Part of our Accounting Concepts guide

Commercial Substance Definition

Commercial substance exists in those business transactions where the result of such transactions is expected to bring some change in the cash flows of the business in the future and is taken into account only when there is a notable change in the risk of cash inflow, the timing of cash inflow and amount paid due to such transactions.

Commercial transactions exist only in those transactions where the result of such a transaction is expected to bring changes in the cash flows in the future period. The cash flow changes are considered when the transaction brings any significant change in 3 factors: change in the risk of getting cash inflows, change in the timing of receiving cash, and change in the amount paid due to such transaction.

Commercial Substance Explained

Commercial substance is a financial and accounting concept that helps in understanding whether an event or a transaction has resulted in any substantial change in the financial position or cash flows of the business. In other words, the concept is used to determine whether the transaction is merely a simple accounting event that has not much significance to the business or it has made a considerable change to the financial position of the company.

It is important to understand this concept of commercial substance in accounting clearly because it provides crucial information about the financial health of the business, that is useful in taking decisions. Any acquisition made for the purpose of expansion and growth will generate revenue in future through increase in customer base. This transaction will add a lot of value to the business and lead to rise in cash inflow and change the overall business strategy in the positive direction.

Similarly, if the business goes for a sale and lease back arrangement for any of its property, it may continue to use the space without any significant change. Thus, the transaction does not result in any huge change in cash flow that can materially affect the company financial condition. Even entering into any financial derivative contract in between periods of financial reporting, just to shift profits, will not significantly affect the economic condition. Thus, there is no such commercial value to the event. Thus, the concept accounts for only those transactions that impact the business in a serious way.

How To Determine?

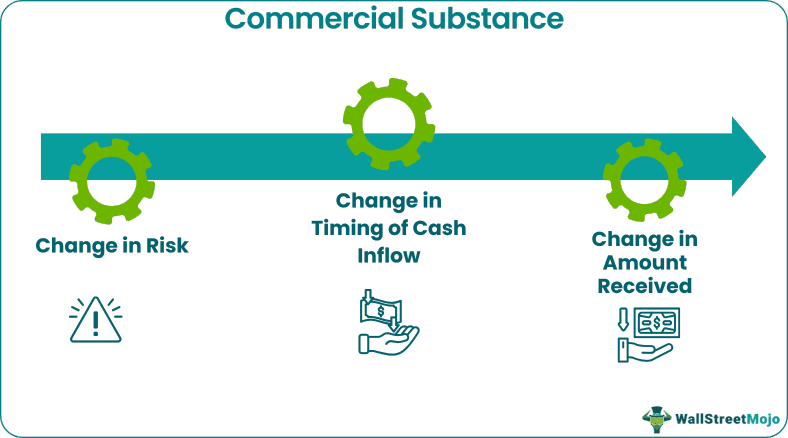

Commercial substance in accounting can be determined when there is a change in any of the following without tax effect:

#1 – Change in Risk

Let’s say a business entered a business transaction with other organizations where it gives motor cars as an asset, and in exchange, it acquires e-vehicles (asset). With the e-vehicles, the risk of accidents got reduced because before, lots of workers were using motor cars to deliver goods. The accident rate was 5%, but the vehicle accident rate was reduced to 2%. Hence there is a change in risk, so the asset is said to have commercial substance.

#2 – Change in Timing of Cash Inflow

In the same example, if ten motor cars are exchanged for 15 e-vehicles, and due to the exchange of e vehicles, the delivery can be faster, and revenue will increase. The differential amount of FMV of e-vehicles less FMV of motor cars will be settled after two years. So here, the inflow of cash increases due to an increase in revenue, and there is a change in the timing of cash outflow, i.e., the asset is said to have commercial substance.

#3 – Change in Amount Received

There is a change in the amount received in the above example of Motor vehicles and e-vehicles due to an increase in revenue.

As the exchange transaction satisfies all the conditions of commercial substance in a contract, this substance exists, and the asset is to be recognized at fair value.

#4 – Non – GAAP Transactions

Due to adherence to accounting transactions that should be followed while accounting any financial event of the business, it may be decided that the transaction does not have much commercial value. Therefore the companies should themselves decide, based on their own accounting rules, whether they should categorise the event any having much significance or not.

#5 – Tax Treatment

This concept also has an effect in the tax planning of the company. Sometimes a company may use some transactions as a means to reduce the tax burden on income earned, even though the transaction is not of much economic importance. In such cases, tax authorities should challenge such events to stop this practice so that there is not incidence of tax avoidance.

Therefore it is important to note that the main purpose of this idea is to ensure transparency, reliability and accuracy of financial statement and reporting. This leads to the fact that there should be a clear line of differentiation between the events that are of good value to the business and the ones that are not.

Example

Let us understand the concept of commercial substance in a contract with the help of a suitable example.

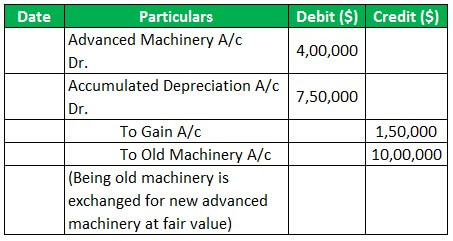

The company gives larger old machinery for smaller advanced machinery. The purchase cost of old machinery was $ 1,000,000, and the accumulated depreciation was $ 750,000. And the Fair Value of old machinery was $ 400,000 (which is deemed the value of smaller advanced machinery). Determine whether the commercial substance exists and, if yes, record the transaction?

Solution:

For a commercial substance to exist, there must be three points to be verified, i.e., whether there is a change in the value of cash flow, a change in timing of cash flow, or a change in risk due to transaction. If any of the above conditions are satisfied, then the transaction is said to have this substance.

In the above example the book value of asset is $ 250,000 ($ 1,000,000 – $ 750,000) and the fair value of asset exchanged is $ 400,000. As there is a change in the value, this substance exists in the transaction.

The above example clearly shows how to identify whether a transaction is with the scope of commercial substance by looking at the data given in the financial statements. It also explains how to record in in the books of accounts. This will help in differentiating between the financial transactions suitable for the concept.

Commercial Substance Of Contract

- A contract is said to have the commercial substance if, because of that contract there is a change in timing of cash flow, there is an increment in the cash flow, there is a change in the risk, or more benefits occur due to the contract.

- For example, A Ltd entered into a contract with ABX and Co., a major supplier of raw materials required by A Ltd. for the production of goods for supplying materials to A ltd. at a cost lower than the cost at which A Ltd. was buying from other suppliers. Because of it, the cost of production is decreased. As a result, the benefits will also be transferred to the customers by decreasing the selling price and increasing revenue. In this scenario, since there is a change in cash flow, it is said to have existed in the contract.

- It is necessary for company management, investors, creditors, analysts and other finance professionals to understand and exercise their knowledge and judgement to identify the proper and useful transaction as commercial substance exchange at the same time be within the accounting standard guidelines and adhere to them.

Commercial Vs Non-Commercial Substance

The two terms given above describe the events or business deals and arrangements that impact the financial position of the company or not. Let us try to identify the differences between them as given below.

- If monetary gains exist due to exchange transactions, the transaction is said to have a commercial substance. If there is no change in monetary gains, the transaction does not have a commercial substance. There must be a change in risk, value, or timing of cash flows for commercial substances.

- The commercial substance exchange transaction is essential for measuring the commercial substance. All monetary transactions are non-commercial substance transactions.

- If a commercial substance exists in the transaction, then the transaction is to be recorded at the asset’s fair value. If the commercial substance does not exist, then the transaction is recorded at the asset’s book value.

- As per the accounting standards, it is necessary that the transaction be recognized as having commercial value and changing the financial condition of the company in big way. If it is not so then it will fall under the category of non-commercial event,

- The former will also impact and change the risk profile of the business. If a lot of cash in flowing in or the event results in earning a huge amount of revenue for the company, this helps in increasing profits, give financial stability and the company is better equipped to handle financial shocks. But the latter is not capable of doing so.

- The former may result in increasing the efficiency, reducing cost and giving a boost to the production process. But the latter will not have a part in all these things.

- Due to their inherent features the former will compulsorily be recognised in the financial statement and reporting processs of the company whereas the later will very often not be recognised.

Thus, the assessment and identification is very important to differentiate between the two successfully leading to proper financial reporting.

Recommended Articles

This has been a guide to what is Commercial Substance. We explain it with example, its role in a contract, differences with non-commercial substance. You may learn more about financing from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.