What Is Buy Now Pay Later (BNPL)?

Buy now pay later (BNPL) is a payment structure that allows individuals to buy any item today with the condition of paying for it in the future. Companies use it to boost their sales by letting customers get access to things they want without worrying about money.

BNPL gives customers time flexibility in making payments. Also, they find it easy to avail as buy now pay later apps do not charge any interest. Therefore, it creates higher customer lifetime value for companies, retailers, and merchants. However, it can attract a penalty for payment failure.

- Buy now pay later allows individuals to make instant purchases without making on-the-spot payments. It is a kind of credit facility with an easy and fast setup.

- BNPL enables zero interest rates and allows flexible payments.

- Some BNPL companies declare exclusive offers to individuals for opting to buy now and pay later.

- Merchants must pay some fees to these companies, ranging from 2% to 6%. Sezzle, Afterpay, Paypal Pay, and Amazon Pay are some examples of BNPL providers.

How Does Buy Now Pay Later Work?

Buy now, pay later finance with a credit facility for customers buying items in the present day. It has no interest attached to it. Many BNPL companies call it a Point of Sale (POS) system, which lets customers buy things immediately. Also, the buyers benefit immensely from this system in terms of higher profits.

The earlier evidence of buy now pays later dates back to the 19th century. Merchants supplied new items and products in the market. However, customers did not have enough funds to buy them. Thus, in the 1840s, shopkeepers and merchants allowed people to buy items (furniture, pianos, and farm equipment) on a credit basis. As a result, customers could easily buy items and pay on a certain future date. That’s the reason why citizens referred to it as an installment plan. Likewise, grocery vendors in India followed the same “buy now, pay later” system. This approach helped them to boost their sales.

Later in the early 21st century, buy now pay later companies, including e-commerce and fintech firms, penned a new name for this concept. They integrated this feature into online shops and e-commerce sites. They added various offers and zero interest rates to encourage participation. Moreover, it allowed customers to receive an instant credit facility at the POS and pay later. Furthermore, customers could use buy now pay later for flights.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

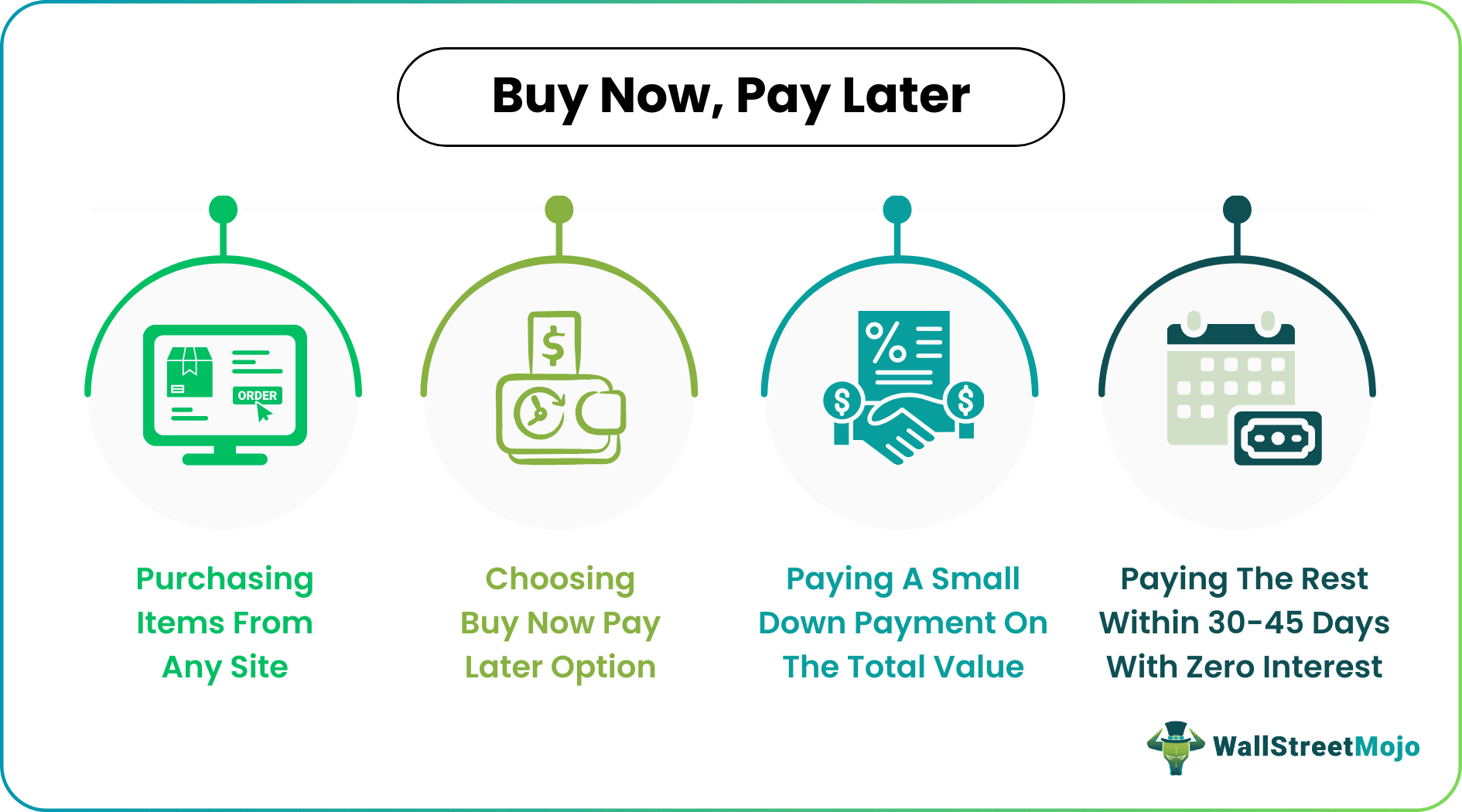

Buy Now, Pay Later Process

The process for availing of BNPL service is very simple and convenient. Financial technology companies like Sezzle, Afterpay, Paypal Pay, and Amazon Pay are some examples of BNPL providers. There are two types of BNPL, loans with and without interest. The only difference is that customers often get charged if they fail to pay. Following are the steps for demonstrating how BNPL works:

- Pick any item from any retailer and drop it into the cart.

- At the checkout point, select the buy now, pay later option.

- BNPL apps will ask the buyer to pay a small down payment (mostly 25%) if eligible.

- Then, the buyer has to pay the rest in installments. However, there would not be any interest charged for the purchase.

- The amount can also get deducted from the buyer’s bank account, credit, or debit card.

Examples

Let us look at some buy now, pay later examples to comprehend the concept better:

Example #1

Suppose Calvin is a music producer buying new equipment for his studio but lacks funds. His friend Alexa introduced him to buy now pay later companies. He found some affordable equipment through a merchant on the suggested e-commerce site. So, Calvin opted to buy now and pay later for electronics at the checkout point.

He was able to purchase the microphone at a small credit facility for 30-45 days. On the cost of $600, Calvin paid a small down payment of $150. During this installment period, he needs to pay the rest ($450) to buy now pay later apps. On failure, the lender might charge a late fee to Calvin.

Similarly, if he had opted for a credit card, he would have paid an extra charge (interest) which is missing in this case.

Example #2

According to a recent survey by DebtHammer, more than 45% of Americans have signed up for the BNPL plan compared to last year (April 2021), which was 41%. In addition, 65% of the respondents felt BNPL was a vital source of credit financing as a last resort. Among all people, generation Z and millennials had the highest consumption of BNPL services.

Another report by Adobe Analytics states that many people in the United States are using BNPL apps like Sezzle, Afterpay, Plan It, and PayPal’s Pay for making future payments. In November 2021, the BNPL revenue rose by 422% compared to 2020.

BNPL vs Credit Cards

Although BNPL and Credit cards offer credit facilities, there is a thin line of difference between them. The former does not charge any interest. However, the latter does charge any interest. The latter might appeal to customers for credit history, while the former denies doing so. While the former allows customers to go without interest for months, the latter charges fixed interest rates.

| BNPL | Credit Cards |

|---|---|

| No interest rates | Fixed Interest rates |

| No credit history | Good credit history is mandatory |

| Very few fintech companies offer them | Wide acceptance |

| Easier approvals | Slightly difficult |

Pros And Cons

BNPL has a lot to offer to the consumers as well as the merchants. Consumers can use it to purchase items in shortage of funds. They get a credit facility of 1-1.5 months for paying the amount. There is no interest charged to the consumer. However, there are certain cons to this system. Although merchants get many sales, they have to pay high fees to the BNPL companies ranging from 2 to 6%.

Customers do not have to pay interest, but it will attract late fees if they fail to make payments. Also, this system makes customers make impulsive purchases resulting in increased debt. For example, if a customer opts to buy now pay later for electronics, he will be tempted to buy other items, too, even though he does not have money.

| Pros | Cons |

|---|---|

| Convenient | Higher merchant fees |

| Fast setup and easy approval | Encourages consumer debt |

| Interest-free terms | Higher spending |

| Exclusive offers | Impulsive towards purchases |

| Increase in credit limit | Attracts penalty on failure |

| Small down payments |

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

Does buy now pay later affect credit score?

Yes, BNPL does affect the credit score of an individual. For example, a customer’s credit score increases when they repay loans on time. In contrast, their credit score will turn negative if they fail to do so.

How to buy now pay later companies make money?

There are two sources for buy now pay later companies to generate revenue. Firstly, they charge the vendors and merchants a transaction fee ranging between 2-8%. And the second source is from the customers in the form of late fees.

Why is buy now pay later so popular?

The main reason for popularizing BNPL is the interest-free credit facility. Millennials and Generation Z often lack credit history but always look for short-term credit. Also, they are the major ones to make purchases, for example, using buy now pay later for flights. Thus, it makes it a good option for them.

What credit score do you need to buy now, pay later?

Most BNPL companies hardly check for credit scores, so it is easy to access credit facilities. However, not making timely payments can lead to increased debt.

Recommended Articles

This has been a guide to What is Buy Now, Pay Later. Here, we explain the BNPL process, its examples, pros & cons, and comparisons with credit cards. You may also find some useful articles here: