Part of our Business Finance guide

In House Financing Meaning

In House Financing refers to the finances that sellers make available to purchasers directly without the involvement of any third party. As the businesses buy products in bulk, they might run short of funds. The sellers help these buyers with finances so that the dealing are done quickly without any delay due to external financing.

In house financing offers payment flexibility to buyers. In the process, the seller provides loans to customers to buy products from them so that the seller doesn’t need to wait till the purchaser’s loan gets processed and the buyer doesn’t need to pay the full amount at the same time as it can be divided into several months.

Key Takeaways

- When a business or seller finances its consumers through a single credit provider or works with a strong credit-providing facility, this is known as “in-house financing.”

- The strain is lessened for the buyer because there is no down payment required and the entire sum can be paid over a few months.

- The buyer and seller might agree to different payment schedules, interest rates, and down payments.

- Perils include some sellers, like used vehicle dealers, only offer used products for in-house financing.

How Does In House Financing Work?

In house financing is done when the company or seller has a strong credit-providing facility or deals with a single credit provider to finance their customers. It simplifies the work of both the seller and the customer.

When a seller offers the purchaser the option of credit on his own or through a single third-party financier to purchase the goods, it is called in-house financing. This helps the purchaser buy the product, as they can pay in monthly installments.

If a customer purchases a product and doesn’t have money to pay, the product cost is split monthly based on the plans they choose, and credit is provided for them. But, again, there won’t be many formalities or time to process these loans as they are provided with the seller’s own risk.

This is the process which helps customers get rid of the third-party financing needs, which involve longer wait time. Such financing alternatives are evident in automotive sector or any huge purchases in the retail industry.

Requirements

There are a few criteria that ones must meet to take up these in house funding services.

Let us have a look at the requirements below:

- If a customer has a low credit score or doesn’t have a good credit history, he may not be eligible to get a loan from a bank or other financing company. They can use this in-house financing facility.

- If a financing company takes time to process and the seller needs that product immediately, he can choose this option.

- With this, the seller can attract more customers as there won’t be many procedures, and they won’t take much time to process those loans.

- Purchaser doesn’t need to pay any down payment, and the entire amount can be divided over a few months, which makes their burden less.

- The buyer has an option to negotiate with the seller about payment terms, rate of interest, and down payment.

Examples

Let us consider the following instances to understand what is in house financing and how it works:

Example 1

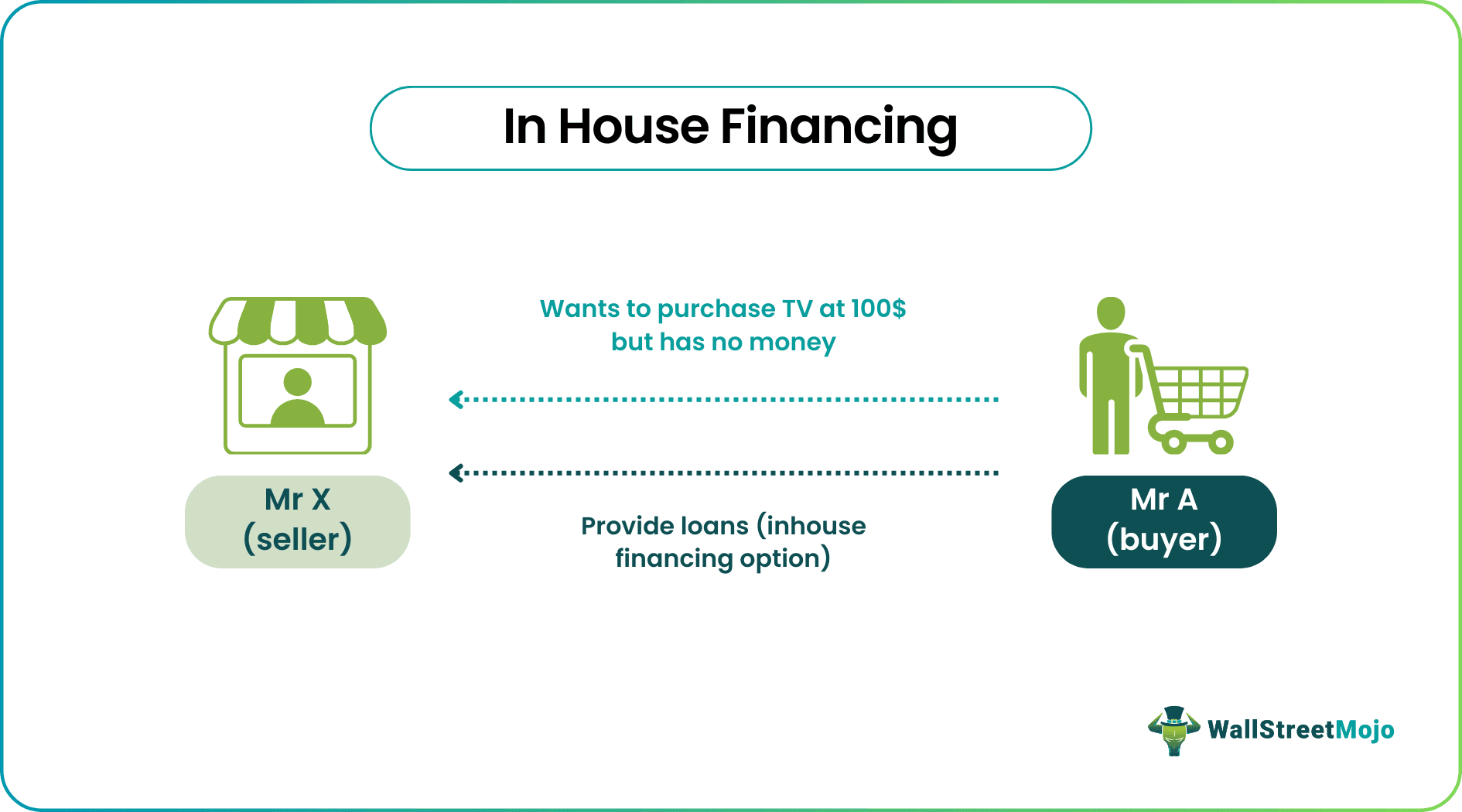

Let’s consider Mr. X has a branded electronics showroom and he is selling all items from TV, washing machines, .etc. A customer wants to purchase a TV that costs $100, has no money to make down payment or initial payment and he is not eligible to get loans from banks or other financing companies.

X here provides Mr. A with the in-house Financing option where Mr. A can pay the money for 12 months, with a 5% interest rate per month, and the procedure is very simple that he can take the loan within minutes.

In this example, the loan is provided by the seller at their discretion, and the payment terms, along with the interest rate, are negotiated directly with the seller; hence, it is known as in-house financing. It’s important to understand reverse mortgages when exploring alternative financing options like this.

Example 2

One of the most common sectors where such financing options are widely used is the automobile sector. However, a recent report covered a statement from AngloScottish Finance, which depicted how customers refrain from taking financial aid from the car dealers due to its expensive nature.

In addition, the report also stated that many dealers charge customers extra if they do not take up their financing services and opt for traditional ones, instead. The example above, therefore, shows how the availability of in house financing options affect the customers or make them to opt for this kind of financing under compulsion.

Advantages

In house financing is beneficial for both customers and retailers, who are also the lenders. This process helps the former get financed for the huge purchases they make without having to wait for the third-party to approve and lend the amount needed. In addition, the process also allows retailers to get the deal done quickly without wasting any more time.

Let us have a quick look at the in house financing benefits below:

- Facilitates customer with instant loans instead of the time-consuming process.

- It is helpful for people who can’t get loans from banks and other financial institutions as it is flexible with terms of issuing loans to customers.

- Whether you pay down payment or not it is not considered.

- The customer will be retained for the seller, and he will purchase again with them.

- Seller provides discounts to customers who opt for their in-house financing options that banks can’t offer.

- Once the loan is closed by the customer, it increases the customer’s credit score.

- Customers can negotiate with the seller for interest rate, down payment, discounts, etc.

Disadvantages

Though in-house financing has many advantages like less time-consuming, not much paperwork, and flexibility with payment terms, it also has disadvantages. A customer must efficiently choose the terms of payment and interest rate to benefit from such financing options. In short, besides the benefits that the process offers, there are a few restrictions or limitations too that the partes involved must know of.

Listed below are some of the demerits of using this financing option. Let us check them out in brief:

- The seller decides the interest rate, higher than the banks and other financial institutes.

- The customer may pay more as the price will be with a higher interest rate.

- The seller also must consider whether the customer pays his dues correctly, as the loan is given at his discretion..

- In some cases, the seller sells only used goods for in-house financings, like the used car dealership.

Frequently Asked Questions (FAQs)

Which is preferable, in-house financing or bank financing?

Housing loans and home loans are other names for bank funding. Compared to in-house financing and Pag-IBIG financing, interest rates for bank financing are typically a little cheaper.

Does internal financing run a credit check?

It doesn’t matter what’s on your credit reports because most in-house financiers don’t even do a credit check. Instead, these dealerships focus a lot on your income and down payment.

Is mortgage financing done in-house?

By definition, in-house financing is a sort of real estate financing in which a property developer permits a prospective homeowner to take out a loan to purchase a home.

Recommended Articles

This has been a guide to In House Financing & its meaning. We explain the concept along with its requirements, advantages, disadvantages & vs bank financing. You can learn more about financing from the following articles –