Part of our Mergers & Acquisitions guide

Bootstrap Effect Explained

Bootstrap Effect or Bootstrap Earnings Effect refers to the short-term boost in the earnings of the acquirer company when it merges with the target company even though there is no economic benefit from such a combination.

As a result of the effect, the earnings per share increases because not the earning is a combined figure of both the entities, the acquirer and the target company. But the outstanding shares do not increase significantly because the acquiring company uses some of its shares to purchase the target company.

When there are no economically viable gains from a business combination, such a surge in share price does not sustain for a long time as investors recognize that the increase in the acquirer’s EPS is purely due to the bootstrap effect, and hence, adjust the acquirer’s P-E downwards in the long run.

However, there have been instances (e.g. 1990’s dotcom bubble) where many high P-E companies bootstrapped their earnings to exhibit continuous EPS growth by successively merging with low P-E companies. Hence, investors must be cautious as companies may use such strategies to create this P-E bubble and maintain it through a merger spree. But, in the end, fundamentals always triumph. So, value investors will continue to be the winners.

Bootstrap Effect Video Explanation

How To Identify?

That was a lot of theory. Let’s just not be overwhelmed by the textual definition and dive more to put this concept under the belt.

The following events identify the bootstrap effect:

- The shares of the acquirer trade at a higher P/E ratio than shares of the target.

- The acquirer’s EPS increases after the merger without any operational contribution.

So why did the earnings per share of the company A shoot up?

If company A acquires company B through stocks, fewer combined shares will be shares outstanding post-merger. Since earnings remain the same but there are fewer shares of stock, the earnings per share ratio increases favorably. However, investors may not understand the reason behind the increase in earnings per share. Instead of knowing the underlying reason behind the sudden surge, investors may believe the earnings per share increased because of the synergy created through the merger, increasing the value of the post-merger stock.

Companies may enjoy this temporary boost in stock price, but the bootstrap effect generally becomes apparent in some years. To sustain the earnings per share ratio at an artificially surged level, the company would have to continue to play the merge-and-expand strategy by aggressively acquiring companies at the same rate. Once a merger-and-expansion spree comes to a halt, the earnings per share will decrease, and the stock price will follow suit.

Example

Let us understand the concept with some bootstrap effect examples.

Example #1

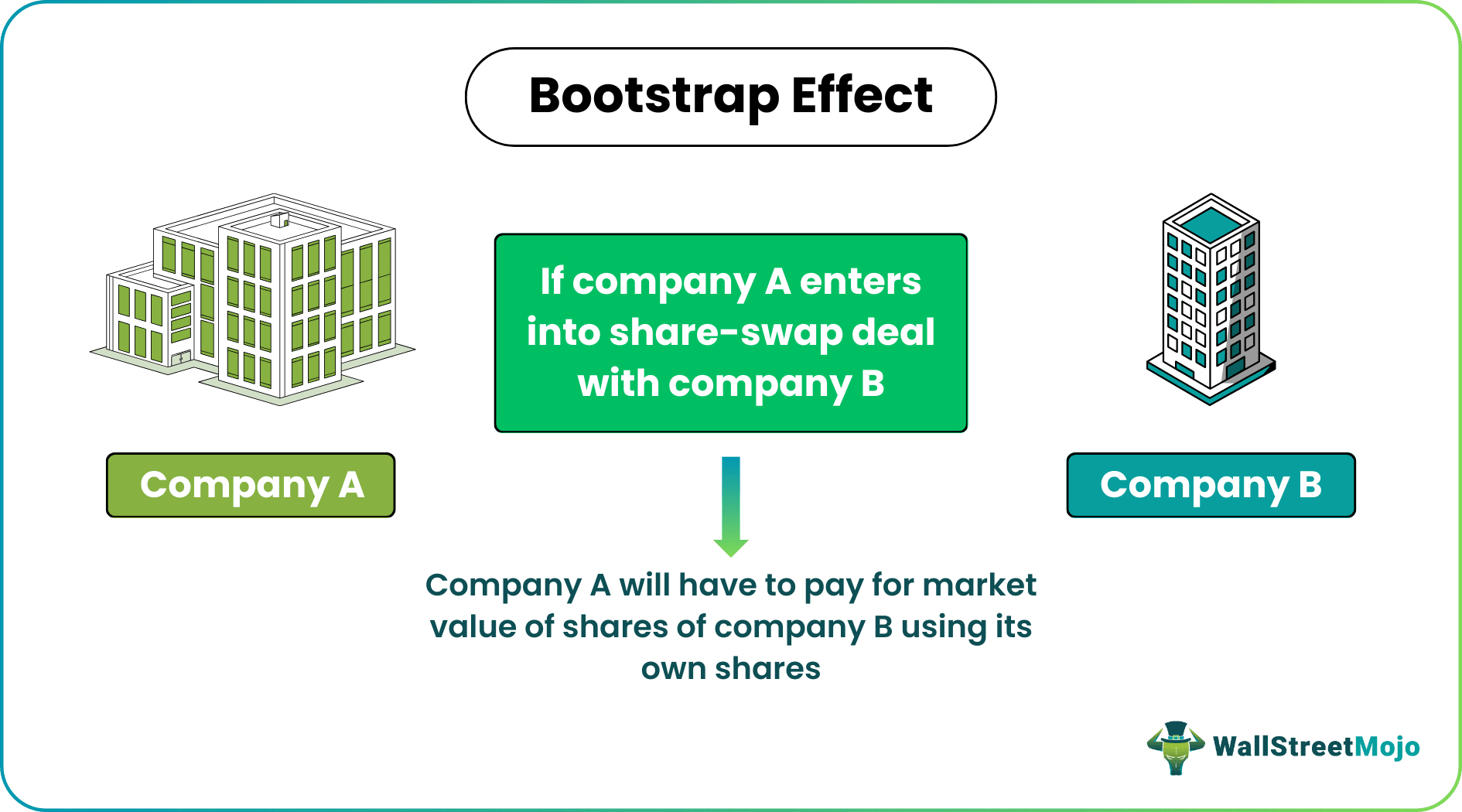

There are two companies: company A and company B. Company A is trading at a higher Price to Earnings than company B, which trades at a lower Price to Earnings ratio. Now, if company A enters into a share-swap deal with company B, company A will have to pay for the market value of the shares of company B using its shares. Given the above situation, the earnings per share of company A post-merger will shoot up. Remember, after the merger, there is no company B.

Example #2

Let’s take an example to understand it further:

| Particulars | Acquirer | Target |

|---|---|---|

| Share Price | $100.00 | $30.00 |

| Earnings Per Share (EPS) | $6.00 | $2.50 |

| Price to Earnings (P/E) | 16.7 | 12 |

| Shares Outstanding | 100,000.00 | 100,000.00 |

| Profit After Tax | $600,000.00 | $250,000.00 |

| Market Value of Equity | $10,000,000.00 | $3,000,000.00 |

- Acquirer needs to pay: $3,000,000.0

- Acquirer’s share price: $100

- Number of shares acquirer needs to issue: $3,000,000.0 / $100 = 30,000 shares

- So, as a result of the merger, there will be a total of 130,000 shares (including 100,000 old shares and 30,000 new shares).

- The post-merger earnings of the merged entity will be $850,000 (including $600,000 of the acquirer and $250,000 of target).

- Hence, the post-merger earnings per share will be 6.5 as per the following calculation:

- Post-merger EPS = $850,000 / 130,000 = 6.5

It can be seen that the post-merger earnings per share of the acquirer are greater than the acquirer’s earning per share before the merger, which is mainly due to the effect of reduction in the total number of shares of the post-merger entity, which is 130,000 (instead of 200,000) and increase in acquirer’s post-merger earnings due to addition of the earnings of the target.

This short-run increase in earnings per share is due to the sheer play of mathematics and not because of any economic growth merger.

Example #3

Let’s take some more bootstrap effect examples.

| Particulars | Acquirer | Target |

|---|---|---|

| Share Price | $100.00 | $70.00 |

| Earnings Per Share (EPS) | $3.00 | $2.50 |

| Price to Earnings (P/E) | 33.3 | 28 |

| Shares Outstanding | 100,000.00 | 50,000.00 |

| Profit After Tax | $300,000.00 | $125,000.00 |

| Market Value of Equity | $10,000,000.00 | $3,500,000.00 |

As per the table is shown above, we will calculate the following:

- of shares to be issued by the acquirer

- Post-merger EPS

- Post-merger P/E

- Post-merger Price

No. of shares to be issued by the acquirer:

- = Market value of Equity of Target / Share Price of Acquirer

- = $3,500,000.0 / $100.0

- = 35,000.0 shares

Post-merger EPS:

- = Total earnings of the Acquirer post-merger / Total number of shares of Acquirer post-merger

- = ($300,000.0 + $125,000.0) / (100,000.0 + 35,000.0)

- = 3.1

Post-merger P/E:

Assuming the market is efficient and hence pre and the post-merger share price of Acquirer will remain the same.

- = Weighted average EPS of Acquirer + Weighted average EPS of Target

- = $300,000.0 / ($300,000.0 + $125,000.0)) x 33.3 + $125,000.0 / ($300,000.0 + $125,000.0)) x 28.0 = 31.8

Post-merger Share Price of Acquirer:

Assuming market is not efficient, hence the share price pre and post-merger will not be the same.

- = Acquirer’s pre-merger P-E ratio x Acquirer’s post-merger EPS = 33.3 x 3.1 = 105

which is higher than the acquirer’s pre-merger share price due to the bootstrap effect.

Benefits

The method provides a lot of benefits to the small businesses and start up companies. They are as follows:

- More Control – In the process the entrepreneurs depend on their own resource and creativity for expansion. So there is no external influence or control.

- Rise in stock prices – If the market is not able to identify the effect in the accounting process, then the stock prices may actually rise.

- Rise in P/E ratio- It is helpful for companies with consistently low P/E ratios to boost their earnings and raise their stock prices.

- Sustainable business – The business becomes more sustainable in the long run because the are more focused on revenue growth.

- Attract external investors – The bootstrap businesses usually attract external investors easily because of their capacity to be profitable on their own.

Thus, the bootstrap effect leads to a continuous growth if there is also a focus on flexibility and customer satisfaction.

Limitations

Even though the approach has various benefits, there are some limitations also.

- Slow growth – Since companies using the bootstrap effect rely on their own internal resources for funding expansion and growth, there is a possibility of limited growth and a hindrance towards being more competitive in the market.

- Lack of external funds – They miss the opportunity of getting more finance from external sources because investors are quick enough to assess that the business has a higher earning not due to actual growth but due to bootstrap effect of the acquisition.

- High risk – Such businesses has a higher risk of failure there is an artificial picture of higher P/E ratio even though there is no actual increase in profitability.

- Limited resources – The limitation of resources can be a setback towards maintaining a competitive advantage in the market.

Thus, since the method has both positive and negative effects, entities should be careful before deciding to use it in their business.

Recommended Articles

This has been a guide to what is Bootstrap Effect. We explain it with examples, how to identify it along with its benefits and limitations. You may learn more about M&A from the following articles –