What Is A Thrift Bank?

A thrift bank, also known as a savings and loan association, is a form of financial institution that provides essential banking services. In addition, it offers a variety of savings options and mortgage loan services. Like commercial banks, these also qualify as depository institutions and may even provide a range of other products and services.

Earlier, thrift banks confine to offering time deposits and savings accounts. Still, with the change in customer behavior, preferences, needs, and expectations, these banks started offering various products and services from commercial banking firms and credit unions.

- A thrift bank, also known as a savings and loan association, is a financial institution that offers essential banking services, savings options, and mortgage loan services.

- Thrift banks qualify as depository institutions and may provide a range of other products and services, similar to commercial banks.

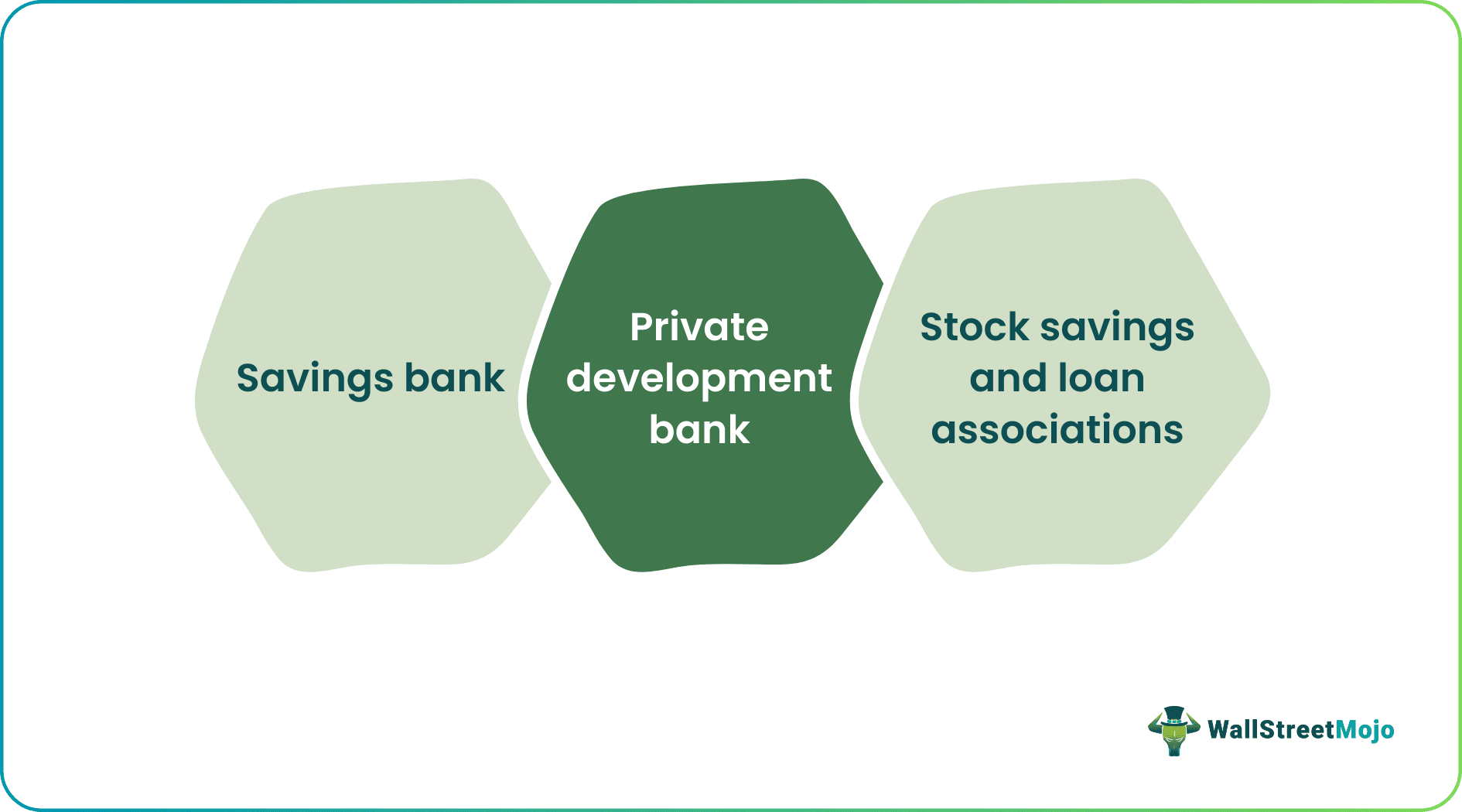

- Types of thrift banks include savings banks, private development banks, and stock savings and loan associations.

- Thrift banks prioritize serving the local community by offering competitive deposit returns and low-interest rates on mortgage loans.

Functions

- These banks are financial institutions that relieve the monopoly stress and offer their account holders facilities like savings accounts, mortgage loans, etc. The purpose is to accept deposits and provide mortgage loans to their customers.

- The interest on the savings deposited by the customers in the bank is high. In contrast, the customers’ curiosity about the mortgage loan is relatively lower than commercial banks and credit unions.

- They formed these thrift banks to offer their customers mortgage loan facilities, enabling them to make savings from time to time. It also focuses on relieving the mortgage and lending market from a monopoly of domestic or foreign banking institutions.

- These banks also offer mortgages at lower costs and savings accounts that pay a higher rate of interest in comparison to national and international banking institutions. These banks operate in the best interest of the local people. For this reason, they offer savings accounts and mortgage loans that could benefit the locals.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

The types are below provided and discussed: –

- Savings Bank- These banks generate funds from selling savings to customers and investing in mortgage loans.

- Private Development Bank- These banks are formed to support government policies.

- Stock Savings and Loan Associations- A locally or privately managed financial banking institution that takes long-term deposits to provide amortized home loans.

Examples of Thrift Bank

Various banks are operating as thrifts. A few of them are below: –

- Allied Savings Bank (Now PNB Savings Bank)

- City Savings Bank

- Business and Consumers Bank (A Development Bank)

- Citystate Savings Bank

- Bank One Savings and Trust Corporation

- Legazpi Savings Bank, Inc.

- Luzon Development Bank

- Dumaguete City Development Bank

- EIB Savings Bank, Inc.

- LBC Development Bank

- Lemery Savings and Loan Bank, Inc.

- Cordillera Savings Bank, Inc.

- Sampaguita Savings Bank, Inc.

- GSIS Family Bank

- Liberty Savings Bank Inc.

- BDO Elite Savings Bank, Inc.

- Inter-Asia Development Bank

- ISLA Bank, Inc.

- Life Savings Bank, Inc.

Thrift Bank vs. Commercial Bank

Thrift and commercial banks are different even though the former now offers similar services to commercial banking institutions and credit unions.

#1 – Commercial Banks

- Commercial banks are profit-oriented. They operate mainly to earn profits, and these banks don’t need to maintain asset class.

- The shareholders mostly own commercial banking institutions. As a result, these banks earn more profits to maximize the wealth of their shareholders successfully.

- The state and federal laws determine the powers of commercial banks.

- Commercial banks operate under the FRS (Federal Reserve System). Banking institutions procure deposit insurance from FDIC (Federal Deposit Insurance Corporation).

#2 – Thrift Bank

- Thrift banks are such types of banking institutions that differ from commercial banks in terms of goals and objectives and are similar only in the case of offering products and services.

- Thrift banks, unlike commercial banks, are not profit-oriented. The thrifts must be a member of the FHLBS (Federal Home Loan Bank System).

- It emphasizes more assets that are related to housing. Unlike commercial banks, these offer loans at a lower interest rate and higher savings return to their customers.

- These banks are not profit-oriented. Rather, these are local people-oriented. These banks function to assist the local people with savings and loan facilities and ensure that the monopoly of the national and foreign banking institutions does not impact the economy.

- They are owned mutually either by depositories or stockholders.

Conclusion

A thrift bank can also be called a savings and mortgage loan association. These are often termed savings banks that offer specialized services in the real estate sector. It offers savings accounts facilities and home mortgage loan facilities to local people. These are mutually owned as some of them are owned by the stockholders. In contrast, the others are held by their depositors.

These banks offer their customers a higher level of liquidity regarding mortgage loans and provide a higher yield for savings accounts. Thrifts initially offered facilities like time deposits and savings accounts. Still, with the expansion of banking services and the change in customers’ expectations and requirements, these banks also started offering similar products compared to commercial banks and credit unions.

Thrift banks function to benefit the local people. For this reason, it offers them high returns on their deposits and charges low interest on mortgage loans. These banks must not be confused with commercial banking institutions. The types are savings, private development, stock savings, and loan associations.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. What are the benefits associated with thrift banks?

Thrift banks offer several benefits to their customers. Firstly, they typically provide higher deposit returns and lower loan interest rates than larger commercial banks. Also, thrift banks often focus locally and prioritize personalized customer service. As a result, they are known for building strong customer relationships and understanding their unique financial needs.

2. What are the disadvantages of thrift banks?

While thrift banks have advantages, there are also some potential disadvantages. One drawback is that thrift banks generally have a limited branch network compared to larger banks. This can result in fewer physical locations and potentially less convenience for customers who prefer in-person banking. Additionally, thrift banks may offer a narrower range of financial products and services than larger institutions.

3. What are the risks associated with thrift banks?

Like any financial institution, thrift banks face certain risks. One significant risk is credit risk, which arises from the possibility of borrowers defaulting on loans. If borrowers cannot repay their loans, thrift banks may experience financial losses and decreased asset quality.

Recommended Articles

This article is a guide to Thrift Bank and its meaning. Here, we discuss functions, types, and thrift bank examples along with its difference from commercial banks. You can learn more about financing from the following articles: –