Part of our Monetary Policy guide

What is Liquidity Trap?

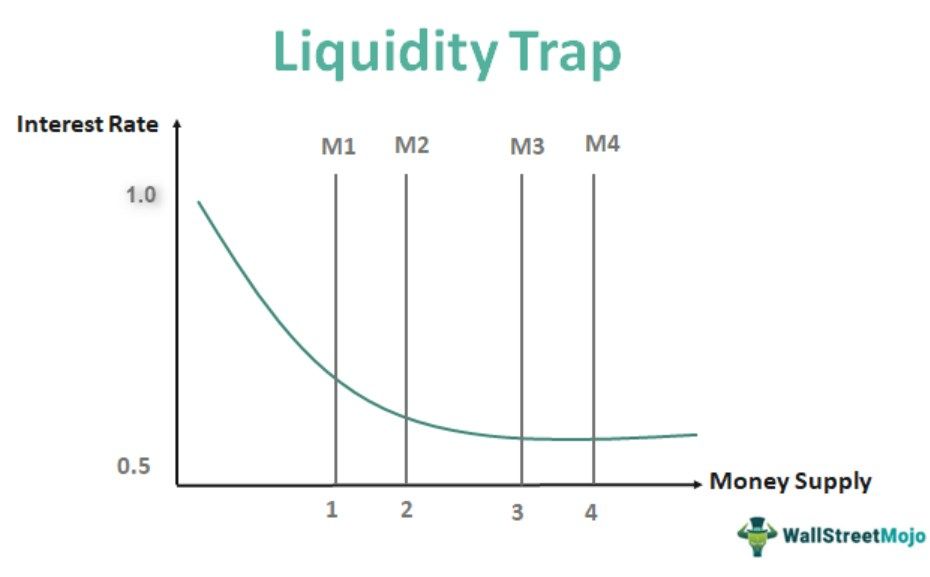

The liquidity trap is a scenario where the interest rates fall. Yet, the savings rate goes high, which tends to bring about ineffectiveness to the objective of expansionary monetary policy to increase the money supply. In this situation, people prefer holding cash rather than bearing a debt leading to virtual omission of liquidity from the market.

Since the central bank of the country injects more cash flow into the economy, it leads to inflation in the prices of goods. This occurs due to the fact that more amount of money is available for the same number of goods. Quantitative easing and greater cash flow is often acclaimed to be the most effective solution to liquidity trap economics.

- A liquidity trap is when interest rates fall, increasing household savings, which increases the money supply. Liquidity is mostly seen after a recessionary gap when the economy needs a boost and has been stagnant for a long time.

- A liquidity trap happens due to deflation, credit crunch, and decline in demand for banks; there is an increased affinity for savings, and investments go down.

- The United States faced a liquidity trap during the global recession in 2008-2010, when banks defaulted, and millions were left jobless.

Liquidity Trap Explained

A liquidity trap occurs when people curtail their spending habits and go on a saving mode or invest even when interest rates are low. As a result, the central bank fails to boost the national economy because of the lack of demand. If it is not controlled initially, it can lead to deflation. One key example of the liquidity trap is Japan’s national economy.The liquidity trap economics is generally seen after a recessionary period. People usually have a savings tendency during those times and prefer to hold cash rather than take debt.

It occurs even when there is a supply of money in the market, it fails to increase the amount of spending and investment.

There is a situation of very low-interest rates in the market. Even though policymakers want common people to hold illiquid assets by increasing the money supply, the scenario fails to attract consumers.

Examples

Let us understand the liquidity trap concept with the help of a couple of examples.

Example #1

Country X started experiencing extremely low cash flow for two consecutive quarters. Upon ordering an enquiry, the leaders of the country found that an ongoing war with a neighbouring country had elicited the sentiment of confusion and panic among its citizens.

As a result, the economy had slowed down to dangerous levels. Therefore, the government decided to set quantitative easing into action which would encourage spending among citizens.

Subsequently, they also injected more cash flow into the economy by printing more currency which revived the cash flow issues and got the economy towards normalcy again.

Example #2

A classic example of a liquidity trap can be the global recession the US faced during 2008-10. When the economy failed, central banks in the United States adapted to almost zero interest rates and short-term lending policies to enhance the liquidity in the market since people were holding their cash close to themselves, fearing the global depression.

Even though the monetary base was tripled during those times, even lending as such interest rates did not produce any significant results on the domestic price indices or the economy, thus creating a liquidity trap.

Video Explanation of Liquidity

Causes

Let us understand the causes of the liquidity trap concept through the discussion below.

#1 – Affinity toward Saving

Generally, people tend to hold cash close to them during the recessionary period. This habit increases the saving rate but decreases the spending rate. Being pessimistic about future conditions, they use this policy as a safety measure. Furthermore, banks are also reluctant to lend even after cutting the base rate to zero; the effect does not get translated to other lower commercial banks.

#2 – Deflation Expectation

If consumers expect a fall in prices, the real rate of interest can climb high even though the nominal rate is close to zero. The difficulty is creating a negative nominal interest rate i.e., a rare condition where banks would pay us to borrow to increase spending.

#3 – Credit Crunch

Banks become reluctant to lend during those phases even if consumers want to take advantage of the low-interest rate because they already suffer a huge loss in buying back defaulted debts and thus move into a stage of cleaning their balance sheet.

#4 – Decline in Demand of Bonds

During phases of a liquidity trap, interest rates go down to almost zero, hoping they will rise after a period. When the interest rate goes high again, the bond price falls. Thus, investors feel that it is preferable to hold cash than bonds..

#5 – Demand for Investment Goes Down

Firms do not find lower interest rates appealing because, during this phase, the firms don’t prefer to invest. After all, the demand stands very low.

Solutions

Even though implementing solutions and witnessing corresponding results can take a considerable long time, it is important to understand them to fully understand the liquidity trap economics.

- The interest rate offered by the central bank can play a key role. Increment in the interest rate of short-term borrowing stimulates people to invest instead of hoarding it. Higher long-term rates boost banks to lend since they will get a better return. This enhances the flow of money.

- The price declines to the lowest point that people are forced to shop more. It is applicable for both durable goods and assets like stocks. Investors start buying again because they can hold onto the investment long enough to overcome the phase.

- An increment in government spending can create confidence that the lender will support economic growth. It helps create jobs, eradicate unemployment, and hoarding of cash.

- Financial restructuring and innovative ideas can help set up a new market and overcome the existing trap.

- Global cooperation can be one of the solutions where two or more nations with excess and deficit of cash can come together and help with each other’s problems to reach a mutual balance.

Occurrences

Below are a few quick pointers that help us understand the liquidity trap concept in depth.

- The nominal rate close to zero gives rise to the liquidity trap.

- Recession or global depression is the prime reason for the liquidity trap.

- Monetary policy becomes ineffective.

- The unemployment rate rises with basic wages coming down.

Advantages

Despite the fact that it causes economic slow-down, there are a handful of advantages of liquidity trap economics. Let us understand them through the points below.

- It creates a market of cheap borrowing options, and thus this can be a phase to avail affordable loans for borrowing.

- It forces the policymakers to audit existing monetary policies and develop newer ideas to match the current scenario.

- It teaches the habit of saving among consumers.

Disadvantages

Let us understand the disadvantages of the liquidity trap concept through the explanation below.

- The liquidity trap generally occurs after a recession. This can further enhance the recession problem even further unintentionally rather than solving it.

- The phase is such that the central bank loses one of its prime powers to tweak the economy with the interest rate factor and stimulate growth.

- The risk of coming out of the liquidity trap is inflation, which comes next due to too much money available in the economy.

- It gives rise to unemployment as companies adapt to layoffs of costly resources and hire other resources at lower prices. It also declines to lower wages where people are further forced to compromise with goods and services.

- When interest rates go abnormally low, banks’ lack of deposit bases their income from loans is not encouraging. Thus, they become reluctant to give loans.

- Insurance companies are greatly affected because of low-interest rates. They rely on interest-based returns on the sum they receive from their customers as premiums to cover the liabilities, which further may lead to an increase in insurance premiums.

Frequently Asked Questions (FAQs)

How to avoid a liquidity trap?

Two ways exist once caught in a liquidity trap. The first approach is to employ a broad-based budgetary policy. Second, lower the floor of zero nominal interest rates once again.

Is Japan currently going through a liquidity trap?

Japan has been in deflation, stagnation, and low-interest rates for many years. Moreover, it has been mired in a liquidity trap for a while, and the current rise in political unpredictability is making matters worse.

What policy helps curb the liquidity trap?

Keynesian economists contend that an expansionary fiscal strategy is the most effective means of reducing the impacts of a liquidity trap.

Does liquidity mean cash?

The term “liquidity” describes how quickly and easily a security or asset can be turned into cash without depreciating. The most liquid asset is cash, while the least liquid asset is tangible goods.

Recommended Articles

This has been a guide to what is Liquidity Trap. Here we explain its causes, solutions, examples, and occurrences during the Liquidity Trap. We also discuss the advantages and disadvantages. You can learn more about finance from the following articles –

- Liquidation Preference

- What is Abnormal Return?

- Contractionary Monetary Policy

- Expansionary Policy Tools

Recommended Articles

Continue with these closely related articles from the same guide.