Part of our Income Statement guide

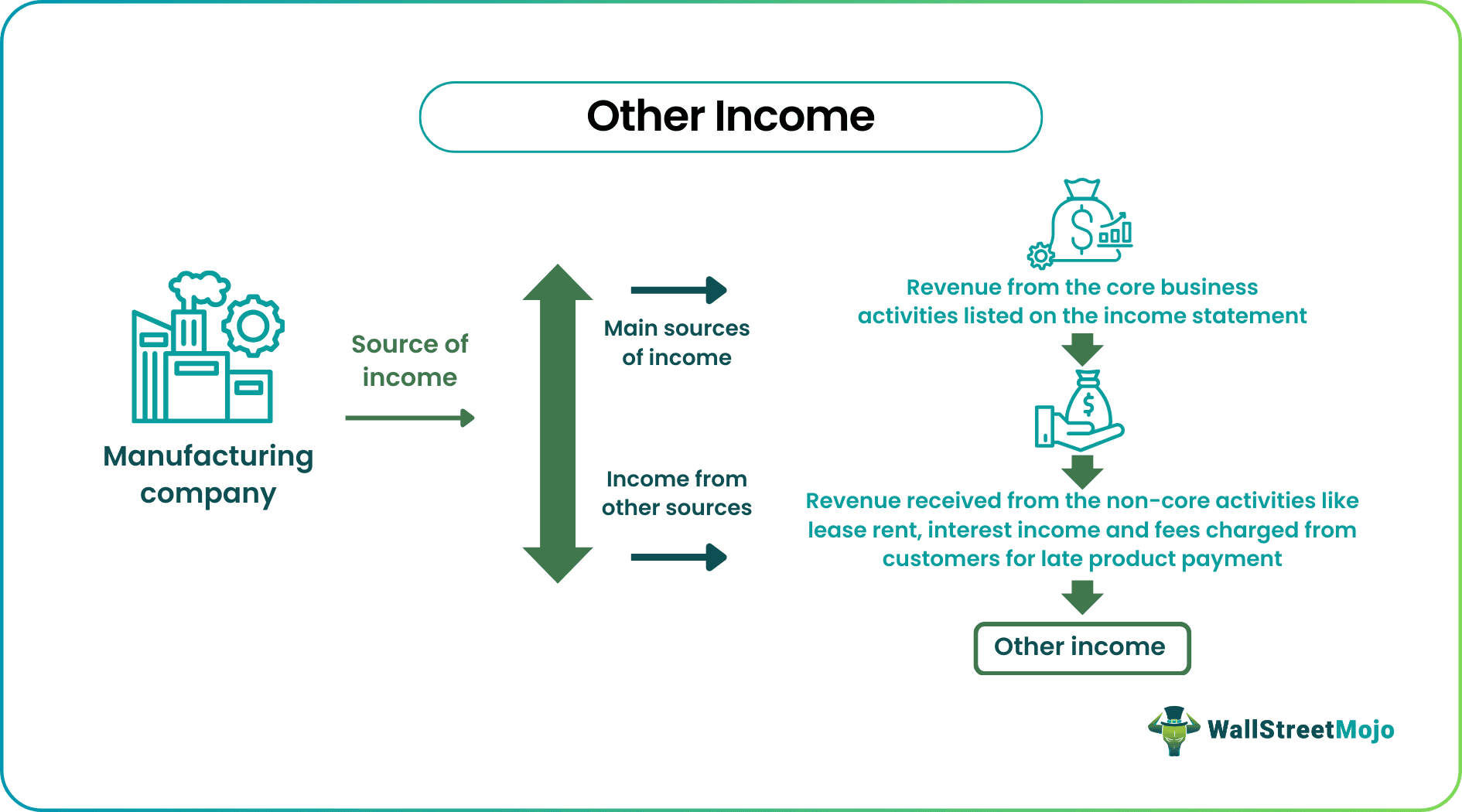

What Is Other Income?

Other income refers to those sources of income of an individual or business which arise out of activities besides the main activity to be recorded separately in Schedule 1 of Form 1040 or on the income statement. It conveys to the authorities that the earnings are from activities besides regular taxable income.

Additional earnings list any income individuals or firms receive from sources without any document. For example, one normally reports canceled loans and inward foreign remittances as other earnings. Hence, businesses only report additional earnings to save tax when it does not come from the main business activity. Examples include fines, interests, rents, and gains.

- All those types of income that come from sources other than a firm’s core business get listed as other income in its income statement.

- It has to be shown in Schedule 1 of tax return form 1040 and recorded in the line after gross profit in the income statement as per IRS other income guidelines.

- There is no fixed criterion to assign an income as additional income. Still, if the revenue from the non-core business is less than 10 percent, it falls into this category.

- Interest income, exchange rate gain, revaluation of fixed assets, and sale of non-current items are examples of additional income.

Other Income In Income Statement Explained

Other income means earnings that come through other sources and activities not part of any business’s core activity or core sources of earnings. It means additional earnings. One routinely records in the income statement just at the end after the gross profit section. Only if the value of the additional earnings falls within 10% of the total earnings does one categorize it as other income. Otherwise, analysts deem the earnings from other sources as a part of the firm’s revenues.

Although companies often record this type of earnings in a separate section before the operation section, no set rules are defined anywhere in the accounting standard for recording it in the profit and loss statement. However, one can set any applicable rule to put the earnings from certain sources as other earnings and other sources as mainstream earnings. Moreover, one must recognize that the criteria for classifying the revenue and other income should be where the rewards or risks are transferred homogenously in the profit and loss statement.

Analysis of the nature of earnings concerning the core business or services offered or products that companies manufacture can become the most basic factor for categorizing it as other income and expenses. For instance, a car manufacturer will get all its revenues from selling its car, spare parts, and customer service. However, if the company gets extra earnings from charging extra fees to customers making delayed payments, it will be its other earnings.

Analysts and researchers calculate other earnings by subtracting operating expenses from gross profits, adding revenue from other sources to it, and subtracting the expenses from it. However, for individuals, as per IRS other income clauses, every payment one gets on a personal basis has to be shown in Schedule 1 of Form 1040.

Types

A firm can include many types of earnings in the other earnings category of the earnings statement, such as:

- Earnings from foreign receipts or remittances if one pays taxes on it and also canceled debts.

- The earnings from the interest earned on the company deposits in the bank.

- The earnings received from the sale of non-current items of the company.

- Earnings from gains after revaluation of company fixed assets.

- Earnings from the charging of interest on customers (applicable to non-banking firms).

- Other income streams from exchange rate gain.

- Earnings out of charging penalties on suppliers, customers, and staff.

Revenue vs Income Explained in Video

Examples

Let us look at some other income examples:

Example #1

Let us take an American firm XYZ that has the following data available to us:

Annual revenue generated by the company = $600,000

Total sales revenue of the company = $400,000

And additional yields from other sources=, $ 10,000

Then the summary of the profit and loss statement will reflect as below:

Annual revenue = $600,000

Sales revenue = ($400,000)

Gross profit = $200,000

Other income = $10,000

Example #2

Let there be an incense stick manufacturer ABC that earns annual revenue of $100,000. It has lots of employees to prepare the incense sticks. It owns two big warehouses and a small shop-like space in a market complex for storing the raw materials that it requires during the peak season of Halloween and Christmas. However, the rest of the time, the shop-like space lies vacant without contributing to its revenues.

Nevertheless, the company has recently received a proposal from an ice cream seller to use the vacant shop-like space for rent for periods other than Halloween and Christmas. Given extra earnings, it accepted the proposal and agreed to a monthly rental of $3000. Hence, these earnings do not form part of revenue as they do not generate from its core business. Therefore, ABC will classify the ear from rental as other income in its earnings statement and record it for accounting procedures.

Example #3

Fines and late fees are other examples of other earnings. Some business-to-business (B2B) companies obligate their customers to quick payments. They should proceed with the payment on the same day or within a month when the products and services are delivered. If they fail to do so, some firms charge them fines as late fees.

The fines are unpredictable and do not relate directly to the firm’s core activities; accountants record them separately on the company’s profit and loss statement.

Negative Other Income

The other earnings section appears negative if the other expenses sum exceeds the other earnings sum. For example, this happens if large firms or organizations put other earnings and expenses in the same section on an earning statement. As a result, the firms mark a comprehensive loss during such periods.

Frequently Asked Questions (FAQs)

1.What is comprehensiveother income?

Those transactions representing the balance after subtracting net earnings from comprehensive income constitute other comprehensive income (OCI). OCI includes expenditures, profits, losses, and incomplete revenues per business accounting standards.

2.What is the difference between income and other income?

Other income is not taken as revenue. Firms calculate income from the company’s core business activities, like selling goods and services. In contrast, they calculate other earnings from is from external sources which are not related to the firm’s prime activities.

3.How to calculate other income?

It depends on the method of accounting employed by the assessee regularly for calculating the earnings from other sources (IOC). For example, if the assessee uses the mercantile system, then the accrual basis for calculating the IOC. The total operating earnings of a firm get added to the revenues from other streams, and net expenses get subtracted to calculate the other income.

Recommended Articles

This article is a guide to What is Other Income. Here, we explain its use in income statement, types, negative other income, and examples. You can also go through our recommended articles on corporate finance –