Types of Credit Facilities | Short-Term and Long-Term

Table Of Contents

Types of Credit Facilities

There are majorly two types of credit facilities; short term and long term, where the former is used for working capital requirements of the organization, including paying off creditors and bills, while the latter is used to meet the capital expenditure requirements of the enterprise, generally financed through banks, private placements, and banks.

While raising equity (using IPO, FPO, or convertible securities) remains one method to raise funds for a company, business owners may prefer raising debt as it could help retain their control over the business. Of course, this decision is strongly dependent on the sufficiency of cash flows to service the interest and principal payments. A highly-levered company may burden the company's operations and the stock price. Consequently, the payment terms, the interest rates, the collateral, and the entire negotiation process of every loan remain the key to devising the capital strategy of a company.

In this article, we discuss the different types of credit facilities and their typical usage in the course of the business..

Table of contents

- Types of Credit Facilities

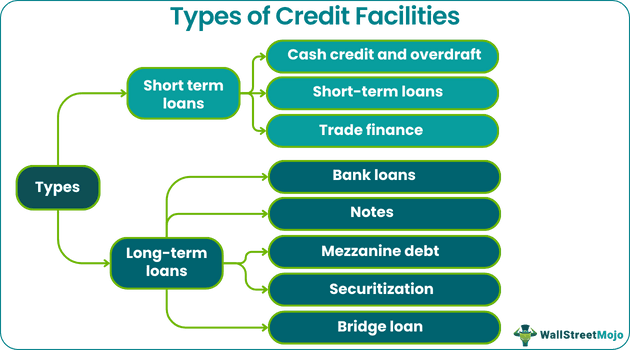

- Types of credit facilities are broadly categorized into short-term and long-term credit facilities.

- Short-term credit facilities are typically used for meeting working capital requirements, such as paying off creditors and bills. In contrast, long-term credit facilities are utilized for capital expenditure needs and are often funded through banks, private placements, and bonds.

- Short-term credit facilities include cash credit, overdraft, short-term loans, and trade finance, which address immediate working capital needs.

- Long-term credit facilities encompass bank loans, Mezzanine debt, notes, securitization, and bridge loans, which fund long-term capital expenditure and expansion plans.

Two Types of Credit Facilities

Broadly, there are two types of credit facilities:

1) Short term loans, mainly for working capital needs; and

2) Long-term loans, required for capital expenditure (consisting mainly of building manufacturing facilities, purchase of machinery and equipment, and expansion projects) or acquisition (which could be bolt-on, i.e., smaller in size or could be transformative, i.e., comparable size).

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Short-Term Credit Facilities

The short-term borrowings can be predominantly of the following types:

#1 - Cash credit and overdraft

In this type of credit facility, a company can withdraw funds more than it has in its deposits. The borrower would then be required to pay the interest rate, which applies only to the amount that has been overdrawn. The size and the interest rate charged on the overdraft facility are typically a function of the borrower's credit score (or rating).

#2 - Short-term loans

A corporation may also borrow short-term loans for its working capital needs, the tenor of which may be limited to up to a year. This type of credit facility may or may not be secured in nature, depending on the borrower's credit rating. A stronger borrower (typically of an investment grade category) might be able to borrow on an unsecured basis. On the other hand, a non-investment grade borrower may require providing collateral for the loans in the form of current assets such as the borrower's receivables and inventories (in storage or transit). Several large corporations also borrow revolving credit facilities, under which the company may borrow and repay funds on an ongoing basis within a specified amount and tenor. These may span for up to 5 years and involve a commitment fee and a slightly higher interest rate for the increased flexibility than traditional loans (which do not replenish after payments are made).

A borrowing base facility is a secured short-term loan facility provided mainly to commodities trading firms. Of course, the loan to value ratio, i.e., the ratio of the amount lent to the value of the underlying collateral, is always maintained at less than one, somewhere around 75-85%, to capture the risk of a possible decline in the value of the assets.

#3 - Trade finance

This type of credit facility is essential for an efficient cash conversion cycle of a company and can be of the following types:

- Credit from suppliers: A supplier is typically more comfortable providing credit to its customers, with whom it has strong relationships. Negotiating the payment terms with the supplier is extremely important to secure a profitable transaction. An example of the supplier payment term is "2% 10 Net 45", which signifies that the supplier's purchase price would be offered at a 2% discount if paid within ten days. Alternatively, the company would need to pay the specified purchase price but would have the flexibility to extend the payment by 35 more days.

- Letters of Credit: This is a more secure form of credit, in which a bank guarantees the payment from the company to the supplier. The issuing bank (i.e., the bank which issues the letter of credit to the supplier) performs its due diligence and usually asks for collateral from the company. A supplier would prefer this arrangement, as this helps address the credit risk issue concerning its customer, which could potentially be located in an unstable region.

- Export credit: This form of loan is provided to the exporters by government agencies to support export growth.

- Factoring: Factoring is an advanced form of borrowing. The company sells its accounts receivables to another party (called a factor) at a discount (to compensate for transferring the credit risk). This arrangement could help the company get the receivables removed from its balance sheet and fill its cash needs.

Long-Term Credit Facilities

Now, let’s look at how long-term credit facilities are typically structured. Banks, private placement, and capital markets can be borrowed from several sources and are in a payment default waterfall at varying levels.

#1 - Bank loans

The most common type of long-term credit facility is a term loan, defined by a specific amount, tenor (that may vary from 1-10 years), and a specified repayment schedule. These loans could be secured (usually for higher-risk borrowers) or unsecured (for investment-grade borrowers) and are generally at floating rates (i.e., a spread over LIBOR or EURIBOR). Before lending a long-term facility, a bank performs extensive due diligence to address the credit risk they are asked to assume given the long-term tenor. With heightened diligence, term loans have the lowest cost among other long-term debt. The due diligence may involve the inclusion of covenants such as the following:

- Maintenance of leverage ratios and coverage ratios, under which the bank may ask the corporation to maintain Debt/EBITDA at less than 0x and EBITDA/Interest at more than 6.0x, thereby indirectly restricting the corporation from taking on additional debt beyond a certain limit.

- Change of control provision means that a specified portion of the term loan must be repaid if the company gets acquired by another company.

- Negative pledge, which prevents borrowers from pledging all or a portion of its assets for securing additional bank loans (even for the second lien), or sale of assets without permission.

- Restricting mergers and acquisitions or certain capex

The term loan can be of two types – Term Loan A "TLA" and Term Loan B "TLB." The primary difference between the two is the amortization schedule – TLA is amortized evenly over 5-7 years, while TLB is amortized nominally in the initial years (5-8 years) and includes a large bullet payment in the last year. As you guessed correctly, TLB is slightly more expensive to the company due to increased tenor and credit risk (owing to late principal payment).

#2 - Notes

These credit facilities are raised from private placement or capital markets and are typically unsecured. To compensate for the enhanced credit risk that the lenders are willing to take, they are costlier for the company. Hence, they are considered by the corporation only when the banks are not comfortable with further lending. This type of debt is typically subordinated to bank loans and is larger in the tenor (8-10 years). The notes are usually refinanced when the borrower can raise debt at cheaper rates. However, this requires a prepayment penalty in the form of a "make whole" payment in addition to the principal payment to the lender. Some notes may come with a call option, which allows the borrower to prepay these notes within a specified time frame in situations where refinancing with cheaper debt is easier. The notes with call options are relatively cheaper for the lender, i.e., charged at higher interest rates than regular notes.

#3 - Mezzanine debt

Mezzanine financing debt is a mix between debt and equity and ranks last in the payment default waterfall. This debt is completely unsecured, senior only to the common shares and junior to the other debt in the capital structure. The enhanced risk requires a return rate of 18-25% and is provided only by private equity and hedge funds, which usually invest in riskier assets. The debt-like structure comes from its cash pay interest and a maturity ranging from 5-7 years, whereas the equity-like structure comes from the warrants and payment-in-kind (PIK) associated with it. PIK is a portion of interest, which instead of paying periodically to the lenders, is added to the principal amount and repaid only at maturity. The warrants may span between 1-5% of the total equity capital and provide the lenders the option to buy the company's stock at a predetermined low price if the lender views the company's growth trajectory positively. The mezzanine debt is typically used in a leveraged buyout situation. A private equity investor buys a company with as high debt as possible (compared to equity) to maximize its returns on equity.

#4 - Securitization

This type of credit facility is very similar to the factoring of earlier receivables. The only difference is the liquidity of assets and the institutions involved. In factoring, a financial institution may act as a "factor" and purchase the Company's trade receivables; however, there could be multiple parties (or investors) and longer-term receivables involved in securitization. Examples of securitized assets could be credit card receivables, mortgage receivables, and non-performing assets (NPA) of a financial company.

#5 - Bridge loan

Another type of credit facility is a bridge facility, which is usually utilized for M&A or working capital purposes. A bridge loan is typically short-term (for up to 6 months) and is borrowed for interim usage while the company awaits long-term financing. The bridge loan can be repaid using bank loans, notes, or even equity financing when the markets turn conducive to raising capital.

In conclusion, there needs to be a balance between the company’s debt structure, equity capital, business risk, and future growth prospects. Several credit facilities aim to tie these aspects together for a company to function well.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions

The types of export credit facilities typically include pre-shipment financing, post-shipment financing, and export credit insurance. Pre-shipment financing provides funding to exporters to cover production and shipment costs before goods are shipped. Post-shipment financing provides working capital to exporters after shipping goods, but payment from the buyer has not yet been received. Finally, export credit insurance protects exporters against the risk of buyer non-payment.

Loans are a form of credit facility that provide borrowers with a lump sum of money that must be repaid with interest over a specified period, usually in installments. On the other hand, credit facilities refer to a broader range of financial arrangements that provide borrowers with access to a predetermined amount of credit that can be used as needed within certain terms and conditions.

A credit facility is a general term encompassing various types of borrowing arrangements provided by financial institutions, including revolving credit lines, overdraft facilities, or term loans. On the other hand, a term facility specifically refers to a loan with a fixed term, usually with a specified repayment schedule. In addition, it may have a fixed or variable interest rate.

Recommended Articles

It has been a guide to Types of Credit Facility – Short-Term Credit Facility and Long-Term Credit Facility. Here we discuss its features and usages in various stages of the business. You may also have a look at the other recommended articles –

- Private Equity Firms in Germany

- Business Risk vs Financial Risk

- Salaries in Private Equity in Russia

- Options vs Warrant