Part of our Banking Products guide

Meaning of Standby Letter of Credit (SBLC)

Standby letter of credit is a credit facility provided by a bank whereby it fulfills a debtor’s payment obligations if he/she fails to make payments to a third party in a trade deal. The standby letter of credit is abbreviated as SLOC or SBLC.

A SLOC is usually found in trade deals between sellers and buyers. It is utilized if a buyer does not fulfil the payment terms of a contract and so, the SLOC issuing bank pays the seller on the buyer’s behalf.

- A standby letter of credit means a bank-issued document that protects a seller if a buyer doesn’t pay for goods or services.

- SLOCs are used in both domestic and international trade. Since they help carry out foreign trade smoothly, they are more frequent in international trade.

- SLOC is a credit facility as such the buyer who has issued a SLOC requires to pay the bank fees and interest over the due amount.

How Does the Standard Letter of Credit Work?

When a buyer enters into a contract with a seller, it is an important part of their deal that the buyer makes payment after receiving goods and services from the seller. Sometimes, the buyer can fail to make payments due to bankruptcy, political disturbances, shortage of cash flow, etc. A standby letter of credit comes as a rescue in such circumstances.

Buyers acquire a SLOC from a bank to ensure timely payments to the sellers if they default on the payment. In such a case, the SLOC issuing bank jumps in and makes the payment on behalf of the buyer to the seller who is referred to as the beneficiary in the SLOC jargon. Once the bank has made the payment to the seller, it requires the buyer to repay that amount as it is essentially a debt it owes to the bank. The rate of interest on such an owed amount varies from bank to bank. Besides, this facility requires buyers to pay specific fees.

Computation of the fee is usually done on 360 days basis from the date the SLOC becomes active, and till the date, it remains active. To understand the sample of a standby letter of credit, this Scotiabank SLOC can help. In this SLOC, the fee is set at 1.10% and the interest rate at 2% per annum.

SLOC is subjected to terms and conditions which are specified in a standby letter of credit agreement. The terms and conditions define specific requirements that the seller must fulfil to receive the bank’s payment. It also specifies all the documents which the seller needs to present to the bank to qualify for the payment.

For example, a SLOC agreement specifies that the payment will be made only if the goods are delivered by the 30th of September. If the goods are delivered on the 1st of October, there will be no payments. The payment is as such assured only on the fulfilment of the mentioned conditions of the agreement.

SLOC is used in international trade heavily as it simplifies foreign trade by offering features like payment in the currency of the seller’s nation.

A letter of credit differs from a standby letter of credit on this account.

Standard Letter of Credit vs Letter of Credit

- A letter of credit is issued by a bank guaranteeing the financial institution will ensure the buyer pays the seller on time. Commonly, the seller will receive the money after delivering the goods as a regular letter of credit does not have performance criteria clauses which are an essential part of a SLOC.

- Hence in a letter of credit vs standby letter of credit debate, a SLOC will not ensure payment when the delivery is made. The payment will happen only after the conditions of the agreement are met.

- Moreover, since it is a credit facility, banks issue SLOCs only after assuring the borrower’s creditworthiness. According to GBC International Bank, bid, advanced payment, and warranty SLOCs are also issued by financial institutions, depending on the buyer’s needs.

Standard Letter of Credit Example

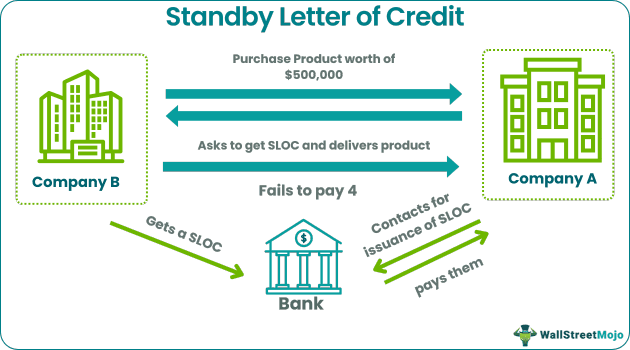

Here’s an example of how a SLOC may work:

Company A sells TVs, and company B wants to purchase $500,000 worth of their product. Since they’ve never done business before, Company A wants to protect themselves and asks the buyer to get a standby letter of credit. Company B goes to its bank and gets a SLOC.

Company A delivers the TVs to Company B and gives them 30 days to pay for the goods. Company B fails to pay for TVs within 30 days. After not receiving payment, Company A contacts the bank that issued the SLOC, informing them that they were never paid for their product. They submit the necessary documentation as per SLOC agreement, and the bank pays them what they’re owed.

For a seller, a SLOC offers exceptional protection and makes completing a business deal a no-brainer. Only catch here being, the seller must follow the agreement in the SLOC precisely. For example, if the $500,000 worth of TVs Company B bought were supposed to be 42” and black, and that was in agreement, but what they received were 36” and grey, that would be a failure to meet the specific terms.

In this case, the bank wouldn’t have to provide payment to Company A. SLOCs act as excellent protection for both buyers and sellers. They help ensure that buyers were delivered the specific goods they asked for and that sellers get paid.

There are many different types of SLOCs, based on their purpose. For example, a financial standby letter of credit protects the seller if the buyer forfeits on payment after delivering the goods or services. An advance-payment standby letter of credit will help recover an advance payment.

How To Obtain A Standby Letter of Credit?

- To get a SLOC, a buyer must apply at a commercial bank. Obtaining SLOC works like applying for a loan. The applicant will have to prove its creditworthiness and put up collateral in cases where the default risk is high.

- The amount of collateral will depend on the amount of money the SLOC is guaranteeing. Collateral is usually in the form of assets or cash.

- If approved, the buyer then submits all necessary details to the bank. These are usually the terms of sale, the specified amount to be paid in case of a default, the seller’s bank information, and the length of time the SLOC needs to be active.

- If there are special conditions the seller must meet to accept the goods or service, these must be explicitly explained in the SLOC agreement.

- Other essential information will go into the document, including dates, the amount the SLOC is guaranteeing, and both parties’ signatures.

- All parties must agree to these terms. Like we specified above, it is normal for a bank to charge their clients a certain fee annually for as long as the document is active. Standby letters of credit are irrevocable – they can only be changed if all parties agree.

Recommended Articles

This has been a guide to what is a standby letter of credit and its meaning. Here we discuss how it works and how to obtain a standby letter of credit along with examples and key takeaways. You may learn more about financing from the following articles –