Part of our Accounting Concepts guide

What Is Cash Basis Accounting?

Cash Basis Accounting is an accounting method in which all the company’s revenues are recognized when there is actual receipt of the cash, and all the expenses are recognized when they are paid. Individuals and small companies generally follow the method.

This method is generally followed by individuals and small businesses with no inventory. It is a straightforward method and can be easily tracked. However, it only considers two types of transactions, i.e., cash inflows and cash outflows. In this method, a single-entry accounting system is followed since, for each transaction, a single transaction record entry is made. Since there is no tally between revenue and expenses in that particular accounting period, comparisons of previous periods are not possible.

Cash Basis Accounting Explained

The cash basis accounting method is a way of recording the accounting transactions for revenue and expenses, which are made in cash, i.e., either cash is received or any payment is made in cash. Therefore, it is ideal for small businesses. However, companies generally move away from cash basis accounting to an accrual method of accounting after they grow from the initial start-up stage.

Under this method, the accounts payable and receivable are not accounted for because actual cash does not change hands. Thus, revenue and expense is recognized when cash is paid or received irrespective of whether the goods and services have been provided or not. They are suitable for small businesses which do not have a large number of complex transactions to record. It can also be used by individuals who want to record their personal financial transaction for better money management.

It definitely has some disadvantages like it does not show the true financial condition of the business since it does not consider any transaction for which cash will be received in the future. It is also not suitable for inventory management.

Finally, whichever method of accounting a company follows (cash or accrual), it is supposed to follow that for both accounting and tax purposes.

Rules

The following are the principal features of cash basis accounting method–

- It follows a single-entry system (Also, have a look at double entry accounting system)

- Records only cash payments received and cash expenses paid. So, transactions will be recorded only cash will actually change hands.

- It is a simple process. And easy to follow and record. Therefore small businesses or any individual who have less number of transactions which are less complex, use it.

- It is not a good accounting tool. Rather it is just a method of keeping track of the daily purchases and sales made by the business.

- It lacks build in Error Checking Tool. It means there is no way of clarifying whether the transactions have been correctly recorded or not and or if any important details have been omitted.

- The cash basis accounting system mainly focuses only on Expenses and does not match Expenses and Revenues.

Example

Let us try to understand the cash basis accounting system with an example.

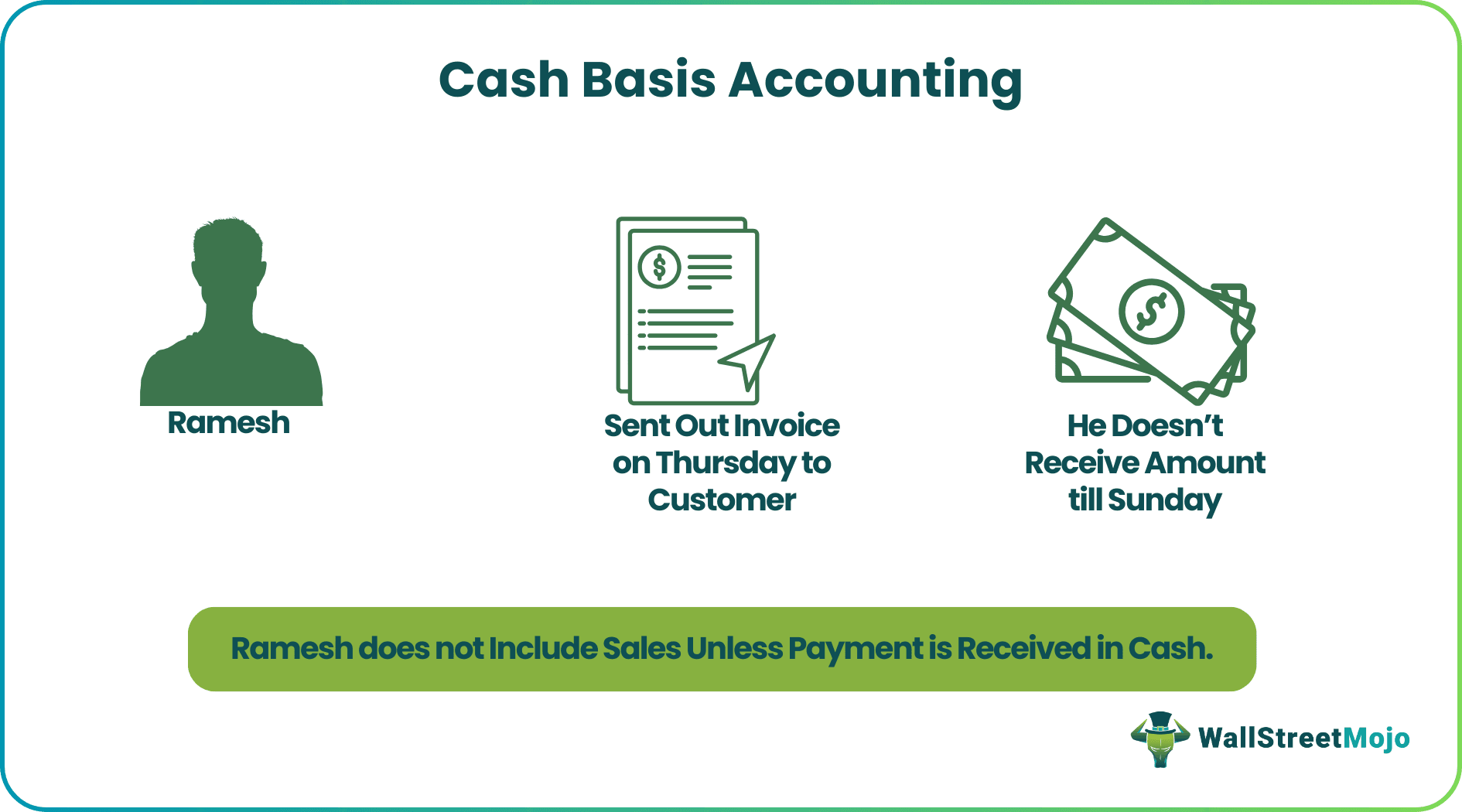

For example, Ramesh owns a small business for which he sent out an invoice on Thursday to the customer. But he doesn’t receive the billing amount till Sunday, so the income is recorded against Sunday’s date in the accounting books. So Ramesh does not include the sales done via credit card or credit account unless the payment is received in cash.

Form the above example, it can be clearly understood how to do cash basis accounting.

Cash Basis Accounting Video

Where Is It Used?

The next question is when to use cash basis accounting and for what kind of entities. It is used in the following cases as mentioned below:

- When a business uses a single-entry system;

- It is used when the business does not sell on its credit, i.e., whenever a customer purchases or a product is sold, payment must be immediately made by cash, check, bank transfer, or third party credit/debit card.

- The business has very few employees.

- When the business owns little (less expensive business supporting physical assets)or no inventory, i.e., the business does not have buildings, massive office furniture, extensive computer database systems, production machinery, etc.

- The company is a sole proprietorship business or privately held and has no bindings to publish income statements, balance sheets, or other financial statements.

The above points highlight when to use cash basis accounting.

Accounting In Small Business

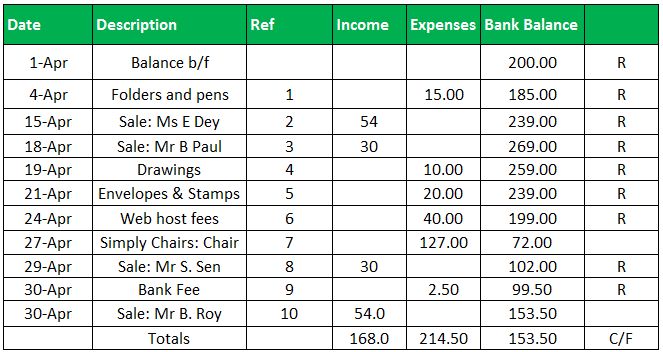

The below mentioned excel shows how to do cash basis accounting in case of a small business.

Journal Entries

→ Explore all 30 Journal Entries articles

Given below are some of the entries that is used while recording the financial cash inflow and outflow for the business using the cash basis. It is to be noted that there is no double entry involved in it where a debit and a credit is recorded in respective books of accounts, as followed in the accrual basis.

| Cash Book Balance | 153.50 |

| Add: Unpresented Check | 127.00 |

| Subtotal | 280.50 |

| Less: Deposit (not yet showing) | 54.00 |

| Bank Statement Balance | 226.50 |

Advantages

- Since it is a single-entry system and simple, it is easily understood by people with very less or no knowledge and background in finance and accounting.

- No trained bookkeeper or accountant is required to implement and maintain this system.

- It does not require complex accounting software. Hence a business can easily maintain a cash basis single-entry system in a notebook or simple spreadsheet.

- Since it tracks cash inflow and outflow, a firm knows how much actual cash it has at a given period.

- Businesses can accelerate payments to reduce their taxable profits, thereby deferring tax liability.

Disadvantages

- It gives us less accurate results since the timings of the cash flows do not provide the exact timing of the changes in the financial condition of a business.

- This type of accounting results can be manipulated by not cashing received checks or changing the payment timings for its liabilities.

- This method does not generate accurate financial statements; hence the lenders refuse to lend money to business having cash basis accounting.

- Auditors will not audit or accept financial statements done with this accounting.

- Since the results are often inaccurate, firms cannot publish management reports using such accounting.

- This method cannot give owners and managers important information for the evaluation of the firm’s financial position.

- Since it doesn’t have an error checking system inbuilt, the error goes unnoticeable until the firm receives a bank statement with an unexpected low account balance or an overdrawn account.

Cash Basis Accounting Vs Accrual Basis Accounting

Here we discuss the four differences between Cash vs. Accrual basis accounting

| Cash Basis Accounting | Accrual Basis Accounting |

|---|---|

| The simple system that keeps a record of business cash flow | Complicated method. |

| Apt for small business, sole proprietorship firm that mostly deals with transactions in cash. | Suitable for businesses that don’t get paid right at the moment. |

| Gives a clear picture of the amount of cash in hand and the bank account; | Gives a clear picture of the correct financial position of a business; |

| It doesn’t reflect the money that is owed to you or money you owe to others. | It records money owed to you and the money you owe to others. |

Recommended Articles

This has been a guide to what is Cash Basis Accounting. We explain its differences with accrual basis accounting, with example, advantages & journal entries. Here we also present the cash accounting method vs. accrual accounting. You may also have a look at the articles below on accounting –