Part of our Expense Recognition guide

What is the Warranty Expense?

Warranty expenses refer to those repair or replacement expenses that are either expected to or already incurred by the company on the goods sold by the company in the past and are still under the warranty period as provided by the company to its customers.

This facility is offered to attract and maintain a customer base for various products, especially consumer durables (refrigerators, televisions, etc.). Warranty expense is an actual or expected cost that a business incurs to repair or replace the goods sold. The total amount associated is limited to the warranty period permitted by the business. Once this period has lapsed, businesses no longer incur a warranty liability.

These expenses are recognized in the same period as the sales for the products sold. It is based on the matching principle, whereby all expenses pertaining to a sale are recognized in the same reporting period as the revenue from the respective transactions.

Recording Warranty Expense

If a company provides a warranty on the product, they should repair or replace it if it’s defective. It creates a liability when the particular product is sold as the company has a liability, which starts when the product is sold.

It might not be ideal for a firm to record an expense that has not occurred, but similar to recording the Bad Debt Expenses, warranties also are required to be recorded on prior firm history and accordingly record the journal entry. Three essential aspects should be known while recording the warranty expense journal entry:

- The number of units of product sold during the time period we require to record?

- The percentage of products sold which are expected to be repaired or replaced? It is based on prior experience and shall be an estimate.

- The average cost of replacements or repair under warranty?

Example

Let us consider the below example for a better understanding

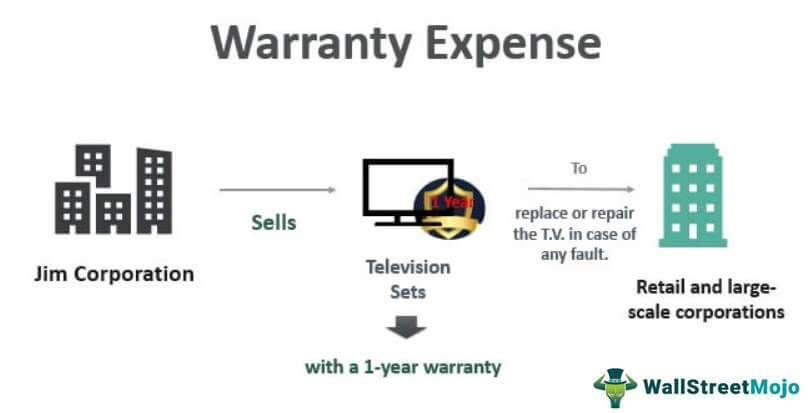

Jim Corporation is selling Television Sets across Retail and large-scale corporations. All the T.V. sets come with a 1-year warranty, whereby Jim Corporation shall replace or repair the T.V. in case of any fault.

The total sales for the year are $2,50,000. Based on records, it’s believed that 1% of the sales will encounter problems and require fixing or replacing.

During the next year, Jim Corporation had to serve several of their T.V. sets and end up costing the firm $7,500. This amount of repair did not record as another expense as it was already considered the previous year when the sale was recorded. Instead, the account of liability is further reduced by $7,500, and the inventory account is reduced accordingly.

One should also note that this liability treatment is essential for firms that have to repair or replace their products consistently. If the firm ever has a warranty claim, it does not require recording the liability. The costs can be recorded as and when they are incurred.

Warranty Expense Journal Entries

→ Explore all 30 Journal Entries articles

On every occasion, there is a Repair or replacement under the warranty facility, the impacted customer is required to file a claim, and the firm has to make a record of it. Depending on one case to another, the claim could either be:

- Accepted Completely

- Accepted partially

- Rejected

The warranty liability is also fulfilled if the firm is fulfilling the claim (entirely or partially). It means the company must decrease this liability amount by the cost of fulfilling the claim.

There are multiple ways through which a firm can fulfill a claim:

- Replacement of an item from the inventory – this would reduce the inventory.

- Secondly, the firm can repair the product using the part from inventory and external labor (cash/bank) or internal labor (wages payable). The repair or replacement should be recorded at cost and not the retail value of the item or parts.

Example 1

E.g. On August 1, Tinker Automobiles Ltd. received 15 mobile phones, which the consumers returned for the replacement under warranty. Every piece costs $25 to produce and ultimately sells at $40.

The firm is required to fulfill a warranty claim in which the company needs to debit the estimated warranty liability. This is because part of the warranty obligation is being fulfilled, and liability is decreasing. If we are removing them from the inventory, they should be removed at cost with the below warranty expense journal entries:

15 containers X $25 per container = $375 cost of inventory

Example #2

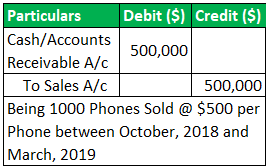

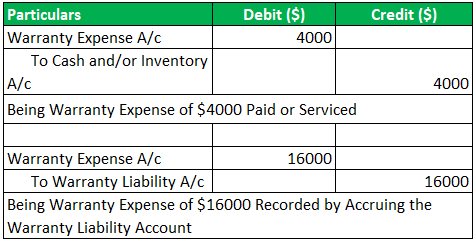

Apple Inc, a smartphone manufacturer, began producing a new phone in October 2018 and sold 1000 units @ $500 per piece in one financial year ending 31 March 2019. Every phone is under a warranty of not less than one year. Accountants estimated an average of 4% of warranty cost per piece, i.e., $20 per piece. As a result, parts replacement and services rendered in compliance with machinery warranties incur $4000 in warranty costs in the financial year 2018-19 and $16000 in the next FY 2019-20.

#1 – Sales Recognition of Phones by the Company

#2 – Recording of Warranty Expense for the FY 2018-19

Understand the company sold 1000 phones and an estimated warranty cost of $ 20 per phone. And in FY 2018-19, the year of sales, the company serviced $4000 against warranty obligation by cash payment and parts replacements. So we use worth $4000 of warranty expenses out of total estimation i.e.

- Total estimated Warranty cost = $ 20000/-

- Warranty exp incurred in FY 2018-19 = – $4000/-

- Remaining un-incurred expenses=$ 16000/-

Now what to do with this un-incurred expense of $16000? The company has to record this $16000 also for the FY 2018-19 itself based on accrual accounting. Accrue means recording expenses or losses now, which are going to recognize in the future.

So based on accrual methods, we incur a full $20000 as warranty expense. And in FY 2019-20 when actual recognition of $16000 happens

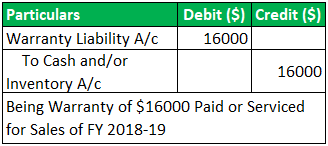

#3 – Recording of Warranty Liability for FY 2019-20

Interesting Point

The amount of warranty expense that occurred in FY 2019-20 is Nil or none. Because we have already expensed it in FY 2018-19.

Recommended Articles

This article has been a guide to the Warranty Expense. Here we discuss the definition, formula, and recording of warranty expense journal entries with practical examples. You may learn more about accounting from the following articles –