Part of our Banking Products guide

Letter of Credit Meaning

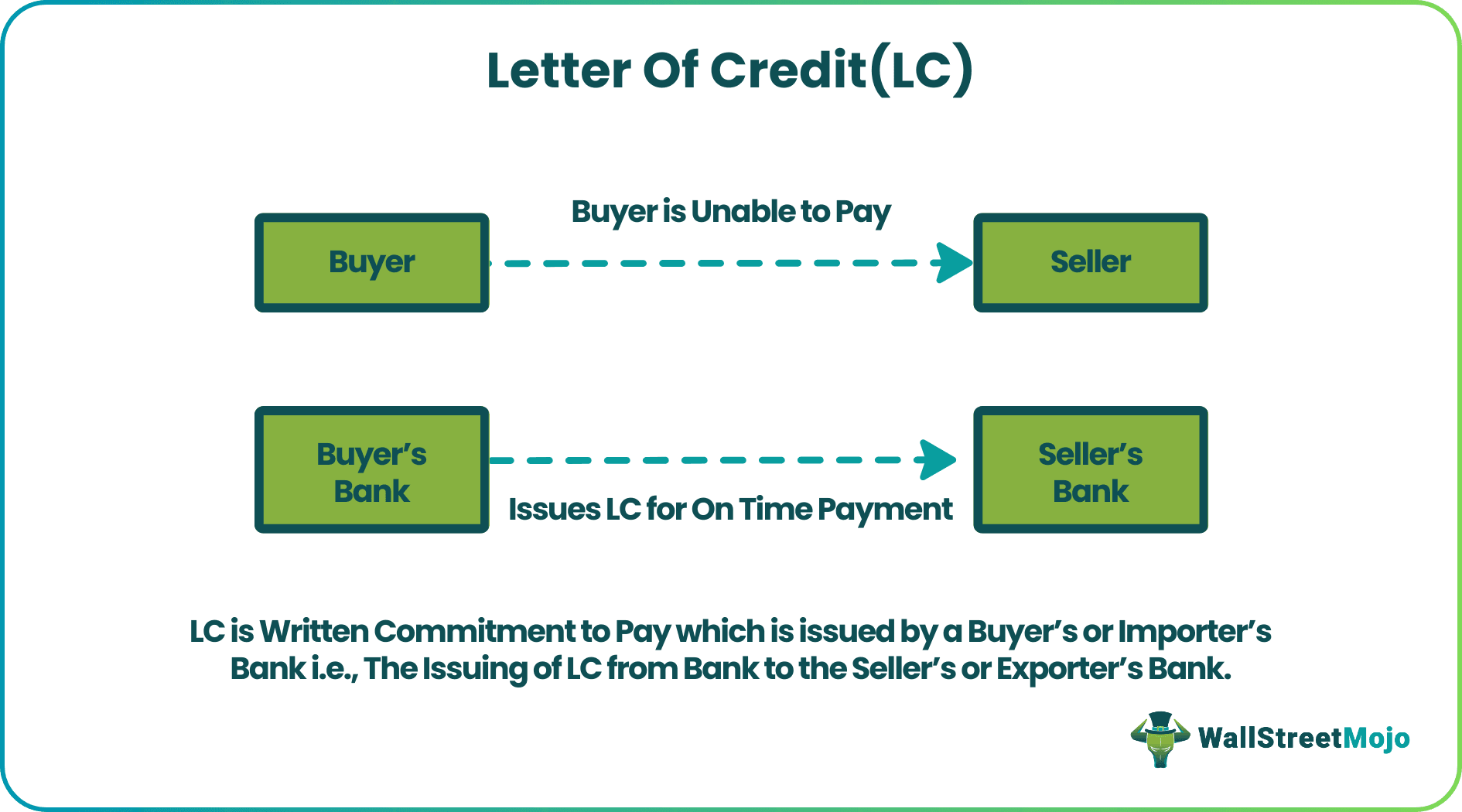

A Letter of Credit (LC) is issued by a buyer’s bank to ensure timely, full payment to the seller. If buyers default, the bank pays sellers on their behalf. Therefore, an LC is used for mitigating credit risks in international trading.

It is a commonly adopted practice in international trade when there is substantial geographical distance or a lack of trust among the parties. It acts as a negotiation instrument. Banks charge specific fees to back the buyers’ purchases. LCs are also known as documentary credit or bankers’ credit.

- A letter of credit (LC) is a bank-issued document that affirms the seller. On behalf of the buyer, the bank guarantees payment upon delivery of the goods or services.

- It is a form of negotiable instrument whereby the buyer makes an unconditional promise to pay. The seller or beneficiary can also transfer the LC to another party to further mitigate their liability.

- If the buyer doesn’t pay the amount, this burden falls upon the issuing bank. Therefore, for issuing LCs, banks charge the buyer a particular percentage as a fee.

Letter of Credit Explained

A letter of Credit (LC) is a legal document backed and issued by the bank. Therefore, it is an essential piece of paper for the reliable export and import of products or services. It ensures that both the buyer and the seller fulfill the commitments stated in the sales contract.

Usually, the seller demands a credit letter while entering a sales contract. The buyer requests the bank to issue an LC by submitting a written application and relevant documents. The issuing bank communicates with the advisory bank and formulates a letter of credit for the buyer. As soon as the buyer receives the goods or service, the seller encashes the LC.

Along with the LC, the seller needs to furnish various documents like an airway bill, packing list, commercial invoice, insurance certificate, certificate of origin, certificate of inspection, and lading bill. Sellers get paid only after providing all those documents. The issuing bank acquires the amount from the buyer. Subsequently, the amount is released in favor of the seller, beneficiary, or the beneficiary’s negotiating bank. If the buyer defaults on payment, the issuing bank is responsible for paying off the due amount. The buyers’ Banks impose a certain fee (usually a specific percentage of the LC amount) for extending these services.

Features

A letter of Credit has the following characteristics:

- Issued by Buyer’s Bank: An LC is released by the buyer’s bank to the seller and is a formal document that comprises all the conditions of the deal.

- Transferability: The LC can be assigned or transferred to a third party by the beneficiary as a mode of payment, and this third party can get it encashed on the due date. Further, it can be transferred several times and remains valid.

- Revocability: Some letters of credit are revocable, and therefore these can be canceled at any time; however, most credit letters are irrevocable.

- Maturity: The LC is a time draft which means it has a due date on which the beneficiary can encash the amount from the issuing bank.

- Negotiability: It is a negotiable instrument whereby the parties can discuss and amend the terms and conditions of the LC. Similar to other negotiable instruments, the letters of credit bear an unconditional promise to pay a certain sum on the due date or demand of the beneficiary.

Letter of Credit (LC) – Video Explanation

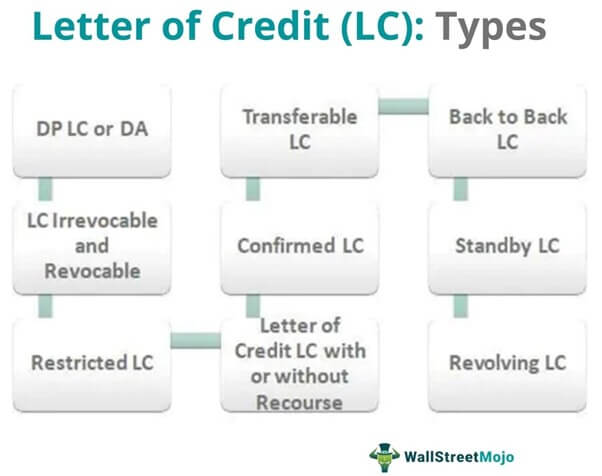

Types of Letters of Credit

There are various types of letters of Credit (LC) used in international dealings. They are as follows:

#1 – DP LC or DA

In this form of LC, the payment must be made on the date of maturity following the credit terms. This is the type of LC where payment is given against documents on presentation.

After receiving and examining the payment-related documents, the buyer is handed over the title for the goods. The buyer then pays the predetermined amount paid on the due date mentioned in the LC. This is also referred to as the “maturity” of the Letter of Credit (LC).

#2 – LC Irrevocable and Revocable

The irrevocable letter of credit can be canceled or amended only with the beneficiary’s consent. A revocable LC can be withdrawn or amended at any time without giving prior notice to the beneficiary. Most LCs are irrevocable.

#3 – Restricted LC

Here, only a nominated bank is authorized to accept, pay, or negotiate the terms of an LC. As nominated, the authorization for LC is restricted to a particular bank.

#4 – LC with or without Recourse

A confirmed LC is without recourse to the beneficiary. But an Unconfirmed or negotiable LC is always with recourse to the beneficiary. For LCs with recourse, the reimbursement is negotiated between a customer and its nominated bank. Reimbursements occur when the buyer defaults.

#5 – Confirmed LC

A confirmed LC is one where the advising bank makes additional confirmation at the request of the issuing bank that payment will be made. Hence the advising bank is equally responsible for payment. Therefore, the confirming or advising bank must bear the cost if the buyer doesn’t pay the sum to the beneficiary.

#6 – Transferable LC

The beneficiary can transfer such an LC in whole or in parts to a second beneficiary, usually supplied to the seller. However, the second beneficiary cannot transfer it further to another beneficiary.

#7 – Back-to-Back LC

In this type of LC, the second LC is opened by the beneficiary in the name of the second beneficiary, wherein the first LC is kept as security for the second one. This type of Letter of Credit (LC) is generally offered to suppliers.

#8 – Standby LC

This is an LC, which is like a performance bond or guarantee issued by the bank. Therefore, the beneficiary can claim it by providing the required documents. A list of required documents is also mentioned in the LC.

#9 – Revolving LC

A revolving LC covers multiple transactions over a period. For example, it can be used for regular shipments. The same commodity is sold to the same buyer repeatedly by one seller. In such an instance, the buyer can use a revolving LC.

Advantages and Disadvantages

Thanks to Letters of Credit (LCs), buyers can easily avail of goods and services from international sellers. The buyers’ creditworthiness improves as their transactions are secured by the reputed guarantors, i.e., banks. The sellers no longer fear the risk associated with the buyers’ credibility and chances of non-payment.

It is beneficial for both the buyer and seller. LCs build trust between the parties. Also, it is amendable, i.e., the terms and conditions of LCs can be changed at any time with the mutual consent of both parties. Further, it reduces the chances of conflict between the trading parties. LCs, simplify negotiations.

However, the LC increases the buyers’ expenses. Banks impose a specific fee for formulating an LC. LCs bind both the buyer and seller to fulfill contractual terms within a time frame. Moreover, the bank has no control over the seller’s quality of goods or services sent to the buyer.

Letter of Credit Example

Consider the hypothetical example to better understand a letter of Credit (LC). ABC Ltd. is a travel bag manufacturer in the US. The company agrees to provide 1000 travel bags to M/S XYZ, a wholesaler in Singapore but requested a letter of Credit from the latter. ABC Ltd. nominated EFG bank as its negotiating bank, and XUV bank is the advisory bank of PQR bank.

Let us go through the whole process comprising the following steps:

- M/S XYZ applies with PQR bank to get an LC.

- The bank asks for relevant documents pertaining to the buyer’s firm.

- M/S XYZ provides the required documents.

- PQR bank submits these documents to the advisory bank XUV.

- XUV bank verifies and cross-checks these documents.

- Subsequently, PQR bank issues a letter of credit (LC) for an amount of $10000 in favor of ABC Ltd.

- ABC Ltd. Then hands over the LC to its negotiating bank EFG.

- Subsequently, ABC Ltd. ships the goods consignment.

- EFG bank simultaneously sends the documents of shipment and other details to the PQR bank. These documents are then forwarded to M/S XYZ for confirmation.

- M/S XYZ authenticates and deposits the amount with PQR bank.

- PQR bank releases the payment to EFG bank.

Frequently Asked Questions (FAQs)

What is a Letter of Credit?

A letter of Credit (LC) is a negotiable document issued by the buyer’s bank that pledges the due amount on maturity to the seller (beneficiary) for the buyer’s purchase of goods or services.

How does a letter of credit work?

The buyer applies for an LC with the issuing bank. The issuing bank offers the LC in favor of the seller in exchange for a specific fee. The issuing bank releases the payment when the seller delivers the goods consignment or services to the buyer. However, if the buyer fails to pay, then the issuing bank has to bear the cost.

What is the LC limit?

The buyer needs to maintain at least 50% of the revolving credit commitments at the time of issuance. This limit can be higher or lower than this, as per the norms of the issuing bank.

Recommended Articles

This has been a Guide to what a Letter of Credit (LC) is and its Meaning. Here we discuss Letter of Credit types, features, how it works, examples, advantages, and disadvantages. You may also have a look at these articles below to learn more about Credit –