Part of our Expense Recognition guide

What is the Bad Debt Expense Formula?

Bad Debt expense is an expense recorded in financial statements when amount receivable from debtors are not recoverable due to inability of debtors to meet their financial obligation and can be calculated using direct allowance/estimation method.

Explanation of Bad Debt Expense Formula

If an organization does its business by selling goods on credit, it always had a risk of non-recoverability of such amount. This non-recoverability is known as Bad debt, and recording such an expense is known as bad debt expense. Bad debt expenses equation can be recognized using two methods:

- Direct Method

- Allowance Method/Estimated Method

Direct Method

Under this method, the organization directly records bad debt expense. However, this method is not generally used by the organization since this method does not uphold the matching principle stated in the “generally accepted accounting principle.” Per this principle, expenses must be recognized in the same period in which they are booked.

Formula

Under the direct method, no formula is required since actual bad debts are recorded in books of accounts as an expense.

Allowance Method/ Estimation Method

Bed debts under this method recognize as a certain percentage of the sale made or outstanding debtors based on their aging and transfer such amount to a separate account known as Allowance for Doubtful debts. When an actual debtor becomes unrecoverable, such an account is debited, and the receivable account balance is reduced by crediting.

Bad debts under the allowance method can be calculated using two methods:

- Percentage of sale method

- Percentage of outstanding debtors

In the percentage of sale method, a certain percentage of the sale is recorded as bad debts expense during every accounting period based on past experience and future estimation.

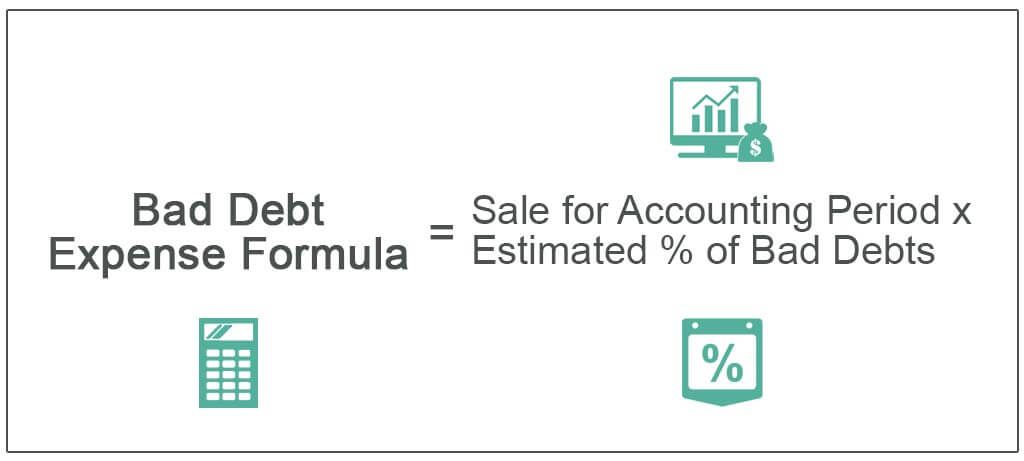

Formula #1

Bad Debt Expense Formula = Sale for Accounting Period * Estimated % of Bad Debts

In the percentage of the outstanding debtor, a certain percentage of debtors is recorded as bad debt expense based on their aging or simply based on how old debtors are. For example, the company will record 1% as bad debts from debtors, not older than 30 days, and 2.5% from debtors, not older than 60 days.

Formula #2

Bad Debt Expense = Outstanding Debtors based on aging * Estimated % of Bad Debts

These two methods are better illustrated with the help of the following examples.

Examples of Bad Debt Expense Formula (with Excel Template)

Let us consider a situation to understand the examples of bad debt expense equation using a direct method.

Example #1

Sale Expert Co. sold goods on credit to Mr. Smart, amounting to $ 1,200 on credit due in 7 days. After 5 days, the company got news of Mr. Smart’s insolvency as he cannot pay his outstanding bank debts. Mr. Smart has confirmed that he will be unable to pay to sell expert co as he does not have enough resources to pay bank debt or sell expert co debt. What accounting treatment should be done by the company to record an unrecoverable debtor?

Solution

The company is certain that the amount receivable from Mr. Smart is no longer collectible due to his insolvency; the company should record such non-recoverability as expense in its financial statement.

The following journal entry should be passed:

| Particulars | L.F No | Debit ($) | Credit ($) |

|---|---|---|---|

| Bad Debt Expense Dr. | 1200 | ||

| Account Receivable | 1200 |

(Being Bad Debt Expense Recognized)

Now we will understand the bad debts expense treatment using the allowance method/estimation method:

Example #2

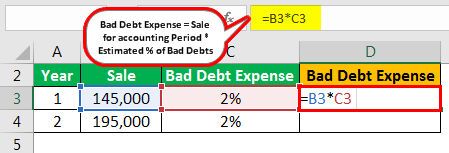

Future first Co. deals with FMCG products. Most of its sales happen on credit with an estimated recovery period of 15 days. The company recorded a sale of $ 145,000 during year 1. The company’s past trend shows that 2% of sales are not collectible.

Suppose in the next accounting period company recorded sales of $ 195,000. There is no change in its bad debt estimation. However, at the end of year 2, the company’s actual bad debt was $5000. Suggest the accounting treatment to be done if the company follows the allowance method of recording bad debt expenses.

Solution

First of all, we will calculate the bad debt expense to be recognized in year 1 & 2

Calculation of Bad Debt Expense

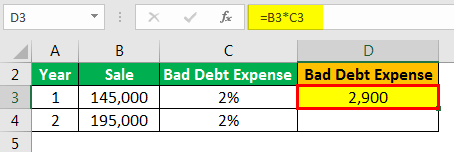

- =145000*2%

Bad Debt Expense will be –

- =2900

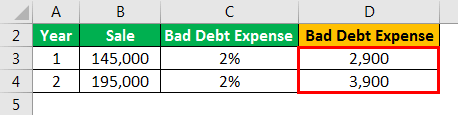

Bad Debt Expense for Year 1&2

- Bad Debt Expense for Year 1 = 2900

- Bad Debt Expense for Year 2 = 3900

Total will be –

- =2900+3900

- = $6,800

Accumulated balance in the allowance for doubtful debts at the end of year 2 follows –

| Sr No | Particulars | L.F No | Debit ($) | Credit ($) |

|---|---|---|---|---|

| 1 | Bad Debt Expense Dr. | 2900 | ||

| Allowance for Doubtful Debts | 2900 | |||

| (Being Bad Debt Expense Recognized) | ||||

| 2 | Bad Debt Expense Dr. | 3900 | ||

| Allowance for Doubtful Debts | 3900 | |||

| (Being Bad Debt Expense Recognized) |

Now actual bad debts are $5,000; the company will record the following journal entry –

| Sr No | Particulars | L.F No | Debit ($) | Credit ($) |

|---|---|---|---|---|

| 1 | Allowance for Doubtful Debts Dr. | 5000 | ||

| Account Receivable | 5000 |

(Being Account Receivable Balance Reduced)

Example #3

Taking the concept of bad debt expense further, let us illustrate a situation where bad debt is recognized based on the aging of debtors.

A local wholesale goods supplier supplies goods in wholesale to retailers. His past trend shows that from debtors not older than 30 days, 2% becomes bad. And from debtors older than 30 days, 3% becomes bad. This estimation remains the same for the current year as well. His debtors for the year is as follows:

- 0-30 days = $ 76,500

- More than 30 days = $ 82,500

The whole seller recommends the treatment to be done in books of accounts if he opts for the allowance method for recognizing bad debts.

Solution

First of all, we will calculate the number of bad debt expenses to be recognized:

Calculation of Bad Debt Expense

- =76500*2%

Bad Debt Expense will be –

- Bad Debt Expense = 1530

Bad Debt Expense for Year 1&2

- Bad Debt Expense for Year 1 = 1530

- Bad Debt Expense for Year 2 = 2475

Total will be –

- = 1530+2475

- Total bad debt expense to be booked = $4,005

Journal entry to be recorded in books of accounts:

| Sr No | Particulars | L.F No | Debit ($) | Credit ($) |

|---|---|---|---|---|

| 1 | Bad Debt Expense Dr | 4,005 | ||

| Allowance for Doubtful Debts | 4,005 |

(Being Bad Debt Expense Recognized)

Relevance and Use

Bad debt expense equation is an accounting procedure generally followed in preparing annual financial statements. Its relevance and use can be understood with the help of the following points:

- The bad debt expense equation helps obtain a true and fair view of financial statements as net profit and debtors are correctly estimated by identifying bad and doubtful debts.

- Bad debt expense recognized through the allowance method helps the organization keep some funds aside to meet future expenses.

- The allowance method is based on the matching principle in accounting, so it affirms that financial statements have been made using generally accepted accounting principles.

- Recovery of bad debts is recognized as income in books of accounts as earlier it was recognized as an expense.

Recommended Articles

This article has been a guide to Bad Debt Expense Formula. Here we discuss the formula for calculating bad debt expense along with practical examples and downloadable excel template. You can learn more from the following articles –

Recommended Articles

For more on Expense Recognition, explore these related articles from our Expense Recognition guide.