Table Of Contents

Conduit Financing Definition

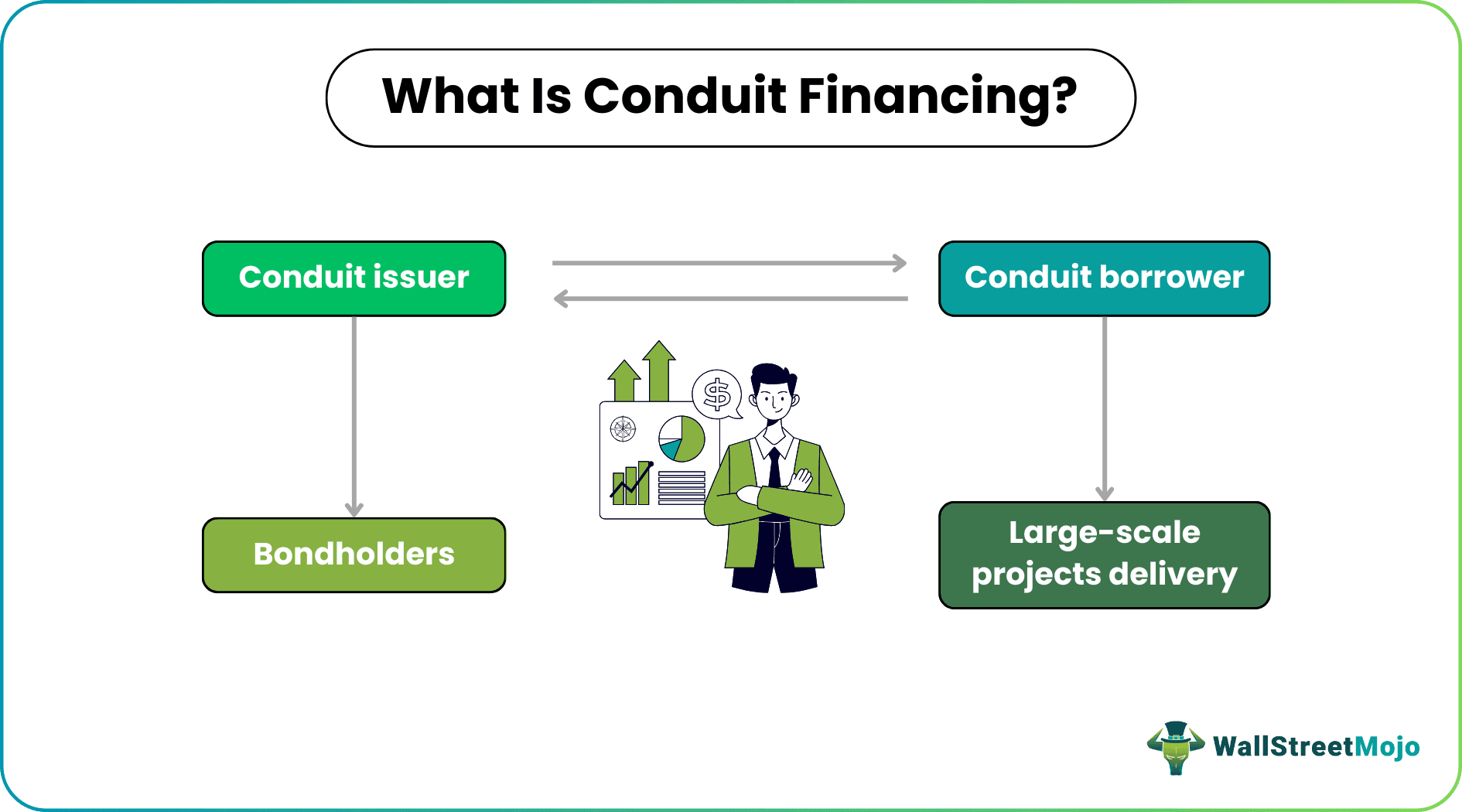

Conduit financing refers to an outstanding non-rated public security for which a private for-profit or non-profit issuer serves as the security's primary credit provider. A local or state government issues bonds and gives the bond revenues to a different party, and that entity is then responsible for repaying the bonds.

The conduit is a short-term finance arrangement that gets money swiftly to the borrowing party. For example, conduit financing secures longer-term loans or mortgages, which is a route for money from investors to borrowers. Moreover, conduits can alter the characteristics of debt instruments and increase their appeal to investors.

Key Takeaways

- Conduit financing refers to an outstanding non-rated public security for which a private for-profit or nonprofit issuer serves as the security's primary credit provider.

- In the municipal bond market, conduit financing comprises the issuance of bonds by a state or local government and transferring the bond proceeds to another organization.

- Similar to any other bonds, they also possess benefits and risks. Therefore, it is sometimes also referred to as conduit bond financing. This is because contractual agreements happen between the conduit issuer and the conduit borrower

Conduit Financing Explained

Conduit financing in the municipal bond market entails a state or local government issuing bonds and giving the bond revenues to a different entity (sometimes referred to as a conduit borrower) that assumes responsibility for bond repayment. They aim to finance client loans and purchase longer-term bonds secured by debt, such as mortgages.

This conduit financing arrangements is sometimes also referred to as conduit bond financing. Conduits invest in long-term, comparatively illiquid assets. They finance these investments by raising short-term debt secured by several debts, including credit card debt and home mortgages. Here, the issuer only has to make payments on the bonds to the extent that it receives funds from the borrower or related parties.

Additionally, the conduit issuer's responsibility is to offer tax exemption or tax credits relating to the bonds or give the borrower access to the municipal bond market. Therefore, the issuer's credit is not a part of the transactions. Hence, one cannot consider it a real party in interest in the financial essence of the transaction.

The conduit conduit financing arrangements issuer and the conduit borrower make contractual agreements between them as part of the financing. For example, a lending agreement, a lease/leaseback arrangement, an installment sale agreement, or some other contract specifies the repayment of the bonds, depending on the statute or policy in question.

It entails the conduit issuer lending the bond proceeds to the conduit borrower by a loan agreement. It also entails the conduit issuer assigning the right to receive payment under that loan contract as collateral to the bondholders (or to a trustee for the bondholders) to secure and provide for bond repayment.

The purpose of conduits is to offer affordable finance. Bank profits wouldn't be as high as anticipated if they had to finance those assets for longer than a few weeks without accounting for any decline in the assets' actual worth.

Example

Let us analyse the concept of conduit financing regulations with the help of an example.

A housing project for the poor needs funds, so the organization in charge of the construction decided to search for funds, and they stumbled upon an idea. They issued bonds to collect money through conduit financing. With the help of capital they raised through conduit funds, and completed the houses. Since this is a public cause, the agency will also have tax exemption.

From the above example we see how the concept can be used for raising funds and using it for social betterment, without putting any pressure on both the parties, the investor and the borrower.

Risks And Benefits

Conduit bond financing involves certain risks and benefits, and they are as follows:

Risks

- Conduit bonds, unlike regular bonds, do not have the full backup of issuing authority's (government or agency) faith and credit. Hence, in this case, more significant returns come at a higher level of risk.

- When buying conduit bonds, investors are putting their money into the projects themselves, not the conduit issuer, so it is essential for them to remember this and to research the project well.

- It's also crucial to have information and proof to support their belief that the project has a chance of success.

Benefits

- Conduit bondholders typically receive higher returns than holders of municipal bonds, the same federally tax-free interest income. In addition, tax-exempt financing may be available to agencies that demonstrate public benefit. For example, housing, hospitals, pollution control measures, and facilities are public benefits.

- By owning conduit bonds, an investor may also be free from paying state and local taxes on interest payments if the bond issue is in the state where the investor resides. However, the tax-free benefit of any municipal bond only applies to the revenue from the bond's interest.

- It may be subjected to capital gains and are hence subject to taxation and is required to be reported to the Internal Revenue Service. In addition, municipal bonds may also be subject to the alternative minimum tax (AMT).

It is important to analyse the risk and benefits of the financial concept of conduit financing regulations so that it can be implemented at the right time and for the right purpose. Analysis of the risks will help the management implement better control so that the risks can be minimised. The benefits will provide incentive to use it to achieve the financial objective of the organization.