Part of our Types of Bonds guide

What Is A Secured Bond?

A secured bond is a type of bond in which the issuer of the bond provides a specific asset as collateral for the bond and offers a reduced rate of interest compared to unsecured bonds. In case of default, the secured bondholders need not worry as the issuer is obligated to transfer the title of the collateralized asset to the bondholder.

Thus, it is a debt instrument that is backed by assets which provides protection to the bondholder in case the issuer defaults. Mortgage-Backed Securities (MBS), Collateralized Debt Obligation (CDO) are some examples of secured bonds. They have a priority during payment as compared to unsecured bondholders. However, due to low risk profile, the interest rates offered is also very low.

How Does Secured Bond Work?

A secured bond is the one that is backed by some specific assets that provide protection to the bondholders in case the issuer defaults. The assets may be in the form of investory, plant and equipment, real estate, that are pledged to the bondholder to provide security.

In case the issuer is not able to make the payment due to bankruptcy or liquidation, these bondholders get a priority over other bonds regarding payment. They can claim the collaterals to recover the investments.

Various factors help in the valuation of these types of senior secured bond. The most important of them is the issuer’s credit rating and the value of the assets used as collateral. If the issuer has good creditworthiness and the collaterals have good value in the market, then the risk is very lower. However, low risk also means the secured bonds interest rate is very low as compared to secured bonds.

But it is important to understand that even though they are backed by security, they are not totally risk-free. If the value of the assets falls or if the credit rating of the issuer falls, the bondholders may face losses.

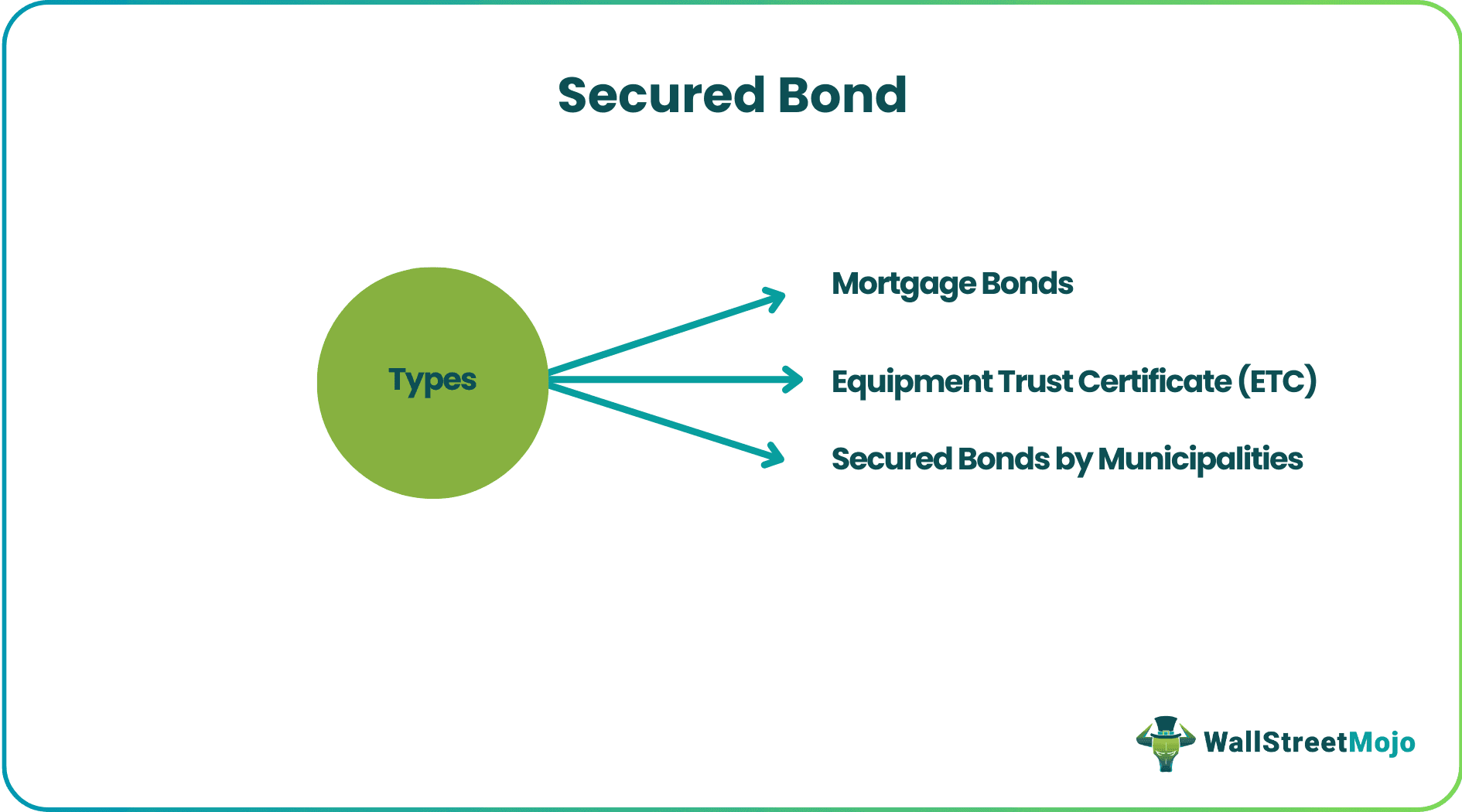

Types

#1 – Mortgage Bonds

Mortgage bonds are typically backed by real estate holdings or tangible property such as equipment. In case of default, the mortgage bondholders can sell off the underlying pledged property and get compensated for the invested amount—the ownership of the asset shifts to bondholders in case of default. As mortgage bonds are safer than corporate bonds (no collateral), they have a lower rate of return.

#2 – Equipment Trust Certificate (ETC)

ETC refers to debt instruments that allow the issuing company to take possession and use the asset while paying the bondholders over the period of time. The ownership of the asset is, without a doubt, belonging to the bondholders, but the company can use and generate income out of it. Investors supply capital by buying certificates; in turn, helping firms buy assets and lease it to them for operations if the borrower can meet lenders’ payment requirements, the ownership is transferred to the borrower. In case of default, the lenders get to choose what needs to be done with the assets.

Firms need not pay property tax on an asset as they have just leased the same from investors and thus increase their profitability from operations. These types of debentures are usually seen in the airline and shipping industry (also with railway cars).

#3 – Secured Bonds by Municipalities

Municipalities can raise funds from investors by issuing these types of senior secured bond for a specific project. The anticipated revenue from that particular project backs the bonds. Upon disclosing the project’s details and expected income, municipal bodies put forward the repayment strategy or plan to the investors. Investors can buy these types of bonds depending on their trust in the projects.

Examples

Let us try to understand the concept with the help of some examples.

Let us assume that there is a company named Agro Capital which needs to raise money for funding its agricultural projects. Therefore, the management decides that they will raise debt in the form of issuance of secured bonds worth $ 300 million. These bonds will be backed by assets in the form of agricultural loans of the company worth $350 million.

Thus, in this case, the agricultural loans act as collateral for the bonds. However, if the borrowers default in paying the loans used as security, the bondholders will suffer losses.

Advantages

Just as every financial concept and instrument has its own advantages and disadvantages, so does this concept. Let us try to understand the advantages first.

- The limited or negligible risk for the principal repayment: As a collateralized asset backs the bonds, the bondholder’s principle can be repaid in case of default by selling an asset.

- Firms can avail tax benefits during purchase and evade property tax on assets leased in case of ETC deals.

- An investor gets to show fully of partially secured bond as long term investments and gets tax shields significantly on their regular income.

- Coupon payments or interest payments will generate cash flow (yearly/quarterly/monthly) for the investor.

- Buying fully of partially secured bond backed by revenue streams will generate cash flow for investors upon the efficient execution of projects.

- Investors can pledge the bonds to raise money for banks or trade bonds in markets and benefit from trades.

- Firms can use secured bonds to raise extra capital in case if need be.

- Firms can lower the monthly repayment overheads by spreading them for a longer period of time.

- Convertible bonds give investors the right to convert to equity and reap profits out of it.

Disadvantages

The following are the disadvantages of the financial instrument.

- If the market interest rate raises than the secured bonds interest rate, the investor experiences losses as his coupon payment will be lesser than market payment (in case of fixed interest rate).

- When the interest rate rises in the market, the bond value goes down, and if the investor wants to liquidate the bond will get paid less than the market.

- If the market value of the collateralized asset depreciates, the principal amount repayment gets affected in case of default.

- In a rising economy, the bond rate will get affected unless the coupon rate is pegged to the market rate.

- In case of an economic recession, when the market value of an asset depletes, the investor’s principal is stuck or only less than the usual amount can be retrieved.

- The interest rate on fully secured bond is costly from a firm perspective in terms of a mortgage.

Secured Bond Vs Unsecured Bonds

Both the above two types of debt securities are used in the financial market. Let us try to identify the differences between them.

- The most important difference is that the former is backed by assets which provides security to the bondholders in case of default whereas the latter is without any backed asset.

- The risk involved in case of the former is very low as compared to the latter due to the collateral used in case of the former.

- Due to low risk, the interest rate of fully secured bond is lower as compared to the latter because the bondholders need less compensation because they are at a lower risk of loss.

- The former has a priority in case of payment during default by the issuer. The bondholders of secured bonds get their principal and interest due before any unsecured bond. They can claim the assets used as collateral to recover the loans.

However, it is always a good idea to do proper research and understand the creditworthiness of the issuer of bonds and make informed decisions about any investment opportunity.

Recommended Articles

This has been a guide to what is a secured bond and its definition. Here we discuss its types along with the examples, advantages, and disadvantages. You can learn more about investment banking from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.