Part of our Revenue Recognition guide

Examples of Deferred Revenue

Deferred revenue or unearned revenue is the number of advance payments that the company has received for the goods or services that are still pending delivery or provision. Its examples include an annual plan for the mobile connection, prepaid insurance policies, etc.

We can find thousands of examples of Deferred Revenues, but some of them are so important to understand as these kinds of transactions most of the firms will have in their books.

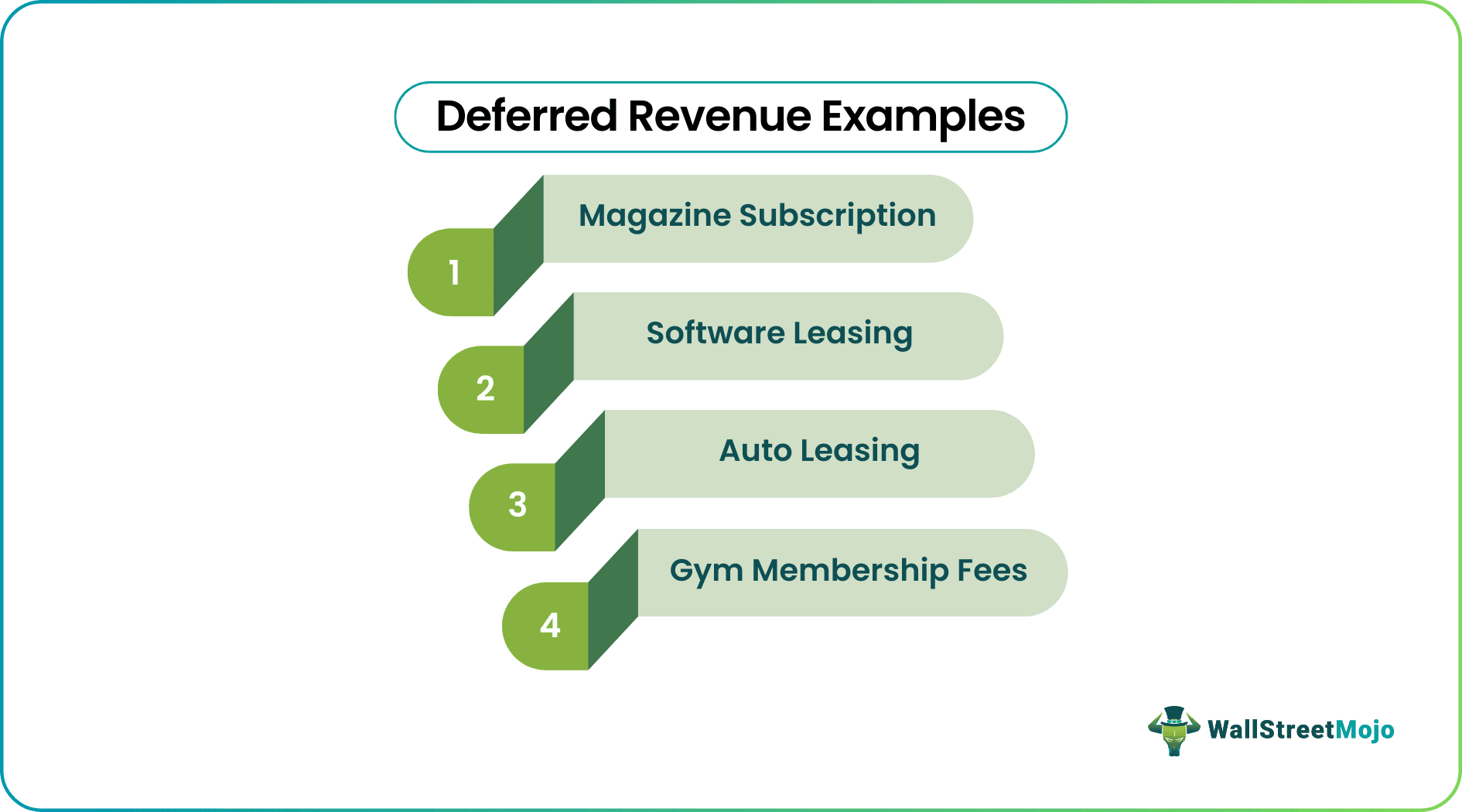

Top 4 Examples of Deferred Revenue

Example #1 – Magazine Subscription

Let’s take an example of a magazine company that publishes a monthly magazine but collects its yearly subscription in advance. The whole amount of the yearly subscription is not part of the monthly revenue. Still, the company earns part of this subscription amount monthly and transfers a monthly portion of this subscription each month for the calculation monthly P&L account.

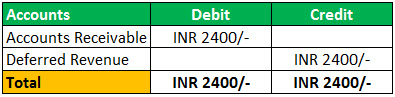

Suppose a monthly subscription to the magazine is INR 200/- but the company collects INR 2400/- from the customer as an advance for a yearly subscription. Each month, the company will transfer INR 200/- from INR 2400/- to the monthly P&L account once the company delivers the magazine’s monthly publication to the customer, and the rest amount will become deferred revenue in the Balance sheet for the next month. So, each month the company will transfer the 1/12 portion of the total amount collected from the customer from Deferred revenue to monthly revenue heard in the P&L account.

The journal entry for the same transaction would be as follows,

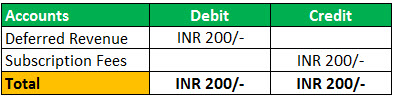

Each month after the delivery of the magazine to the customer, the accountant will transfer INR 200/- from the deferred revenue account to the Subscription Revenue account in P&L, as shown in the journal entry below. In the same way, each month, the whole amount from the deferred revenue account would be taken care of at the end of the year.

Deferred Revenue (Income) Video Explanation

Example #2 – Software Leasing

We can see a software manufacturing company which manufactures antivirus for computers. Software companies collect annual prepayments for the software, which is supposed to be used every month by the customer. The company will receive a total amount for the 12 months and transfer this amount to the Deferred Revenue head when receiving the prepayment amount. Each month, the company will transfer the 1/12 portion of this amount to the actual revenue head in the P&L account for the month when the customer is using that software.

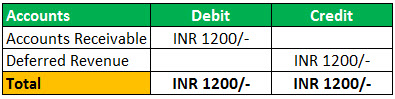

Suppose the cost for the antivirus software is INR 1200/- annually, which the customer is paying in advance. The journal entry for this transaction is as per below:

Example #3 – Auto Leasing

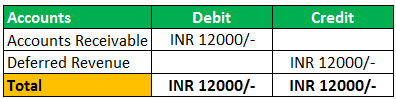

A bus leasing company has signed a work contract with an IT company to provide its buses on the annual leasing basis of INR 12000/- each bus, which would be payable in advance at starting the contract.

In this case, the IT company will transfer INR 12,000/- for each bus to the leasing company as an annual advance payment for its services. The leasing company will record this transaction to its Deferred Revenue head on its liability side of the balance sheet. They have to deliver their services for the next 12 months but receive the whole amount in advance.

The journal entry for this transaction would be as follows,

Example #4 – Gym Membership Fees

The best example to understand this concept is that of Gym Membership. Gym organizers annually charge it as advance payment giving gym services for the next 12 months.

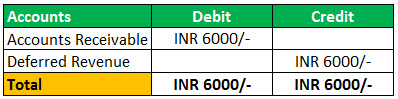

Suppose Gold Gym sells its membership plan for 6000/- per annum, INR 500/- per month, but it collects the whole amount for membership in advance from the customers. Mr. A wants to join Gold gym and transfers INR 6000/- to Gold Gym Account. The accountant will account for this transaction into the Deferred Revenue head as the services for the same amount have not been delivered yet, and the same will be provided in the next 12 months.

The accounting journal entry would be as follows,

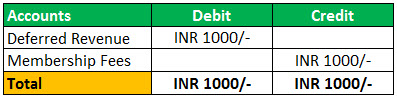

Each month the accountant will transfer monthly membership fees to its membership fees account in the P&L as follows,

In this way, the accountant will transfer monthly membership fees to its P&L each month, and at the end of the 12th month, the full deferred revenue account will be taken to membership fees accounts.

Conclusion

The following kind of organizations deal with deferred liabilities,

- Software leasing companies, and auto leasing companies, collect leasing amounts annually for their services.

- Insurance Companies that issue insurance policies for General Insurance, Health Insurance, etc. These companies collect insurance premiums on an annual basis, and they will cover any claims for the next 12 months or as per the policy structure.

- Any professionals who collect retainer fees (Audit firms, Lawyers, Business Consultants). These professionals collect annual retainer fees in advance and provide their professional services as per the contract signed and the client.

- Any businesses which collect subscription fees, such as magazines and grocery delivery companies;

- All those companies which have membership fees, such as Gyms, clubs, etc.;

From the above examples, we have understood that Deferred Revenue is an advance payment for any goods and services delivered or serviced in the future. It will transfer to the Deferred Revenue accounting head on the liability side of the balance sheet. Deferred revenue is also called Unearned Revenue, which will be earned in the future but collected in advance.

It could be considered as debt also as clients will give you advance payment for any goods and services you are going to deliver in the future, but this extra cash you can use for your business. It’s a kind of line of credit.

Recommended Articles

This has been a guide to Deferred Revenue Examples. Here we discuss the top 4 practical examples of deferred revenue like Magazine Subscription, Software Leasing, Auto Leasing, Gym Memberships Fees, etc. You can learn more about accounting from the following articles –