Part of our Banking Products guide

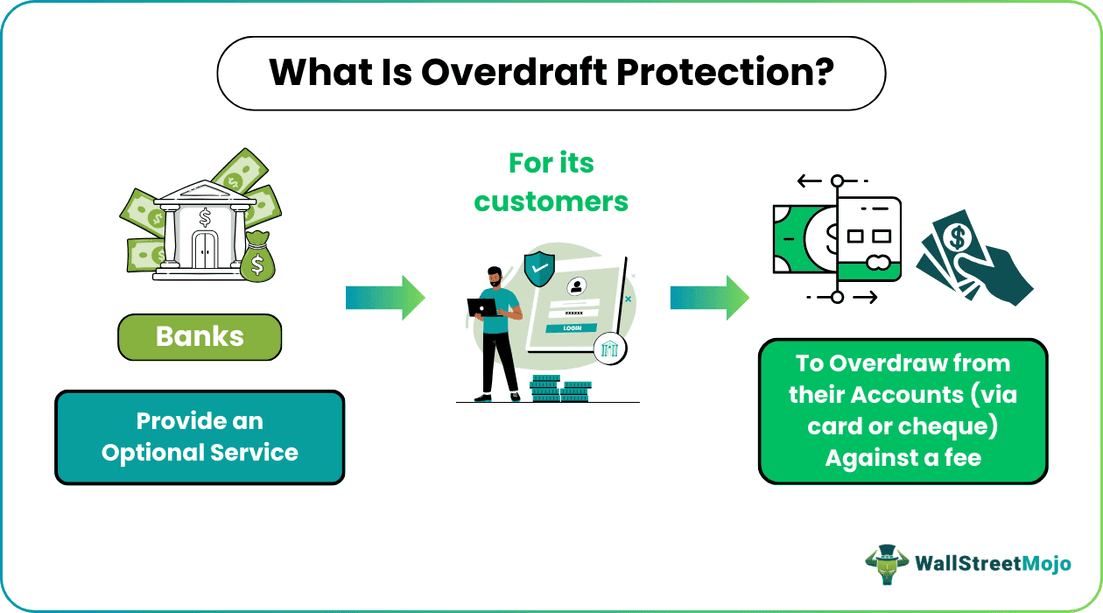

What Is Overdraft Protection?

An overdraft (OD) protection refers to a service banks provide for their customers to clear checks or debit card transactions in case of insufficient funds in the customer’s account. As a result, such a cushion assists account holders in avoiding penalty charges or fees from third-party vendors and minimizes interest charges.

Overdraft protection definition explains a bank overdraft when a customer’s account has insufficient funds to transact a check or payment. Thus, banks with overdraft protection cover the difference amount through a backup account, credit card, line of credit, or any other linked savings account to clear an outstanding payment successfully, even when the customer overdraws.

- Overdraft protection refers to services banks and financial institutions provide to clear checks or other payment transactions in case of insufficient funds.

- It is a service available to customers through an agreement with their respective banks that mentions and approves overdraft fees applicable and interest charges. Thus, available options for backups are credit cards, line of credit, debit cards, or another savings account.

- In case of the absence of an overdraft agreement between an account holder and the bank, the banks charge non-sufficient funds (NSF) fees. Additionally, the bank does not clear the incoming payment due to the absence of an agreement.

How Does Overdraft Protection Work?

Overdraft protection is a service available to banking customers that cushions against check bounce or penalty fees. It is an optional service that allows them to withdraw more than their account balance through a pre-approved route. This pre-approved route links a customer’s checking account to a line of credit, savings account, credit card, etc.

A customer chooses an overdraft protection service to prevent a check bounce and avoid vendor penalties or non-sufficient funds (NSF) charges.

A business with an extremely active payment cycle, such that it incurs regular weekly payments, usually opts for OD protection. It benefits them in two ways – firstly, it ensures smooth business transactions without much hassle with the vendor. Secondly, overdraft protection helps them maintain good credit ratings and scores.

Banks with overdraft protection and a pre-approved agreement with the customers take lesser time to process overdraft loan payments than traditional loans. Thus, a business or individual conducting business activities concerned with making daily or weekly payments and cannot monitor account balance regularly should opt for such a cushion.

Similarly, OD protection is useful for a business when the date for their accounts payable occurs before accounts receivables. Thus, overdraft protection will help overcome the difference between bank account balance and checking amount. Simultaneously, once the account holder receives the payments from its clients, the account balance is restored, and the OD fees get deducted.

Types

Banks with overdraft protection usually provide two options,

- Authorized – In this case, a pre-approved agreement with the bank allows customers to use another savings account or overdraft protection credit card at their convenience to transact differences in amounts. In addition, both entities agree on a borrowing limit, allowing the account holder to clear a transaction even with an insufficient amount. However, an overdraft bank fee is applicable in this case too.

- Unauthorized- An unauthorized OD protection is when an agreement is not signed in advance or the account holder exceeds the borrowing limit. Thus, the account holder attracts an expensive fee and interest charges on such a transaction.

Overdraft Protection Fees

An overdraft fee is applicable when an account holder withdraws more than the available balance, yet the bank transacts it for a fee. It is because a pre-approved agreement exists between both parties that mention and approves the overdraft fee.

In case of the absence of an agreement with the bank, the customer might have to pay non-sufficient fund (NSF) fees. It is applicable daily, weekly, or monthly. However, customers shall pay the overdraft amount, fees, and interest charges when the bank clears an overdraft without an agreement. Otherwise, the overdraft loan amount and interest charges get deducted from the next payment received into the bank account.

Comparatively, the OD fees and interest charges applicable without an agreement with the banks are higher and more expensive.

Similarly, a linked overdraft protection line of credit to the checking account has lower charges than standard overdraft schemes offered by banks. The schemes and programs offered by banks incur OD fees of around $35 per transaction. However, charges worth $35 on each transaction are sometimes very high compared to the actual OD loan amount. Instead, a line of credit linked to a checking account will help deduct only the OD amount and attract a minimal interest rate as an OD fee.

Examples

Let us take some examples to understand why bank overdraft fees apply and the terms and conditions that banks impose. Additionally, let us understand why an account holder resorts to overdraft protection.

Example #1

For instance, the US Bank overdraft protection fee is $36. This bank charges OD fees when the overdraft amount paid by the bank on behalf of the account holder exceeds $5.01. Additionally, the bank charges an OD fee if the account reflects a negative balance of $5.01 or more. Thus, in the case of US Bank OD protection, the bank does not charge a fee on every transaction. But it charges a fee beyond a limit that the account holder exceeds.

Example #2

Max receives her electricity and internet bills on the 20th of each month, which varies from $160 to $170 per month. However, her salary gets credited to her account on the 1st of the next month. Thus, to avoid any penalties or late fees charges from the suppliers or vendors, Max opts for an overdraft protection line of credit for her checking account worth $500.

As a result, she can flexibly issue checks and authorize multiple payments. Simultaneously, her bank provides the cushion to clear them before the penalty date or in case of insufficient funds. Additionally, for a line of credit worth $500, her bank charges an interest rate similar to that applicable on credit card charges. The OD protection helps Max avoid the hefty NSF charges or OD fees per transaction.

Frequently Asked Questions (FAQs)

1.Can you opt out of overdraft protection?

Yes, an individual or entity may opt-out of OD protection to limit their spending if they forget that their debit or ATM card does not have a sufficient amount. Thus, they may reach out to their respective banks to cancel OD protection, which will help them save additional fees and interest charges.

2.What happens if you don’t have overdraft protection?

If there is no OD protection, the bank will decline any payments or transactions incoming into an individual’s checking account and apply charges for non-sufficient funds (NSF). In this case, the bank will not charge an overdraft fee. Additionally, the vendor might charge the buyer an excess fee to the original amount as a penalty. In another situation, the bank might clear an overdraft for an individual but apply hefty OD fees and interest charges superior to standard OD programs.

3.Does overdraft protection affect credit score?

Overdraft protection might affect the score of a user or account holder if they have linked their checking or OD backup to either a credit card or a line of credit from the bank. Thus, if an individual or entity cannot clear OD charges and amounts, it will affect their credit score. Similarly, an individual or entity must have a good credit history to qualify for OD protection credit.

Recommended Articles

This article is a guide to What is Overdraft Protection. Here, we explain its working, types, fees applicable, and some examples. You can also go through our recommended articles on corporate finance –