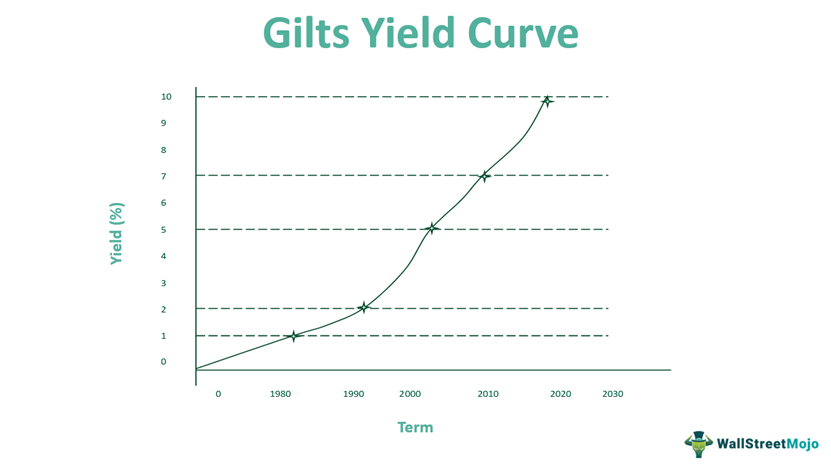

Gilts Yield Curve

Yield curves show the yield or return UK gilts have given over a specified time frame. One can gather this data for a particular period following the investor’s priority, and analyzing it can help them make investment decisions.

For example, suppose the yield on the gilts curve shows a decline, it is better to refrain from investments, and if the curve is showing an upward trend, it is likely to give similar results in the future.

For example, if a UK gilts bond gives returns of 1%, 2%, 5%, 7%, and 10% over five decades 1980,1990,2000,2010, and 2020, then it shows an upward trend, which means they give higher returns. We can plot this as follows:

Advantages & Disadvantages

Here are the main advantages and disadvantages of Gilts:

Advantages

- Security – The government issues them for financial purposes, and they must pay. Hence, they carry minimal default risk.

- Long maturity periods – The yield on gilts is regular, predictable income. Investors who want to invest for the long term can opt for it. Long-term investments give better results than short-term ones, and these bonds provide that option.

- Low risk – These are low-risk carriers since the government issues them, and they come with a guarantee in payment.

- Tax exemptions – Gilt sale profits are exempt from taxes, and people do not need to report them on tax returns.

Disadvantages

- Inflation – The real return on the security will decline due to inflation, and the possibility of rising interest rates will devalue the bond.

- Not Zero risk – They are low-risk carriers but not wholly devoid of risks. This is because there are governments that have defaulted on payments before.

Gilts vs bonds vs Gilts Funds

→ Explore all 63 Bonds articles

Gilts funds are debt funds, and their investments mainly focus on government securities. Therefore, they do not face the risk of nonpayment of interest or the invested principal. However, interest rate movements affect gilt funds as government borrowing usually happens over a long period.

Bonds are securities an issuer issues where they owe the holder an obligation of payment. Similarly, gilt bonds are securities or a type of bond issued by the UK government where the government is the issuer. Therefore, the issuer has to pay the holder later.

Frequently Asked Questions (FAQs)

What are UK gilts?

Gilt funds are fixed interest-bearing securities issued by the government. They are low-risk and secure and are referred to as “gold” or “gold-edged security.” Government securities in India are also known as gilts.

How do gilts work?

A invests $1000 in a gilt bond in the year 2020 with a maturity period of 10 years that pays 4% interest. After 2030, A will receive the investment amount, but the government will pay $40 (4% of $1,000) annually or in two installments if it’s 20.

Are gilts taxable?

Individual investors’ profits or losses on selling gilts (including on redemption) do not need taxes. Therefore, they do not need to report it as income or capital gains on their tax return.

Are gilts a good investment?

Investment decisions differ with individual long and short-term goals. Therefore, it varies from person to person. Gilts are best suited for people who invest for the long term and with a low-risk appetite. The returns may be moderate but guaranteed. On the other hand, high-interest short-term securities involve high risks.

Recommended Articles

This article has been a guide to Gilts and its meaning. Here, we explain how it works, its types, yield curve, advantages & disadvantages, and comparison with bonds. You may also find some useful articles here –