Part of our Cost Classifications guide

Semi-Fixed Cost Definition

A Semi-Fixed Cost refers to the cost that contains both variables and fixed elements of costs, i.eThe cost remains fixed up to some level of the activity or even if there is no activity but then increases with the increase in the level of activity.

Example

Suppose there was a toy manufacturing company. The factory of toy manufacturing was taken on rent for $ 20,000 per month. The total units produced in the factory in one month were 100,000 units. The production cost was $ 500,000. There was a supervisor, Mr. John, in the factory who charged $ 40,000 per month. But the company has also decided to give $ 1 per unit if the units produced under his supervision increase by 100,000. In April, the units produced were 110,000. In this case, we need to calculate the total semi-fixed cost in April.

Solution

In the above scenario, Rent paid is the fixed cost because rent is to be paid at every level of production in the company, and the same does not change with the change in the level of production in the company. The production cost of $ 500,000 is the variable cost as it changes with the change in the production level in the company.

But in this case, the salary of the supervisor, Mr. John, is semi-fixed cost as this salary is fixed up to the level of 100,000 units. But, still, beyond that, it increases with the units produced under his supervision.

Semi Fixed Cost = Fixed Salary Pay + Variable Cost Per Unit * (Units Produced – Normal Production)

- = ($ 40,000 + $ 1 (110,000-100,000))

- = ($ 40,000 + $ 10,000)

- = $ 50,000

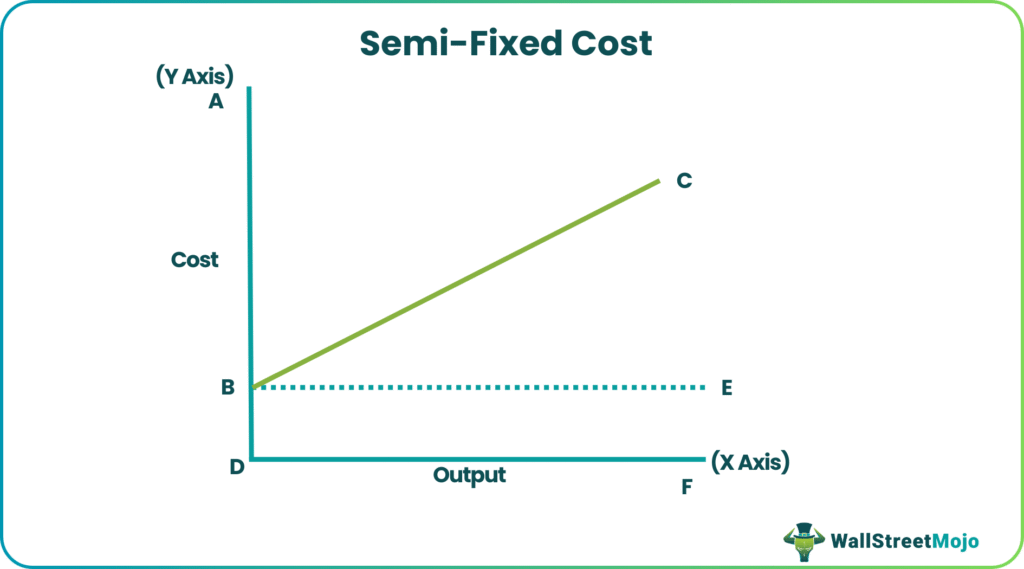

Semi Fixed Cost Graph

The X-axis shows the different activity levels in the above graph, i.e., different output levels, and the Y-axis shows the costs. Line BC shows the total cost incurred at different levels of output in the company. It is a semi-fixed cost. Here, there is some cost (as depicted by point BD), which has to be incurred even if there is no production, i.e., zero output. This cost is known as the fixed cost of the company. Fixed costs will remain the same at all output levels. Rest all of the cost changes with the change in the production level to be a variable cost.

Importance

Semi-fixed costs play an important role in the company’s decision-making process. This is so because when the company plans the level of output that it should produce during a particular period, then the semi-fixed cost is to be considered as these costs may limit the company’s profitability at the higher levels of production and erode the bottom line of the company.

Semi Fixed Cost vs. Semi Variable Cost

Both types of costs are the same as they are a mixture of variable and fixed components. For example, the company has taken a package from the telephone company that is up to 10,000 minutes or less. The telephone company will charge $500, but when the minute consumption increases from 10,000 minutes, the telephone company will charge $0.5 per additional minute of call. Therefore, the consumption of minutes should be taken care of not to increase the organization’s cost.

Advantages

The advantages are provided and discussed below-

- To have an appropriate costing system, it is important for the company to know its semi-fixed cost and bifurcate its different costs.

- This cost helps plan the level of output that the company should target during the period under consideration.

Disadvantages

The disadvantages are provided and discussed below-

- In practical scenarios, it often becomes difficult to know the exact amount of the semi-fixed cost in the company as its calculation is not as straightforward as it is provided in theory.

- If this cost is not calculated correctly, it will lead to an incorrect forecast of different important aspects of the company.

Conclusion

Semi-fixed cost includes both fixed and variable components as these are the costs that are fixed up to some level of production in the company. Still, it then increases with the increase in the level of production activity of the company. Therefore, the companies must consider these costs while considering the increase in the production level, i.e., they are to be considered while planning the company’s production output level for every period.

Recommended Articles

This has been a guide to Semi-Fixed Cost and its definition. Here we discuss its formula and its graph, examples, advantages, and disadvantages. You may learn more about financing from the following articles –