What Is Banker’s Acceptance?

Banker’s Acceptance refers to the consent and promise that a bank gives or makes to a party exporting products to its native nation. In the process, the bank (instead of the account holder) guarantees for the payments at a future date, thereby ensuring smooth export and import relationship between countries without any financial disturbance.

Through banker’s acceptance, the bank accepts the liability to pay the third party if the account holder defaults. It is commonly used in cross-border trade to assure exporters against counterparty default risk. This helps exporters trust the country importing the goods on financial terms as the former knows they would receive the payment anyway.

- Banker’s acceptance is a financial instrument in which a bank guarantees payment to a third party at a future date, rather than the account holder guaranteeing the payment.

- The bank assumes responsibility for paying the third party if the account holder defaults on the payment.

- Banker’s acceptance is typically used in cross-border trade to protect exporters from counterparty default risk.

- The bank assesses the account holder’s credibility on various grounds, including their credit history. If the account holder meets the bank’s criteria, the bank will assume responsibility on their behalf.

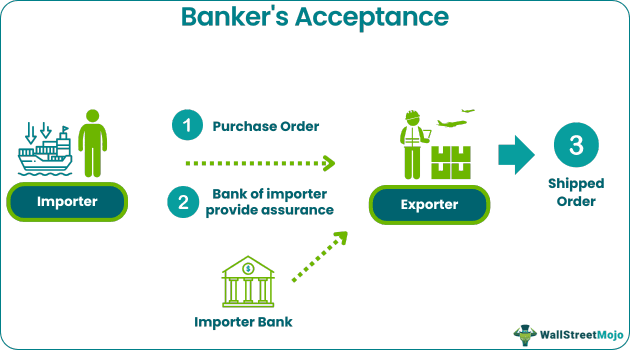

How Does Banker’s Acceptance Work?

Banker’s acceptance, as the name, suggests is the scenario where the bank of one party agrees to pay for the products received from another party in case the former is unable to do so. This guarantee coming from the bank itself enables the exporters or the sellers to trust the importers and transport goods to them even if the payment is to be made at a future date. In short, this arrangement helps avoid any disturbance in the trade relations of two nations.

Here, an importer enters into a transaction with the exporter from another country. A business entity that wants to enter into a high-value transaction will approach its banker with an account. It must provide details of the trade to be executed and the amount of credit required.

The banker will assess the credibility of the account holder on various grounds, particularly the account holder’s credit history. If it is satisfied on all fronts, it will accept the liability on behalf of the account holder. The account holders must prove sufficient funds on the execution date and pay for the charges to the bank.

The exporter is ready to supply the whole quantity to the port of the importer country. First, however, the exporter needs an assurance of payment. On the other hand, the importer is doubtful whether the exporter will supply the goods with the correct quantity and appropriate quality after full payment is made to the exporter.

Hence, both the parties have some transaction-related risks. Here is where a banker’s acceptance comes into play.

The importer’s banker assures the banker’s acceptance to the exporter. The exporter is reasonably assured of the payment as the bank guarantees it. It facilitates trade between the parties. In case of any concerns about the quality and/or quantity of the goods, the exporter and importer can decide accordingly.

It provides financial support to importers as well. If everything goes well, the banker clears the payment on the due date specified on the banker’s acceptance. The financial banker will charge a commission to the account holder for such a service.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Characteristics

Banker’s acceptance is one of the most significant concepts in the world of export-import. It allows two parties to trust each other with the items sold and the payments made. However, for this financial instrument to be active, there are a few things that one must be aware of. The characteristics that define how and in which scenarios such options work include the following:

- The banker’s acceptance is issued against the parties’ creditworthiness. The banker receives a commission for facilitating such trade. Thus, the bank’s profit is involved in the successful execution of the contract.

- The banker’s acceptance is available only for customers with good credit history. Such customers are usually corporate entities with good credit history. Such creditworthiness is also linked to the investment in bonds.

- Another characteristic is its marketability. It is a short-term debt instrument that can trade in the market, i.e., sell it. In such a case, the liability to pay for the debt is transferred to an altogether third party. Such transfer is feasible only due to the entity’s ethical practice and stringent credit evaluation rules.

- Banker’s acceptance is known for its easy conversion from instrument to real hard money. In addition, it is said to have a higher liquidity since the amount is passed from the bank holder’s account to the debit account at the time of the instrument’s creation. Thus, there is confirmation of liquidity with lower risk.

Examples

Let us consider the following instances to understand the concept better and also check how it actually works in a practical scenario:

Example #1

Suppose a U.S. company wants to purchase 1,000 units of mobiles at an accumulated price of $1 million from a German company. The U.S. bankers issue bankers’ acceptance to the German firm for a credit period of 40 days. Once the exporter ships the mobiles, it provides the evidence (i.e., documents) to the US bank and receives the banker’s acceptance.

The German firm can hold the bill until maturity or discount it today through the German bank. By ignoring it, it receives the amount today with a cut of 6.235%, i.e., $9,37,650. That is called discounting of the bill.

The German banker has further options to hold until maturity to receive $1 million or discount it further to another party. That goes on till the banker’s acceptance is held till maturity. The ultimate holder gets the face value.

Example 2

Canadian Fixed-Income Forum (CFIF) published a whitepaper in January 2023 stating how Canadian Dollar Offer Rate cessation will be impact banker’s acceptance (BA) to a great extent. According to the report, these BAs would not exist and hence, the market participants must look for effective options that could replace BAs.

BAs, occupying a significant place in the Canadian market, would be tough to replace and hence around 80 industry experts joined the workshop conducted by the CFIF to explore alternatives of this process. They all agreed to develop new types of investment products that would make it easier for people to transition from BAs.

With the CDOR cessation date nearing, the BAs issuance rate would drop relatively. The Canadian market, as a result, is likely to witness the efficient issuance of the banker’s acceptance by the end of 2023. However, this would be little or no more active starting June 2024.

Banker’s Acceptance Rates and Marketability

Due to the banker’s acceptance of the liability to pay for the debt guaranteed by the bank, the instrument is assumed to be a safe investment by the market players. Thus, they can trade such an instrument at a discount to face. The discount to face value is nothing but the interest rate charged at a nominal spread over the U.S. treasury bills.

For example, say the banker has an acceptance liability of $1,50,000 for the trade execution. The holder (exporter) to whom such assurance is provided can sell the instrument in the secondary market at $1,45,000. This way, the liability of bankers does not change. Such trading in the secondary market proves the marketability of the instrument.

Benefits

The concept of banker’s acceptance appears to be a blessing for parties that are unable to pay immediately and need goods and products from a seller on credit. When the banks take the liability to pay back if the party defaults, it becomes easier for the sellers to trust them and hence, the deal or transaction happens smoothly.

Listed below are some of the major advantages that this process brings along:

- The account holder (importer) against whose default the assurance is provided need not pay the amount in advance. The liability amount gets debited only on the due date of payment.

- The banker’s acceptance facilitates trade between the two unknown parties. In addition, it helps build trust between the business entities.

- The exporter is assured about its payment, and the importer is assured about the timely receipt of goods.

- The exporter need not worry about the default of a country’s financial institution The exporter is assured about its payment, and the importer is assured about the timely receipt of goods.

- The exporter is assured about its payment, and the importer is assured about the timely receipt of goods.

- Guarantees in payment promote the business.

Risks

The process of banker’s acceptance involves guarantees from the bank on behalf of its customers. As the deal involves financial promises to be kept for a future date, it is important to have some restrictions imposed on the parties taking up such services or consent. Hence, there are a few limitations or challenges associated with banker’s acceptance that one must know about before opting for such options.

Let us have a look at some of them in brief:

- The primary risk of a financial banker is the inability to pay the account holder. The banker has accepted the risk of default. The bank will have to honor the payment even if the account holder does not maintain sufficient funds on the payment date. That is the reason why all banks do not issue bankers’ acceptance.

- To hedge the banker’s risk, it may ask the importer to provide collateral security in the bank’s name.

- Even if the banker has performed the fundamental check, it still faces the liquidity risk from the importer.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. Is a banker’s acceptance an asset?

Yes, a banker’s acceptance is an asset. It is a type of short-term promissory note that represents a promise by a bank to pay a specified amount at a future date. Bankers’ acceptances are commonly used in international trade to facilitate the payment of goods and services.

2. What is a banker’s acceptance vs. commercial paper?

Banker’s acceptance and commercial paper are both short-term financing instruments that are used by businesses to raise capital. However, a banker’s acceptance is a financial instrument that involves a bank accepting an obligation to pay a specified amount on a future date. At the same time, commercial paper is a short-term promissory note issued by a corporation.

3. Is the banker’s acceptance the same as a letter of credit?

No, a banker’s acceptance is different from a letter of credit. A banker’s acceptance is a short-term financing instrument that involves a bank accepting an obligation to pay a specified amount on a future date. On the other hand, a letter of credit is a financial instrument that a bank issues on behalf of a buyer to guarantee payment to a seller in a transaction.

Recommended Articles

This article has been a guide to what is Banker’s Acceptance. Here, we explain the concept along with its examples, characteristics, benefits, and risks. You may learn more about financing from the following articles: –