What Is The Cost of Revenue?

Cost of Revenue is directly attributable to a company’s goods or services. It includes the manufacturing, production, and distribution cost of a product or service to its customers.

Cost of Revenue of a Product Company

The following are the types of cost included in the product-oriented company –

Key Takeaways

- Direct Material – Manufacturing a product requires various components. It may involve the costs of raw materials, consumables, and semi-finished components. The total costs of the materials utilized in production are included in the Direct Material Cost.

- Direct Labor – Every company has a workforce that is partly allocated towards production and other departments such as administration, finance, and legal. The wages paid to employees who are directly involved in the manufacturing process are included under Direct Labor Costs.

- Direct Expenses – Apart from labor and materials, there are other expenses incurred by a company that can be attributed solely to its production process. For example – any commission paid on purchasing raw materials or consumables. These costs are included under direct expenses.

- Distribution Costs – These are costs incurred in delivering the product to the customer. Examples of distribution costs are freight charges, goods handling charges, storage costs (where goods need to be stored while in transit), and any related insurance charges.

- Marketing Costs – Costs directly attributable to the products for a particular period shall be included in this component. Examples of marketing costs are agency fees and advertising.

- Other costs – Any other cost directly attributable to the production and distribution of a product to the customer.

Cost of Revenue of a Services Company

Unlike a manufacturing concern, a service-oriented company has no material-related expenditure. Its major cost is the labor force. The components of a service-oriented company are discussed below in detail –

- Direct labor – The main asset of a service-oriented company is its human resources. The salaries paid to the service personnel constitute a considerable cost for the company. The companies also spend substantial time recruiting the right people for the right posts to ensure that services are provided optimally.

- Direct expenses – Direct expenses for a service-oriented company include costs of pieces of equipment utilized in providing these services.

- Marketing costs – There is no significant difference in marketing costs incurred by service-oriented and product-oriented companies. Although the target audience may vary, the components remain the same: agency fees, advertising fees, etc.

- Other costs – Any additional cost directly attributable to the production and distribution of a product to the customer.

Revenue vs Income Explained in Video

What is not included?

- Indirect Expenses – Indirect expenses such as depreciation, bank charges, communication expenses, and rents of office premises;

- Research and Development Costs – Any costs incurred by a company on the research and development of its product are not included in the cost of revenue calculation. These costs are usually high and are more likely to be amortized over a while.

- Administrative Costs – These are salaries paid to the non-production departments such as admin, legal, and finance.

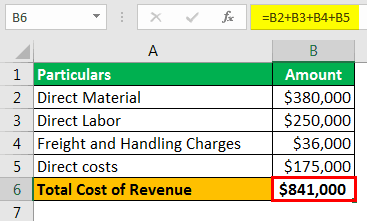

Example to Calculate Cost of Revenue

The revenue of the company for the year is $2 million, direct material costs are $380,000, labor costs $250,000, R&D costs $350,000, freight and other handling charges $36,000, admin costs $200,000, other direct costs $175,00, other indirect expenses $123,000.

The calculation for Cost of revenue –

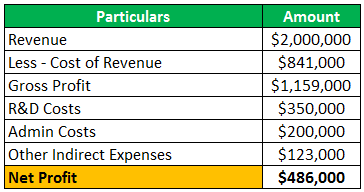

Calculation of net profit –

Cost of Revenue vs. Cost of Goods Sold (COGS)

Although both costs of revenue and COGS are used interchangeably, there are minute variances. The primary difference between them is that the cost of goods sold does not consider marketing and distribution costs. Manufacturers are more prone to use the cost of goods sold, whereas service providers are more prone to consider the cost of revenue. Cost of goods sold can be calculated by using the following formula –

Purposes of Calculating Cost of Revenue

- Ascertain direct costs – It includes all the direct costs associated with the product’s production and distribution.

- Calculation of gross profit – The gross profit calculation is simplified using the cost of revenue:

- Management decision making – Cost of revenue helps management decision making in a way that it separately identifies direct and indirect production costs. The company may optimize its operations by minimizing excess costs incurred.

Conclusion

The cost of revenue is a crucial component of a company’s income statement. Its components differ based on the nature of the company and the industry. Not only does it help in profit calculation but also in cost optimization.

Recommended Articles

This article has been a guide to the cost of revenue. Here we discuss types of cost of revenue in product and service-oriented companies along with examples & calculations. You can learn more about financing from the following articles –