Part of our Income Statement guide

What is Non-Interest Income?

The non-interest income is the revenue generated from the non-core activities by the banks and financial institutions (loan processing fee, late payment fees, credit card charges, service charges, penalties, etc.). It plays a vital role in its overall profitability.

Explanation

- The core activity of any bank or financial institution is to accept deposits and from the accumulated deposits bank lends money. Thus, a bank earns interest income by lending money to the borrowers at a higher rate and paying interest on the deposit accounts at a relatively lower rate. The net interest income is the difference between the earned and paid. Thus, in the banking business models, the net interest income is the net interest income. Thus, in the banking business models, the net interest income is the operating revenue generated from the core activities of the business.

- The total income of any Bank or financial institution is the sum of interest income and non-interest income. However, it is not the only source of income a bank or financial institution may have during the year of operation. The other revenue streams are not directly attributed to lending the money.

Interest Income Explained in Video

Examples of Non-Interest Income

- For example, assume XYZ Bank lent the US $ 1000,000 to ABC Inc. at the rate of 6% p.a. for ten years equated to repayment. Let us assume the bank earned a total interest income of US $ 60,000 from ABC Inc. However, at the time of sanction of the loan, XYZ bank charged 0.5% of the loan amount towards the Loan origination fee, an upfront payment of US $ 500 towards the other service charges.

- The amount of US $ 5000 (as Loan origination fee) and the US $ 500 (as other service charges) is also income for the bank, but this US $5,500 is not coming from interest charges. Thus this income is classified in the books of XYZ Bank as Non-Interest Income.

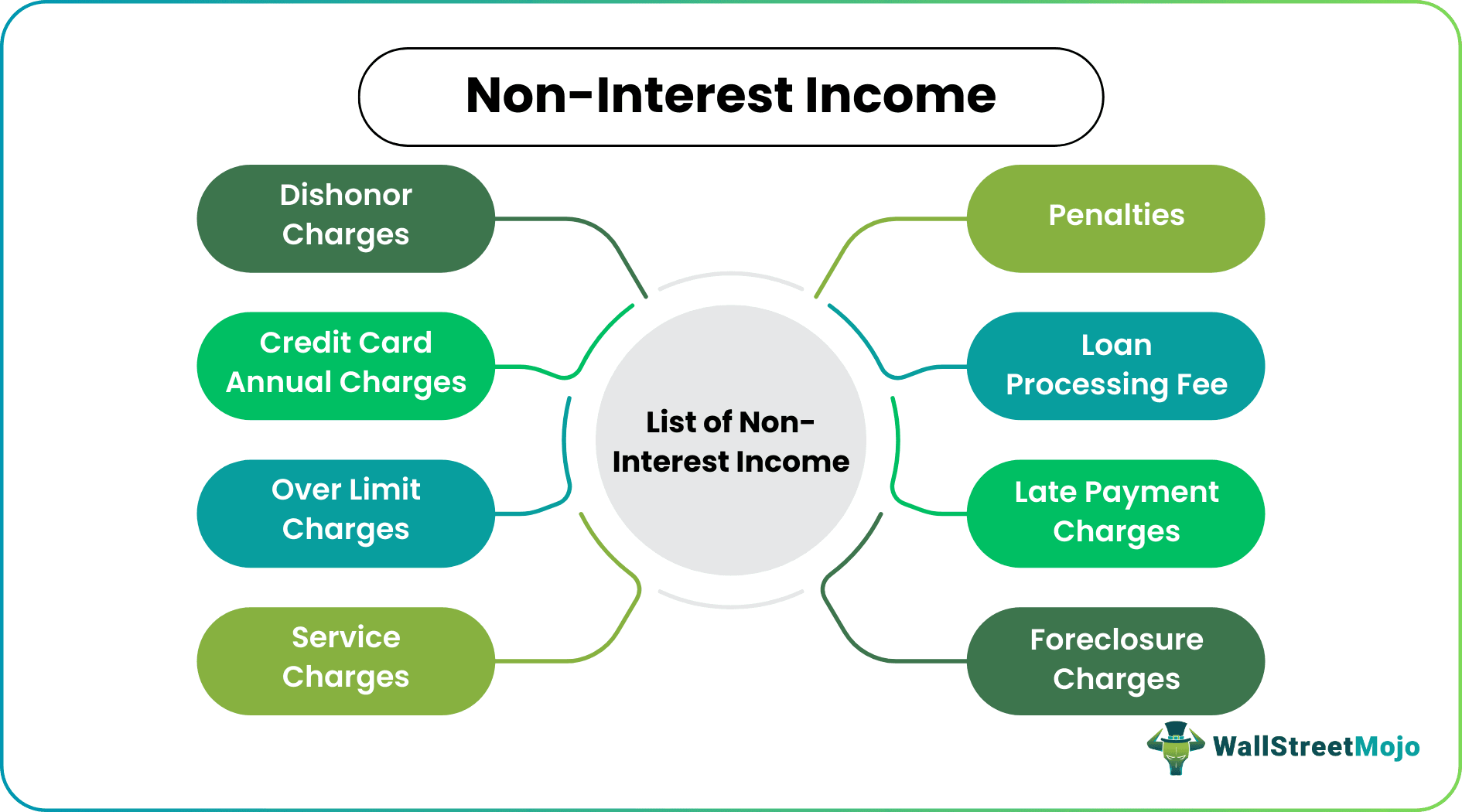

List of Non-Interest Income for Banks

List of Non-interest income includes income earned from the non-core activities of the banking business, such as:

- Loan processing fee

- Loan origination fee

- Late payment charges,

- Foreclosure charges

- Over limit charges,

- Credit card annual charges,

- Cheque book issue charge

- Insufficient funds charges,

- Service charges

- Dishonor charges

- Penalties

Significance

- Generally, for any business that manufactures or trades goods or provides any service, the non-interest income is considered the revenue generated from the core business activities such as the sale of goods or services. However, only in the case of banking and the financial institution the interest income is considered revenue generated from core activities. It is considered income from non-operating activities of the business. It is because the critical operational activity for any bank or financial institution is accepting money deposits and lending money

- However, it becomes significantly important during the economic slowdown or financial crisis when the banks face difficulties in lending money or when the bank lends money at lower interest rates. Due to any of these, banks struggle to maintain their margins. In such scenarios, the earning inflow from other non-interest income becomes crucial for the banks to offset the loss due to the lower interest rate.

- The following table shows the last ten-year trend of interest income and non-interest income of all the US commercial banks. One can observe that when the interest income of the banks decreased in 2009 due to the financial crisis when banks were not ready to lend any additional money, the % of non-interest income increased significantly.

Non-Interest Income as a % of Interest Income

| Year | Number of Commercial Banks | Interest Income | Non-Interest Income | Non Interest Income as % of Interest Income |

|---|---|---|---|---|

| 2008 | 7077 | 530.61 | 194.17 | 36.59% |

| 2009 | 6829 | 482.34 | 242.72 | 50.32% |

| 2010 | 6519 | 481.65 | 216.69 | 44.99% |

| 2011 | 6275 | 455.65 | 213.04 | 46.76% |

| 2012 | 6072 | 444.66 | 227.66 | 51.20% |

| 2013 | 5847 | 430.48 | 231.9 | 53.87% |

| 2014 | 5607 | 429.42 | 227.84 | 53.06% |

| 2015 | 5340 | 438.2 | 233.56 | 53.30% |

| 2016 | 5112 | 471.9 | 232.74 | 49.32% |

| 2017 | 4918 | 524.35 | 235.92 | 44.99% |

| 2018 | 4717 | 610.05 | 254.34 | 41.69% |

United States Commercial Bank (US $ in millions)

Drivers of Non-Interest Income

- The extent of non-interest income variation is counted on economic scenarios. The interest income largely depends on the minimum rate of interest charged on the sanctioned loan value. The interest rate is based on the Federal Bank’s benchmark rate. Now, when the economy faces challenges of deflation, as a preventive measure Federal Bank lower the interest rates.

- In such a case, the banks are supposed to pass down the credit of reduction in interest rates to the consumers. It is done by revising the rate of interest charged on the loans. It leads to a fall in the interest income of the bank. To offset the revenue fall, the banks slightly increase the charges levied on transactions that constitute the non-interest income.

- Likewise, when the economy goes through inflation, the Federal bank raises the interest rate to increase the cost of borrowing to control the price hikes. It increases the interest income.

- However, non-interest income falls because the consumer avoids borrowing the money at the higher cost of funds, which results in a decrease in loan origination changes, loan service charges, late payment charges, etc.

Conclusion

The non-interest income is generated from non-core activities of banking and financial institutions. It plays a vital role in the overall total income of the banks. Mostly, the non-interest income is affected by the extent of interest income.

Recommended Articles

This has been a guide to What is Non-Interest Income & its Definition. Here we discuss the list of non-interest income in Banks, its significance, and examples and drivers. You can learn more about it from the following articles –