Part of our Banking Products guide

What Is Credit Card Settlement?

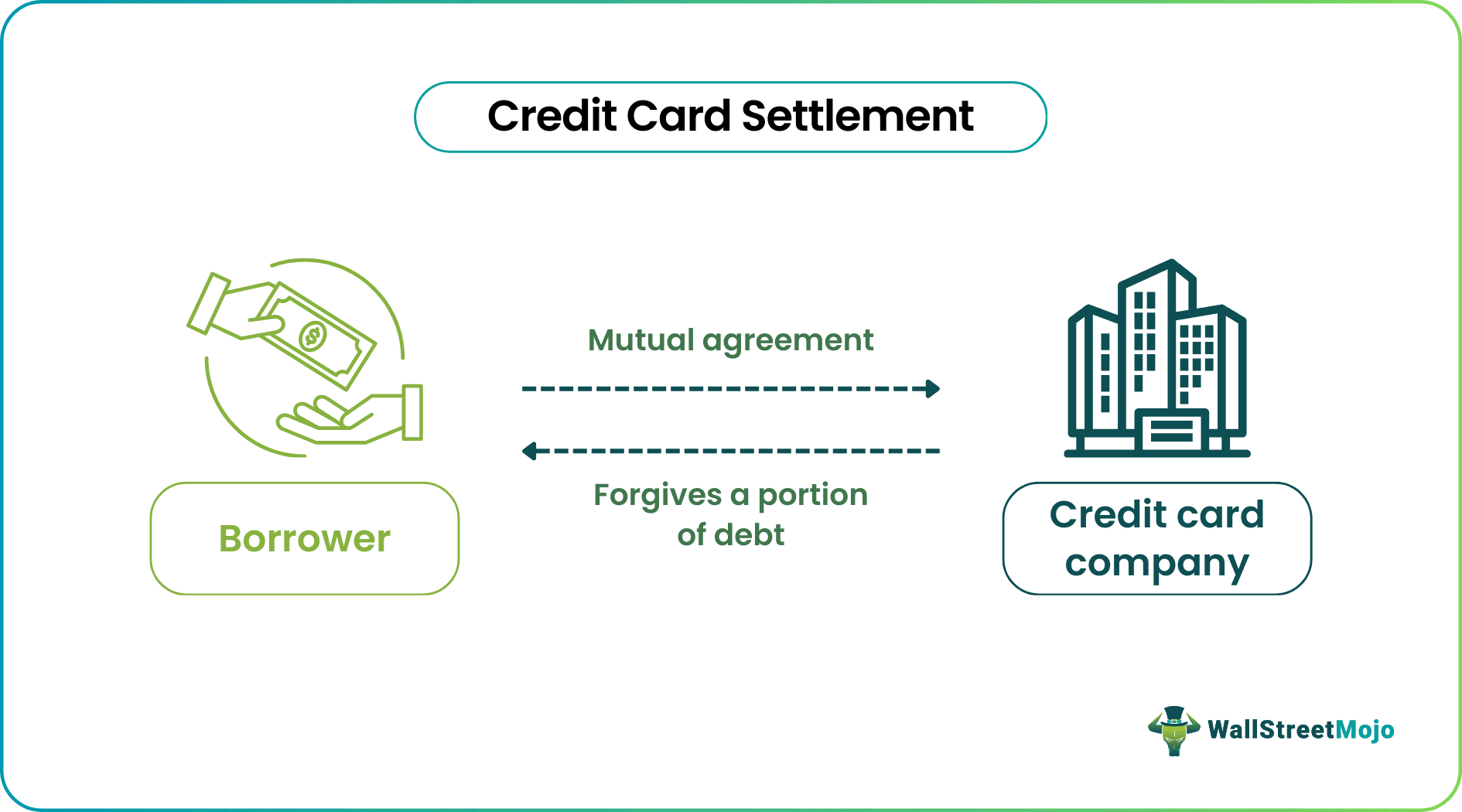

Credit card settlement is a process through which a credit card company forgives a portion of a cardholder’s debt, and in return, the latter pays the remaining amount owed to the former. Cardholders opt for this route to get out of serious credit card debt.

Individuals can repay the outstanding amount in one go. Alternatively, they can make a series of payments to the card issuer. The repayment depends on the agreement between the two parties. Credit card issuers cannot seize an individual’s assets if they fail to repay the dues. Hence, they negotiate a settlement with their customers to recoup as much as possible.

- Credit card settlement meaning refers to an agreement between a credit card company and its customer in which the former forgives a part of the unpaid amount and considers a reduced payment made by the cardholder as full payment.

- The Internal Revenue Service (IRS) deems the forgiven portion of a credit card debt as income. Hence, individuals may have to pay taxes depending on the principal amount.

- This is one of the options available to people who want to avoid being sued for debt. However, it negatively affects an individual’s credit score, and settlement agencies usually charge a high fee.

- One can overcome significant debt and avoid bankruptcy by negotiating a settlement.

Credit Card Settlement Explained

Credit card settlement meaning refers to an agreement between a credit card issuer and its customer where the former writes off a part of the outstanding debt. In exchange, the latter usually pays the remaining amount through a lump sum payment. Individuals aim to pay less than they owe by negotiating a settlement with the card issuer.

One can refer to the following points to understand how the credit card settlement process works.

- A cardholder stops paying their credit card bills.

- The person transfers the amount they would have used to pay the bills to a savings account. Usually, a debt settlement agency manages this account.

- After many months, when the amount due on the credit card is significant, the settlement agency gets in touch with the card issuer. It proposes to settle the debt via a lump sum payment using the funds in the savings account.

- If the credit card company accepts the proposal, they write off a portion of the debt.

Individuals must remember that they may have to pay tax on the amount saved in the bank account. In addition, they must pay the fees charged by the settlement agency. Sometimes, credit card companies may not accept the proposal. In other words, they refuse to settle. In that case, they take the customer to court.

Example

Let us say that David owes $10,000 to a credit card company CredEase. However, he can only repay a maximum of $6,000. If this is acceptable to CredEase, it may agree to settle the loan and write off $4,000. The card issuer will regard $6,000 as full payment. CredEase closes the credit card account after the settlement process is complete.

Taxes

Before opting for the credit card settlement process, individuals must consider potential tax liabilities. This is because the card issuer has a legal obligation to report the forgiven or written-off debt (excluding the finance charges and forgiven fees) to the Internal Revenue Service (IRS).

The federal tax agency considers the forgiven amount as income for cardholders as they technically borrowed it and did not make repayment. Therefore, depending on the principal amount forgiven, one may owe taxes. Hence, after the credit card issuer agrees to settle the debt, the cardholder will likely receive Form 1099-C via mail.

Advantages And Disadvantages

Let us look at the benefits and limitations of the credit card settlement process.

Advantages

- It enables one to get relief from serious debt and repay the outstanding borrowings faster.

- One can avoid bankruptcy by negotiating a settlement with the credit card provider.

- Individuals can take this route to avoid getting sued for their debt.

- The credit card company will not send the debt to collections.

Disadvantages

- Credit card settlement agencies usually charge a significant amount.

- It negatively impacts an individual’s credit score. This, in turn, affects employment opportunities, credit availability, and loan terms in the future.

- The creditor may refuse to negotiate a settlement.

Another noteworthy disadvantage of credit card settlement is that even if the card issuer agrees to settle the debt, individuals still may have to pay taxes on the amount forgiven as the IRS considers it an income.

Credit Card Settlement vs Credit Card Capture vs Paid In Full

Individuals unfamiliar with credit card capture, paid in full, and credit card settlement might find the terms confusing. One must understand their critical differences to avoid confusion and get a clear idea. So, let us look at them.

| Credit Card Settlement | Credit Card Capture | Paid In Full |

|---|---|---|

| In this case, a credit card issuer agrees to write off a portion of a debt in exchange for the cardholder repaying the remaining amount. | It is the process of completing a credit card purchase by settling or capturing the funds for the transaction. | This term applies to loans after a borrower repays the entire amount payable to the lender or creditor. |

| It negatively impacts one’s credit score. | This process does not impact a person’s credit score. | If an individual pays the outstanding amount in full, it positively impacts their credit score. |

Want a smarter way to bank on the go? Revolut offers a user-friendly app with global access, crypto and stock trading, and innovative budgeting tools—all in one powerful platform.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. Can I get loan after credit card settlement?

Generally, debt settlements remain on a credit report for several years. Hence, one may find it difficult to find a lender to provide financial assistance immediately. Moreover, even if banks give a loan, they may not sanction a high loan amount or offer favorable terms.

2. Is credit card settlement a good idea?

Although settling credit card debt is better than not paying, one should always try their best to pay off a debt in full. This is because the ‘settled’ status in a credit report negatively impacts one’s credit profile. In addition, banks and other lenders usually do not provide loans immediately or offer the best loan terms if a person’s credit history includes a settlement.

3. What happens after credit card settlement?

After the settlement process is complete, the credit card company cancels the credit card. The person making the payment becomes free of the dues, but the settlement significantly affects their credit score.

4. How long does credit card settlement stay on credit report?

A settled account remains on a person’s credit history for seven years from the settlement date.

Recommended Articles

This article has been a guide to what is Credit Card Settlement. We explain its taxation, advantages, disadvantages, comparison with paid in full, and an example. You may also find some useful articles here –