Difference Between NPV and IRR

The Net Present Value (NPV) method calculates the dollar value of future cash flows which the project will produce during the particular period of time by taking into account different factors whereas the internal rate of return (IRR) refers to the percentage rate of return which is expected to be created by the project.

Planning to make an investment decision? Confused about how to know its profitability? Well, there are two most important approaches which are used, and they are Net Present Value and Internal Rate of Return.

You can download the NPV vs IRR Excel Template from below –

Let assume that your organization has asked you to do an analysis – Whether the new project will be beneficial?

In this scenario, you would first analyze the project cost and try to evaluate its cash inflows and outflows (Free cash flows). Next, you will check in how many years the cost of the project would be recovered, and by what period of time that project will start providing the benefits. In order to measure the lucrativeness of the project or long term investment plans, there are capital budgeting tools used by many organizations and individuals to find out the profitability of the project.

The most common tools used are NPV & IRR. Both the tools are majorly used to evaluate the profits from the investments, and they both have their own pros and cons. But the primary question is – Which tool is better? There is a lot of debate you must have read, which states NPV is a better measurable tool well other states IRR. In this article, I will be guiding you through the difference between the two and also which tool has more relevance.

NPV vs IRR Infographics

NPV vs IRR Explained in Video

Advantages and Disadvantages of NPV

Net Present Value is the calculation of the present value of cash inflows minus the present value of cash outflows, where present value defines what will be the worth of the future sum of money as of today.

- If you are investing in certain investments or projects, if it produces positive NPV or NPV>0, then you can accept that project. This will show the additional value to your wealth.

- And in case of negative NPV or NPV<0, you should not accept the project.

Advantages

- Time Value of Money is given more importance i.e., the value of money today is more than the value of money received a year from now.

- Project profitability & risk factors are given high priority.

- It helps you to maximize your wealth as it will show are your returns greater than its cost of capital or not.

- It takes into consideration both before & after cash flow over the life span of a project.

Disadvantages

- It might not give you accurate decision when the two or more projects are of unequal life.

- It will not give clarity on how long a project or investment will generate positive NPV due to simple calculation.

- NPV method suggests to accept that investment plan which provides positive NPV, but it doesn’t provide an accurate answer at what period of time you will achieve positive NPV.

- Calculating the appropriate discount rate for cash flows is difficult.

Advantages and Disadvantages of IRR

You can use this approach as an alternative method for NPV. This method entirely depends on estimated cash flows as it is a discount rate that tries to make NPV of cash flows of a project equal to zero.

If you are using this method to make a decision between two projects, then accept the project if the IRR is greater than the required rate of return.

Advantages

- This approach is mostly used by financial managers as it is expressed in percentage form, so it is easy for them to compare to the required cost of capital.

- It will provide you excellent guidance on a project’s value and associated risk.

- IRR method gives you the advantage of knowing the actual returns of the money which you invested today.

Disadvantages

- IRR tells you to accept the project or investment plan where the IRR is greater than the + [Cost of Debt * % of Debt * (1-Tax Rate)]” url=”https://www.wallstreetmojo.com/weighted-average-cost-capital-wacc/”]weighted average cost of capital, but in case if the discount rate changes every year, than it is difficult to make such comparison.

- If there are two or more mutually exclusive projects (they are the projects where acceptance of one project rejects the other projects from concern) than in that case, IRR is not effective.

Example of NPV vs IRR

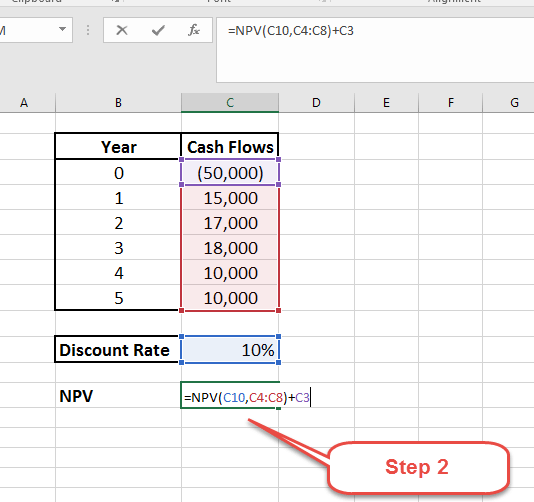

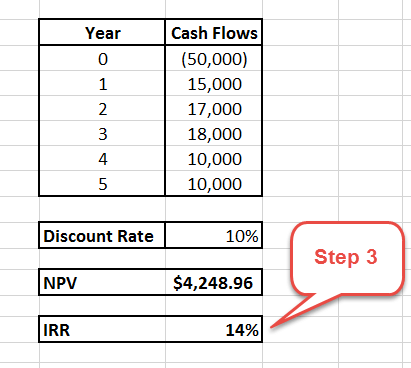

XYZ Company is planning to invest in a plant. It generates the following cash flows.

| Year | Cash Flow |

| 0 | (50,000.00) |

| 1 | 15,000 |

| 2 | 17,000 |

| 3 | 18,000 |

| 4 | 10,000 |

| 5 | 10,000 |

From the given information, calculate NPV & IRR & the discounting rate is 10%. And suggest whether XYZ Ltd. should invest in this plant or not.

#1 – NPV Formula Calculation

Where:

- CF = cash inflow

- r = discount rate

- t = time

- Cash outflow = total project cost

Step 1: Project the Cash Flows, Expected discount Rate and apply the NPV formula in Excel

Step 2: Add the Cash Outflow to the NPV Formula

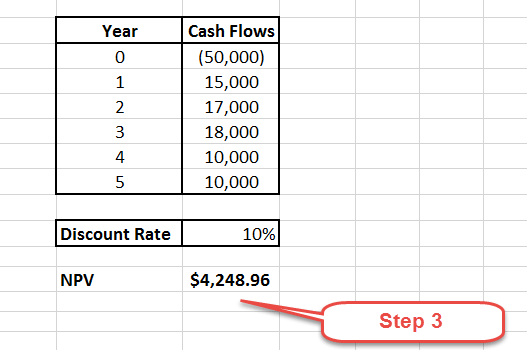

Step 3: Sum total to find the Net Present Value

#2 – IRR Formula Calculation

Where:

- CF = cash inflow

- t = time

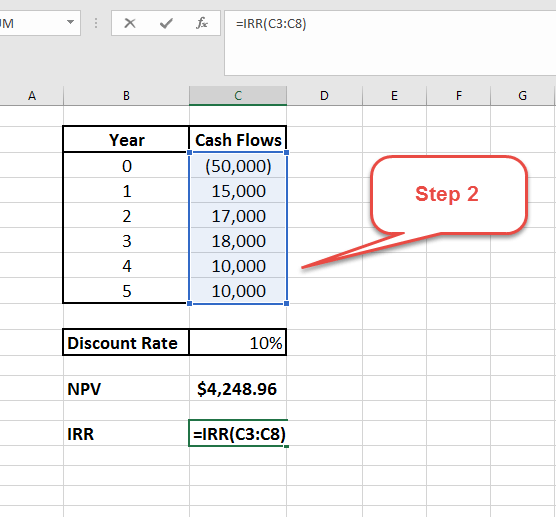

Step 1: Populate the Cash Flows

Step 2: Apply the IRR formula

Step 3: Compare the IRR with the Discount Rate

- From the above calculation, you can see that the NPV generated by the plant is positive and IRR is 14%, which is more than the required rate of return

- This implies when the discounting rate will be 14%, NPV will become zero.

- Hence, the XYZ company can invest in this plant.

Conclusion

As I can conclude that if you are evaluating two or more mutually exclusive projects, so better go for the NPV method instead of the IRR method. It is safe to depend on the NPV method for selecting the best investment plan due to its realistic assumptions & better measure of profitability. Even you can make use of the IRR method, it is a great complement to NPV and will provide you accurate analysis for investment decisions. Also, NPV finds its usage in DCF Valuations to find the present value of Free Cash Flows to the firm.

Recommended Articles

This has been a guide to NPV vs IRR. Here we discuss the difference between NPV and IRR using infographics along with its example advantages and disadvantages. You may also look at the following articles –