Part of our Banking Products guide

What is Bank Deposit?

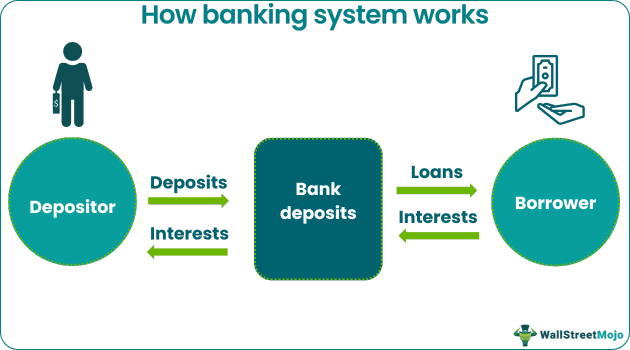

A bank deposit is the money someone places into a bank account. The depositor lets the bank safe keep their money for some time, in return for which the bank pays the depositor interest payments. The bank uses this money to invest or provide loans to its borrowers and, in return, receive interests payments from them.

- Bank Deposit accounts are bank accounts where money is deposited into a bank and held there.

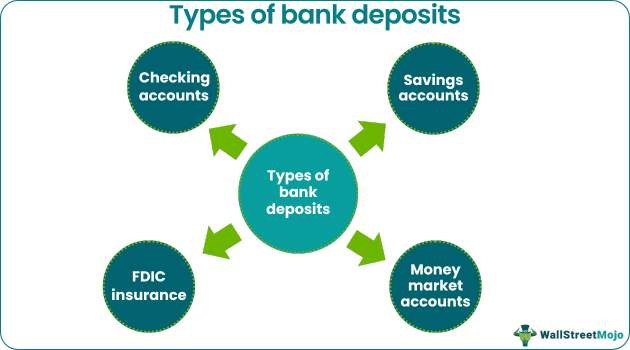

- The types of bank account deposits are checking accounts, FDIC insurance, money market accounts, and savings accounts

- Bank Deposit accounts are not investments and, as such, are a liability of the bank beholding them.

- Money market accounts can offer a higher interest rate than savings accounts.

Specific deposit accounts include checking, savings, and money market accounts. Depending on the terms and rules agreed to by the bank and its customer, bank deposits are available for withdrawal by the customer. They are also free to transfer the money to another person or use it to pay for their various requirements.

How Bank Deposits Work?

The deposit is an agreement of money the bank owes to the customer and acts as the bank’s liability to the depositor. Even though the depositor can enjoy access to the amount they see in their account, the bank now holds total responsibility for the asset.

When one deposits money in the bank, the bank takes the money and invests it elsewhere. Let’s say a person deposits $50. The bank would have spent it, but it is their responsibility that they must provide it if the person wants to withdraw it at any given time. Legally, the bank takes responsibility for the money and owns the legal rights while also keeping the balance available to the depositor.

Types of Bank Deposits

#1 – Checking Accounts

Checking accounts or current demand accounts, allows the depositor to withdraw their money whenever they want and “on-demand .” One can withdraw the cash from the checking account by card, withdrawal slip, check, or direct e-payment.

Banks purpose these accounts for day-to-day expenses. While there are fees associated with them, most are waived by meeting minimum requirements. Examples of such requirements are setting up a direct salary deposit linking to the checking account and at least withdrawing 1-2 times from the account each month.

Money is intended to move in and out of these accounts every month. Through checking accounts, banks can construct an accurate spender and income profile of their clients. They use this data to analyze wealth profiles and categorize customers into certain target levels. Advisors then direct their attention towards clients with higher supposed net worth for investment products and services.

#2 – Savings Accounts

Savings accounts are accounts where one deposits money to save it and not use it as often. Saving accounts are where one “parks” money for a longer period of time than a checking account.

In essence, nothing really separates a checking from a savings account except for the penalties. The money still belongs to the same bank, and one technically has the same privilege to the funds as per client agreements. The main functional difference is that there are withdrawal limits per month on a savings account for which the bank can demand fees if not adhered to.

Some savings accounts place these restrictions on their customers to not have the savings accounts operate like checking accounts. Banks offer an incentive to their customers to keep the money in the account in the form of an attractive interest rate.

Although typically very low (in most cases under 1% per year), an interest-bearing savings account allows the customer to save their money and accrue a certain level of interest per year. Banks have a vested interest in doing so as keeping a certain level of cash on hand is both a federal requirement and necessary for their own investments.

#3 – Money Market Accounts

Savings accounts that yield a higher interest rate than a traditional savings account are money market accounts. These accounts usually pay interest rates based on current interest rates in the money markets. For reference, these are also still lower than 1% but closer to 1% than a typical savings account. A typical APY, considered “high,” is around .35-.65%, meaning one will earn less than 1% interest on their entire deposit in a given year.

These accounts also have different requirements than a typical savings account. Money market accounts need higher minimum balances to maintain them. Usually, one must maintain minimums anywhere from $15,000 and upwards within the account to receive the yearly interest rate.

Money market accounts also have a debit card, check writing, and insurance privileges. In addition, insurance privileges, also called FDIC insurance, are present for all deposit accounts.

#4 – FDIC Insurance

FDIC insurance protects every deposit account a customer has for up to $250,000. This means that the bank has a liability to always guarantee at least $250,000 of the money available to the depositor under all conditions. Hence, before they can invest any excess, the bank has to have in cash up to that amount on reserve.

It is to safeguard against financial collapse and to secure the banking system. The Glass-Steagall Act legislation created this requirement after the stock market crash of 1929.

Should a person have less than this amount in each account, all their money is safe. Should they have, though, let’s say, $900,000 in an account and the bank liquidates, they lose $650,000.

To circumvent this, most people open several different accounts in the bank. For example, the customer with $950,000 would thus open four different accounts to safeguard all of their money.

Joint accounts, where two people are under the same account, can insure up to $500,000.

Things to Consider

Certain deposit accounts carry certain benefits besides the bank simply holding them. For example, money market accounts can generate much higher interest than typical savings accounts. That being said, it should not be considered an investment vehicle.

Money market accounts can offer a higher interest rate because they can invest in CDs (certificates of deposit) and other safe investments like government treasuries and commercial paper. Savings accounts on the other hand do not have permission for this.

Those who are usually best suited for money market accounts are looking to chip away at inflation and have large amounts of money to do so.

If one wants to have a larger return on their money, investing in variable interest rates is more appropriate. Banks also often lure high net worth clients with higher rates on MM accounts as they are considered” sticky” products that will likely have a client staying with them for a long period.

Frequently Ask Questions (FAQs)

Frequently Asked Questions

What are bank deposits?

<p>Bank deposits are money placed in a bank by a depositor for safekeeping. Even though the legal responsibility of the money now resides with the bank, the saver or depositor can withdraw or transfer the money to someone else as they please.</p>

Are bank deposits assets or liabilities?

<p>Bank deposits are a bank’s liability to the owner of the money. Therefore, even though the money is now the asset of the bank, it completely belongs to the owner, and they can do whatever they want to do with it within the boundaries of agreement.</p>

How do bank deposits work?

<p>A depositor puts their money in the bank for a specific period of time. People can open many different kinds of bank accounts with different features and benefits. The bank offers a specific interest on the deposit capital in return for this. Similarly, the borrowers can avail loans from the bank while they have to pay specific interest to the bank until the amount is repaid.</p>

Recommended Articles

This has been a guide to Bank deposits and their meaning. Here we discuss 4 types of bank deposits and how it works. You can learn more from the following articles –