Part of our Mergers & Acquisitions guide

What Is Accretion/Dilution Analysis?

Accretion/Dilution Analysis refers to the tool that determines how a merger and acquisition (M&A) would impact the earnings per share (EPS) of the buyer. The main goal of this analysis is to help the buyer and seller understand and explore the benefits of the proposed M&A deal.

The EPS accretion/dilution analysis is part of the merger and acquisition (M&A) strategies. It tries to understand the impact of a particular deal on the firm’s future EPS. However, the real-life application of the M&A accretion/dilution analysis is complex.

- Accretion/dilution analysis refers to an approach for determining the acquisition or merger’s effectiveness after the deal.

- It considers the earnings per share (EPS) of the acquirer as suitable for the short term. Thus, it helps in attracting investors on a global scale.

- Accretion refers to increased growth, whereas dilution refers to dissolved equity. This approach will define the benefit received by the acquirer.

- The steps involve the calculation of pro forma net income, pro outstanding shares (Acquirer shares plus new shares issued), and the calculation of pro forma EPS.

Accretion/Dilution Analysis Explained

Accretion/Dilution Analysis is an effective measure for studying the impact of a transaction deal like a merger or acquisition on the company’s earnings. In simpler terms, it considers how a transaction between two companies can affect their future EPS. Since the acquirer invests their capital to acquire another firm, the major influence or effect is visible in them. Therefore, the buyer mostly performs EPS accretion dilution analysis.

The word accretion refers to the addition or growth of earnings. At the same time, dilution refers to the reduction in the same. So, when two companies enter into a deal, there is an exchange of synergies between them. Both enjoy the benefits associated with it. But, if the deal does not bring enough benefits, it can cause losses. Therefore, the acquirer or buyer develops the M&A accretion dilution analysis model. It helps understand if a particular deal brings growth or loss to the company’s cash flows.

It is possible to find the pro forma effect using the simple accretion dilution analysis for private companies. The following are the equations for accretion/dilution analysis:

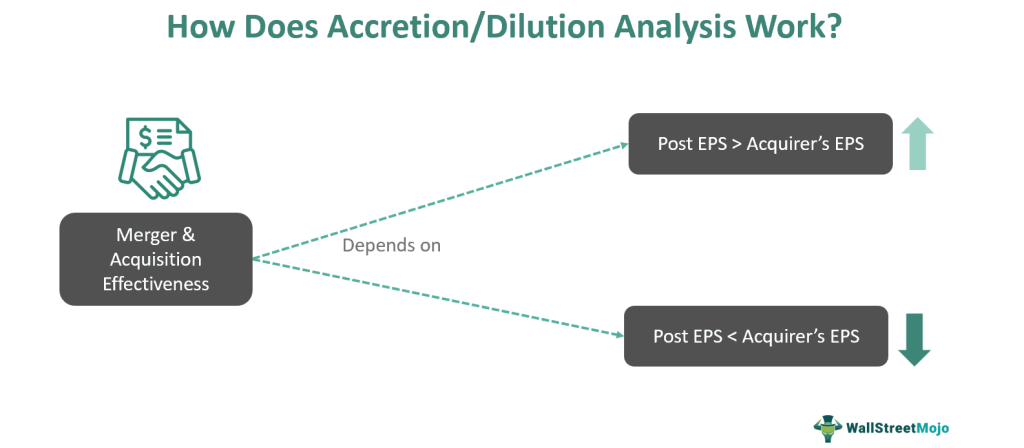

In cases of accretion, the EPS after M&A > the acquirer’s EPS.

Similarly, during dilution, the acquirer’s EPS > EPS after the deal. But, sometimes, there might be no effect on the buyer’s EPS.

The EPS serves as a perfect tool for understanding the effect of M&A. Since EPS is a short-term measure, investment bankers are less likely to consider it. Instead, they focus on the firm’s cash flows. However, investors need more time for detailed analysis. Therefore, they look for cash EPS to understand the effect of the merger. Yet, it is essential to note that accretion or dilution does not impact earnings in terms of long-term wealth creation.

Steps

Let us look at the steps on how to perform simple accretion dilution analysis for private companies:

Step #1 – Calculation of Pro Forma Income

One of the primary purposes of accretion/dilution analysis is the calculation of pro forma income. It includes the calculation of the following items in the order mentioned:

- Acquirer’s Net Income – It refers to the net income (after all deductions) earned by the acquirer in the standalone statements.

- Acquired Earnings – It includes the net income of the target company.

- Synergies – The combined value of both firms is known as synergy. However, the calculation depends on the percentage of revenue or earnings before interest, tax, depreciation, and amortization (EBITDA).

- Interest Expenses – Here, interest expenses are fees related to the M&A deal.

- Foregone Interest Income – It refers to the interest income that will no longer appear on the balance sheet. Instead, the target (acquired) firm will use it to pay the acquirer.

Step #2 – Determine the Outstanding Shares

After determining the pro forma income, check out the outstanding shares. It is essential as the purchase price might be paid in cash, stock, or both. The fully diluted outstanding shares can be taken if the entire amount gets settled in cash.

Here, the shares of the acquirer plus the new shares issued by the target company, if any, are considered. The resulting answer is that the pro forma shares are outstanding.

Step #3 – Calculate the EPS

The next step is to calculate the pro forma EPS. The formula for pro forma EPS is as follows:

Step #4 – Comparison Between Pro Forma EPS and Acquirer EPS

Lastly, the accretion/dilution analysis comes into the picture. Now, the analyst can find the post-deal effect by comparing the pro forma EPS with the acquirer’s EPS.

Examples

Let us look at the examples to comprehend the concept better:

Example #1

Suppose ABC Ltd and XYZ Ltd went into a merger in 2023. The former is the acquirer (buyer), and the latter is the acquired (seller). Following are the details for calculating the accretion dilution analysis:

Calculation of Accretion/Dilution Analysis of ABC Ltd.

| Particulars | Amounts ($) |

|---|---|

| Acquirer Net Income | $10,00,000 |

| Add: Target’s Net Income | $800,000 |

| Synergies After-Tax | $50,000 |

| Less: Interest Expense | (30,000) |

| Forgone Interest Income | (150,000) |

| Pro Forma Income … (1) | $16,70,000 |

| Acquirer Fully Diluted Outstanding shares | 100 shares |

| Add: New shares to be issued | 100 shares |

| Pro Forma Outstanding Shares … (2) | 200 shares |

| Pro Forma EPS (1/2) … (3) | $8.35 per share |

| Acquirer’s EPS … (4) | $7.25 per share |

| EPS (Accretion/Dilution) [=3/4 -1] | 0.15 or 15% |

Here, ABC Ltd is accretive because their earnings per share have been more than what they were before the deal.

Example #2

According to the news dated May 2023, the Indian fashion brand Aditya Birla faced a price downfall after the acquisition of TCNS Clothing. Wealth management firm Nuvama’s statement states that the latter’s potential should not depend on accretion/dilution analysis. Instead, the focus should remain on the fit and turnaround of TCNS Clothing. After two years of trailing peers, TCNS’s recovery and underperformance can be attributed to the brand’s fit and turnaround, which can generate value for shareholders.

Example #3

The merger of Halliburton and Baker Hughes in 2016 led foundation of an oil giant with a then-expected revenue of around $55 billion. The companies, given the predicted accretion of 8.4%, combined their product lines, global presence, and technology in the oil and natural gas industry to create a comprehensive suite of products and services for customers worldwide. This, in turn, reflected growth opportunities and high returns on capital.

Frequently Asked Questions (FAQs)

What are the key drivers for accretion dilution analysis?

Among the critical factors for accretion dilution analysis include purchase price, estimated synergies, purchase price decided between the parties, cost of capital mix, and others. Most of the deals have lower acquisition costs and cheaper forms of financing.

How does accretion dilution analysis affect M&A?

As accretion/dilution analysis is calculated for a short tenure, it helps the firms determine the deal’s future. For example, if an acquisition is not fruitful to the buyer for the three quarters, the firm might reframe the agreement. It provides a detailed overview of the top executives on M&A deals.

What are the limitations of accretion dilution analysis?

Some advantages of an acquisition, like altered market dynamics or unforeseen costs, were not fully considered in this analysis. Additionally, it depends on predictions about future performance, which might only sometimes be true.

Recommended Articles

This article has been a guide to what is Accretion/Dilution Analysis. Here, we explain the concept in detail along with its examples and steps to calculate it. You may also find some useful articles here –