Systemic Risk Meaning

Systemic risk is the financial risk that possibly threatens the entire business, enterprise, entity, or economy, leading to its abolition. It begins with affecting units at a smaller scale and continue transmitting the effects to larger entities, thereby hampering the financial mechanism of the economy as a whole.

It differs from a systematic risk, which is easy to assess beforehand, and the individuals and entities involved get an opportunity to prepare and work on the shortcomings. In short, while the former leads to the sudden collapse of the financial ecosystem, the latter symbolizes perpetual market risks.

Key Takeaways

- Systemic risk is a non-gaugeable risk that transmits from one institution or entity to another faster and severely impacts the financial mechanism, including the collapse of an economy.

- It differs from systematic or market risk that doesn’t come as a shock but emerges gradually, given an ongoing turmoil or issue.

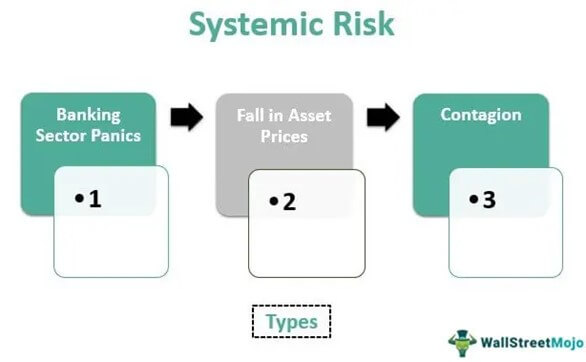

- Such risks are classified based on the reason that causes them. Hence, these are classified as banking system panics, falls in asset prices, and contagion.

- As it reduces the benefit of diversification in the market, it is also known as an undiversifiable risk.

Systemic Risk Explained

Systemic risk in finance indicates the possibility of one unhealthy institution affecting the other healthy units to such an extent that it causes a complete breakdown of the entire financial mechanism of the economy. Moreover, such risks quickly transmit from one entity to another, making it difficult to assess them beforehand.

Most risks observed affecting the market take time to spread and are easy to gauge. On the other hand, systemic risk comes to notice only when it has severely impacted some of the affiliated institutions in the series.

The Property Casualty Insurers Association of America classifies entities into two types to assess their chances of getting affected by these risks. One is too big to fail (TBTF), and the other is too connected or interconnected to fail (TCTF/TICTF). The risk measurement depends on the systemic risk analysis that lets analysts learn whether an institution falls under TBTF or TCTF/TICTF label.

If an institution falls under the TBTF label, it is most vulnerable to this risk. This is because such institutions are too big, and their failure would lead to severe consequences, including the collapse of the whole financial ecosystem. TBTF test indicates the size of an institution compared to the size of the local or global financial markets and helps authorities assess how vulnerable it is to systemic risk.

TCTF/TICTF test checks the chances of the total negative impact of an institution in case it fails to continue its operation. If the same is high, it leads to a more severe impact and vice-versa.

Causes

The cause of systemic risk identifies the type affecting the financial mechanism of an institution, industry, or economy. Here are the major types of such risks as defined by their causes:

The first on the list is the banking sector panic, which refers to the crisis in the banking sector due to depositors withdrawing more money than they need. It generally happens when they see other people removing reserves from the economy. Next is the decline in asset prices, like housing and stocks, which trigger systemic risk.

Contagion is yet another such risk that occurs when the collapse of one distressed financial institution leads to the destruction of other financial institutions. One such recorded event was the 2008 economic crisis.

Impact

The systemic risk reduces the benefits of diversification, affecting the insurance and investment market, given the role that risk diversification plays. Hence, this risk is also referred to as an undiversifiable risk.

Financial organizations are more vulnerable to such risks than other sectors or industries. The small occurrence can lead to the collapse of the entire economy or market collapse. If not prevented or regulated, such risks induce financial crisis and depression as they did in the 2007-2008 financial crisis.

Examples

Let us consider the following systemic risk examples to understand the concept better:

Example #1

The 2007- 2008 financial crisis started due to trouble in the subprime mortgage market in the U.S., led to the collapse of Lehman Brothers. The failure of such a big company led to the liquidity crunch, which adversely affected the entire credit and financial market and resulted in economic depression or crisis in the U.S.

The recession resulted in a global fall in trade and investment, a sovereign debts crisis, recession in other advanced economies, including Europe, and the Great Recession of 2007- 2008, which resolved later in 2009.

Example #2

Following the financial crisis of 2007-2008, the U.S. authorities introduced the Dodd-Frank Act of 2010 with a new set of guidelines to ensure no other similar event as the Great Recession occurs. This Dodd-Frank Wall Street Reform and Consumer Protection Act facilitated tight regulations to limit systemic risks to the maximum possible extent.

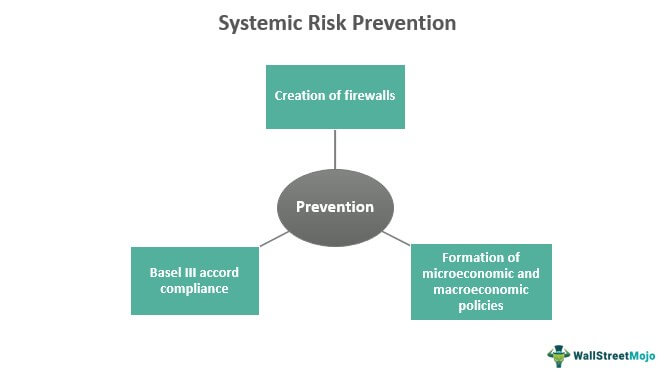

Prevention Regulations

The financial regulators prevent systemic risk worldwide after the 2007-2008 financial crisis. They began by creating firewalls and restrictions to reduce the economy’s vulnerability to such risks.

They formulated robust and strict microeconomic and macroeconomic policies for banks and other financial institutions. While the former includes regulations to protect the financial firms individually, the latter safeguards a nation’s financial system.

In addition, the Basel III accord came into being following the 2008 depression, which was introduced to mitigate the risk for the banking sector by asking them to maintain the required leverage ratio and capital reserve.

Systemic Risk vs Market Risk

Systemic risk differs from market risk, also known as systematic or undiversifiable risk.

The former is a non-gaugeable risk that transmits from one unhealthy institution to other healthy entities faster. This, thereby, affects the overall financial balance in the economy without giving it time to take care of the situation.

On the other hand, market risk is gaugeable and is influenced by multiple factors. Hence, businesses and authorities get time to take effective measures to deal with it.

Frequently Asked Questions (FAQs)

What is systemic risk in economics?

It is the probability or risk of an event that could trigger the downfall of an entire industry or economy. It happens when capital borrowers, like banks, big companies, and other financial institutions lose trust in providers like depositors, investors, capital markets, etc.

How to measure systemic risk?

The regular monitoring of the capital shortfall can help financial players to avoid such risks to some extent. However, as it is a risk that cannot be quantified, it appears as a shock, thereby creating severe turmoil in the industry or economy. Hence, analysts must be careful in measuring systemic risk and keeping a check on the small changes in the finances or capital building, especially of an entity too big to fail (TBTF) and too (inter)connected to fail (TCTF/TICTF).

How to mitigate systemic risk?

From creating firewalls and other security measures in the automated systems to following the guidelines set by higher authorities, businesses must be alert in implementing strategies and deploying technological measures to ensure avoiding such risks in the economy to the best possible extent.

Recommended Articles

This is a guide to Systemic Risk and its meaning. We explain its types, impact, prevention regulations, examples, and differences from market risk. You can learn more about finance from the following articles: –