What Is A Flexible Spending Account (FSA)?

A flexible spending account (FSA) is a health savings bank account that is opened as a requirement of an employer-employee agreement and is used for building the surplus cash position for any emergency needs of the employee, such as medical expenses or any other purpose. The individual or employee contributes the surplus over the years of his regular earnings.

Flexible spending account items offer tax benefits, allowing employees to contribute pre-tax dollars to cover eligible healthcare or dependent care expenses. It also helps individuals save on out-of-pocket medical or childcare costs by using pre-tax funds. However, they often operate on a use-it-or-lose-it rule, where unused funds at the end of the plan year may be forfeited, which is a major drawback.

Flexible Spendings Account Explained

The Flexible Spending Account allows deducting a specific amount from your regular earnings frequently. Such a deduction lowers the taxable income of the individual. Lower taxable income leads to a lower tax liability for the individual as the deduction is made from earnings before taxes.

One of the primary advantages of FSAs is the tax benefits they offer. By contributing to an FSA with pre-tax dollars, employees can reduce their taxable income, resulting in lower overall tax liability. This tax advantage extends to qualified expenses such as medical co-payments, prescription medications, and certain dependent care costs. This reduction in taxable income provides individuals with a valuable opportunity to save on necessary expenditures.

The IRS provides a maximum flexible spending account limit on the contribution to these accounts. If the individual is married, the limit applies separately to the spouse through the spouse’s employer. Per the revised limits in 2020, the per-employee limit for medical expenses is $ 2750 compared to $ 2700 in the calendar year 2019.

Further, the employer may also contribute to the FSA of the employee at their discretion. However, such contribution by the employer is voluntary.

Therefore, FSAs offer a practical and tax-efficient solution for managing healthcare and dependent care expenses. Despite the potential forfeit of unused funds, the tax advantages make FSAs an attractive option for employees seeking to alleviate the financial burden of eligible out-of-pocket costs.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

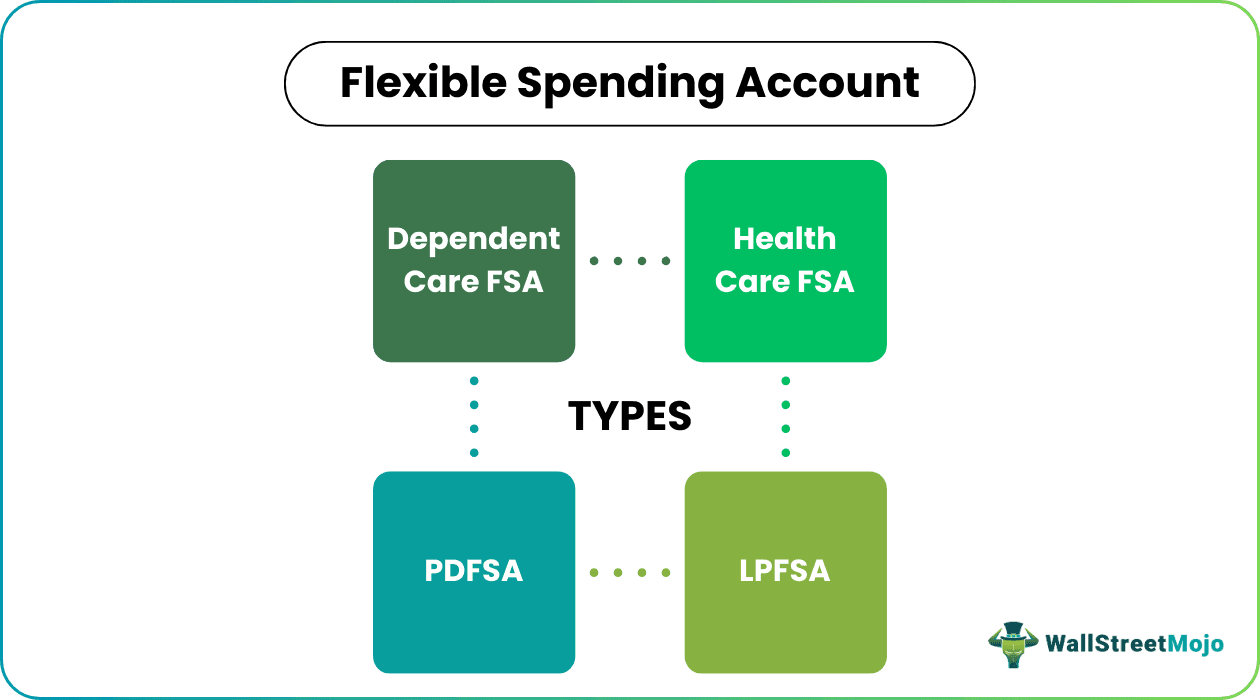

Types

Let us understand the different flexible spending account limits based on their primary nature through the detailed explanation below.

#1 – Dependent Care FSA

It is also called a “dependent care reimbursement account” (DCRA). This account is used only for the expenses of the dependent person. Expenses such as daycare, elderly care or preschool, or any other dependent expenses are allowed under such an account.

#2 – Health Care FSA

The funds accumulated in such an account can be used for medical, vision, dental expenses, or any other qualified expenses. Usage for non-qualified purposes is usually not allowed.

#3 – LPFSA

It stands for Limited Purpose Flexible Spending Account. It can be used along with a health savings account. The available funds can be used for dental or vision expenses or any other purpose as notified.

#4 – PDFSA

It stands for Post Deductible Flexible Spending Account. The IRS allows a minimum deductible amount. These funds are used for section 213d medical expenses if the minimum deduction limit is achieved.

Rules

Understanding the rules and flexible spending account items is essential for the recipient to maximize the benefits of such accounts. Let us understand them through the points below.

- Annual Contribution Limit: Employees must adhere to annual contribution limits set by the Internal Revenue Service (IRS).

- Use-It-or-Lose-It Rule: Many FSAs operate under this rule, stipulating that unused funds at the end of the plan year may be forfeited.

- Grace Period or Rollover: Some plans offer a grace period or limited rollover, allowing employees additional time to spend unused funds or carry a portion into the next plan year.

- Qualified Expenses: Funds can be used for eligible medical and dependent care expenses, as defined by the IRS.

- Enrollment Period: Employees typically enroll during specific periods, often coinciding with the employer’s open enrollment season.

Limit and Grace Period

Let us understand the flexible spending account limits and grace period through the discussion below.

- Even if the account name is “flexible” spending, you must use the funds within the plan year itself. However, the employer may allow grace period of up to 2.5 months over & above the normal tenure to let you use the funds of the said account.

- On the other hand, the employer may allow you to carry forward the amount to $ 500 per annum in the next plan year. The employer will provide either of these options at his discretion.

- If the funds are not utilized within the plan year or the grace period, the pending balance amount is not refunded back to you. Thus, it would be best if you strategically thought over the amount of contribution to be made in FSA.

List

The IRS is very concerned about what is included in the term “medical care.” As per the definition of medical care, it should relate to diagnosis, mitigation or treatment, or prevention of disease, cure, or the care of any part or function of the body. The funds out of FSR are eligible to be spent for the following purposes:

- Purchase of health care products over the counter

- Payments for doctor visits or expenses

- Payment for prescribed medical needs

- Dental expenses

- Vision expenses

- First aid supplies expenses

- Expenses for prescribed eyeglasses

Benefits

The benefits of FSAs are as listed below:

- Urgent medical needs of the employee are taken care of.

- The amount contributed is provided as an exemption from taxable income, which lowers the individual’s taxable income. Lower taxable income results in lower tax liability for the individual.

- Needs for dependent care or children care are also taken care of.

- The employee is saved from the stress of managing the expenses in case of medical emergencies.

Disadvantages

Despite the various benefits, here are the disadvantages:

- There is an expiry period for the amount deposited. The hard-earned money is lost if you do not use the funds within the said period. However, the employer may provide an option for a grace period or carry forward the amount.

- There is an upper cap of $ 2750 (for the calendar year 2020). If the actual expenses exceed the said amount, the employee needs to bear the remaining amount.

- Flexible savings accounts are linked to the employer. If you leave the job, you cannot carry forward the benefits to the new employer.

- No deduction is allowed for actual spending of the amount.

Flexible Savings Account Vs Health Savings Account

Let us understand the distinctions between FSAs and HSAs through the comparative points below.

Flexible Spending Account

- FSAs are offered by employers as part of employee benefits.

- Employees contribute pre-tax dollars, reducing their taxable income.

- Typically, there’s a use-it-or-lose-it rule, where unused funds at the end of the plan year may be forfeited, though some plans may allow a limited rollover or grace period.

- Funds can be used for eligible medical and dependent care expenses defined by the IRS.

- Employers have more control over plan design, including contribution limits and eligible expenses.

Health Savings Account

- Both employees and employers can contribute to HSAs, with contributions made with pre-tax dollars.

- HSAs offer a rollover feature, allowing funds to accumulate and carry over from year to year, even if the individual changes employers.

- HSAs provide a triple tax advantage – contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

- To qualify for an HSA, individuals must be enrolled in a high-deductible health plan (HDHP).

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This has been a guide to What is a Flexible Spending Account & its Definition. Here we discuss its types, how it works, benefits and disadvantages. You can learn more about it from the following articles –